Reason Foundation’s 2024 Pension Solvency and Performance Report provides a comprehensive overview of the current status and future of state and local public pension funds. As the nation navigates another year marked by significant economic fluctuations and demographic shifts, this report aims to assess the resilience and adaptability of U.S. public pension systems. This analysis ranks, aggregates, and contrasts plans by funding health, investment outcomes, actuarial assumptions, and many other indicators.

This report marks the inaugural edition of an annual series by Reason Foundation’s Pension Integrity Project, dedicated to addressing the problem of unfunded public pension liabilities that threaten the fiscal stability of many states, cities, and counties. The objective of this analysis is to deliver clarity and foster a deeper understanding of the challenges confronting U.S. public pension systems, public workers, state and local governments, and taxpayers. The main findings are prominently highlighted in bullet points at the beginning of each section.

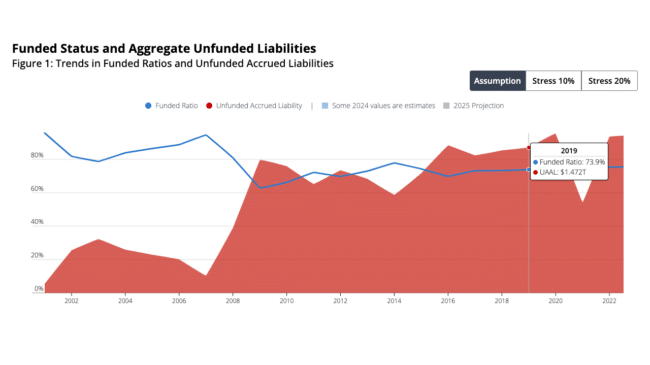

Unfunded pension liabilities

Public pension systems in the U.S. have seen a significant increase in unfunded liabilities, particularly during the Great Recession. Between 2007 and 2010, unfunded liabilities grew by over $1.11 trillion—a 632% increase—reflecting the financial challenges faced during that period. Despite some improvements in funding ratios over the last decade, these liabilities have continued to rise, underscoring ongoing financial pressures.

As of the end of the 2023 fiscal year for each public pension system, total unfunded public pension liabilities (UAL) reached $1.59 trillion, with state pension plans carrying the majority of the debt.

The median funded ratio of public pension plans stood at 76% at the end of 2023, but stress tests suggest that another economic downturn could significantly increase unfunded liabilities, potentially raising the total to $2.71 trillion by 2025.

Funded ratios of public pensions

The funded ratio of public pensions, which indicates the percentage of promised benefits that are currently funded, has experienced considerable fluctuations. After peaking at 95% funded in 2007, the funded ratio of U.S. public pension systems fell to 63% during the Great Recession. Although funded ratios have recovered somewhat, they remain susceptible to market fluctuations.

A stress test scenario for 2025, assessing the impact of a 20% market downturn, indicates that the average funding level of public pension plans could fall to 61%. This could lead to critical underfunding for many pension plans, raising concerns about their ability to meet future obligations.

Changes in investment strategies

Over the past two decades, investment strategies of public pension funds have shifted notably. Allocations to traditional asset classes, like public equities and fixed income, have decreased while investments in alternative assets, such as private equity, real estate, and hedge funds, have increased. This shift reflects a strategic move for pension systems trying to achieve higher investment returns in a challenging market environment.

By the reported 2023 fiscal year end for each pension system, public pension funds managed approximately $5.05 trillion in assets, with a significant portion now invested in alternative assets such as private equity/credit and hedge funds. While these alternative investments may offer the potential for higher returns, they also introduce greater complexity and risk.

Pension system investment performance: Overly optimistic assumptions, underwhelming returns

Public pension funds have faced challenges meeting their assumed rates of return (ARRs). Over the past 23 years, the average annual return has been 6.5%—well below what plans had assumed. The average assumed rate of return for public pensions has been gradually reduced from 8.0% in 2001 to 6.89% in 2023. Failing to meet their overly optimistic assumed rates of return has contributed to a large increase in unfunded liabilities, requiring additional pension contributions from state and local governments to maintain funding levels.

Investment returns themselves have varied widely, with public pension plans posting solid gains in 2021 (25.3%) contrasted with large losses in 2009 (-13.0%) and 2022 (-5.0%). This volatility between expected and actual returns has created budgetary challenges for employers.

Employer contributions

As unfunded liabilities have grown, the burden on employers—primarily state and local governments—has increased. Employer contributions to public pensions have risen steadily since 2019, driven by the need to address rising amortization costs associated with unfunded liabilities. In contrast, employee contributions have remained relatively stable, placing more financial responsibility on government budgets.

Despite these increasing contributions, many pension plans continue to operate with negative cash flows, where benefit payments exceed contributions. However, some progress in recent years suggests that pension managers are beginning to address these financial challenges more effectively.

Conclusion

Public pension systems face significant challenges as they navigate rising unfunded liabilities, variable investment returns, and increasing financial demands on government budgets. Without meaningful pension reforms and more realistic assumptions about future investment returns, many public pension plans may encounter further financial difficulties in the years ahead.

This report was produced by Reason Foundation’s Pension Integrity Project—an initiative to conduct research and provide consulting and insight about the public pension challenges our nation grapples with.

Full Study: Annual Pension Solvency and Performance Report