The political and social equality of the sexes has led many to assume economic equality would soon follow. It didn’t. Women still, on average, make less than men. The best evidence suggests this is not driven by discrimination, but rather, because men and women tend to lead different lives and therefore have different—though interconnected—careers. Most women will get married and become mothers, and mothers are more likely to take career breaks, temporarily work part-time, or switch to jobs with flexible hours, particularly during their children’s early years.

These differences in men’s and women’s careers have direct implications for retirement. Some employee-provided retirement benefits structures are more flexible than others, better accommodating career interruptions. Rather than providing one-size-fits-all retirement benefits, employers and policymakers should consider offering plans that accommodate a wider range of career paths.

Broadly, there are two main retirement benefit models: traditional defined benefit (DB) pensions and defined contribution (DC) accounts. In the private sector, portable DC plans—401(k)-style accounts—are the norm. But in the public sector—especially at the state and local level—most employees are offered a DB pension, which is explicitly designed to reward long, continuous tenure with a single employer and penalize early departure, leaving many public employees with insufficient retirement wealth if they leave before vesting.

Given that most new hires in the public sector leave within the first several years of employment, it is essential that they have access to portable and flexible retirement benefits, such as a defined contribution plan. Because women’s careers are more likely to include interruptions, retirement plan flexibility matters even more for them.

The motherhood gap

There has long been a gap between the average pay of men and women, often estimated at about “80 cents on the dollar.” But this statistic compares median earnings across the entire workforce; it does not compare men and women in the same roles, with the same hours, tenure, and experience.

When researchers control for education, occupation, age, and hours worked, early-career earnings for men and women are indistinguishable—in fact, some recent analyses have even found that, in big cities and highly educated areas, young women now earn more than young men.

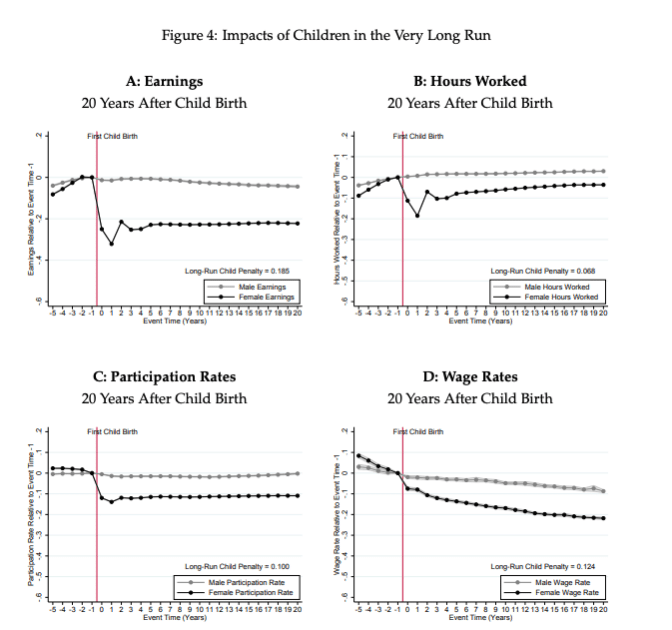

The “gap” between men’s and women’s earnings starts around the birth of a woman’s first child—and it persists for years afterward. Therefore, what is commonly referred to as the gender pay gap is more accurately described as a motherhood pay gap.

Using Danish administrative data from 1980 to 2013, a study found that men’s and women’s earnings trajectories were nearly parallel before the birth of the first child. The gap opened sharply after childbirth. Although it narrowed somewhat as children aged, it never closed. The authors estimated that the long-run cumulative earnings penalty for mothers was approximately 20%. This pattern is widely reported in analyses that cover American workers.

While women with children are more likely to be employed than the overall population, their employment status and schedules differ based on the age of their children. Women with younger children are less likely to be employed or more likely to work part-time than those with older children, whereas fathers of both younger and older children are just as likely to be employed. Caretaking is the most commonly reported reason by mothers for periods of joblessness or part-time work.

Is the motherhood wage gap a problem? Many economists view it as a reflection of the voluntary choices of men and women—a rational allocation of capital within the household, given that women have a biological role in parenthood that men don’t. Others believe the gap is a reflection of unfair expectations and biases placed on women and a failure of economic and labor markets to accurately support mothers. Still others believe that, although it is a result of freely made choices, employers could do more to enable women to balance work and family life, to the employer’s own benefit.

For those designing retirement benefits, the key point is that the motherhood gap exists. Regardless of its causes, motherhood affects women’s careers in predictable and systematic ways, which in turn shapes how they can accumulate retirement savings.

The two retirement benefit models

Women are more likely than men to work in the public sector. At the state and local level, women make up 56% of state government and 62% of local government employees.

Most women will be mothers. At the same time, women’s earnings represent a large share of their household’s wealth, with at least 40% of women being the main or sole breadwinner in their household. Retirement benefits should be structured with both facts in mind: that women’s earnings are fundamental to household wealth, yet they are more likely than men to take career breaks or seek more flexible employment to accommodate childcare responsibilities.

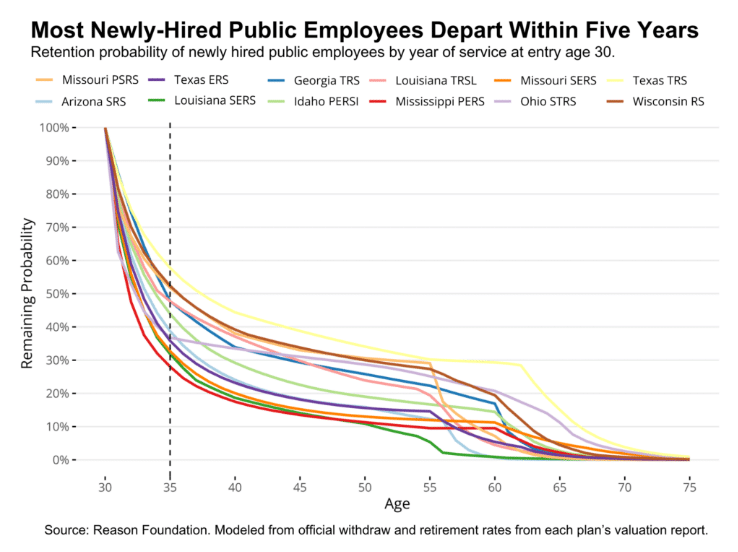

In the public sector, almost all employees are offered traditional DB pensions, which are explicitly designed to encourage continuous tenure with a single employer. This structure provides certainty for employees who plan to remain with an employer for decades, but that has become the exception rather than the rule. A Reason Foundation analysis of 12 public pension plans found that most new hires leave within five years of hire.

According to Bureau of Labor Statistics survey data from 2025, among private-sector workers, only 14% had access to a DB pension, while 70% had access to a DC plan. Among state and local government workers, by contrast, 86% had access to a DB and only 36% had access to a DC.

DB plans guarantee a specific lifetime retirement benefit, which is typically defined by a formula, but employees must remain with an employer long enough to vest in order to earn that benefit. That structure tends to work for the minority of workers who remain with a single employer long enough to retire under the plan. But for workers who change jobs, reduce hours, or take breaks, DB benefits often end up being small or non-existent.

On the flip side, DC plans guarantee a defined contribution to an individual retirement account designed to be sufficient to fund retirement. Employees take on both the downside risk and the upside potential of investment outcomes. Importantly, employees gain flexibility and autonomy over their retirement savings: Vesting typically occurs quickly, or immediately, assets are portable, and workers are not exposed to benefit cuts or contribution increases driven by a retirement plan’s funding shortfalls.

Consider a hypothetical 27-year-old public school teacher who, after teaching for four years, leaves her job to take care of her young children. If her school offers a DB pension, assuming she leaves before the minimum vesting period, she will likely forgo her pension benefits, receiving only a refund of her share of retirement contributions. Her employer contributions—a major part of her compensation—are lost. Despite several years of work, she leaves with little retirement wealth.

If her employer offered a DC plan instead, both the employee and employer contributions made during those years would have remained invested in her account, assuming she had satisfied the DC plan’s vesting rules, which are typically much shorter than those of DB plans. Whether or not she later returns to teaching, those assets would remain invested and would grow year after year.

The advantages of DC and other portable retirement plans are especially important for single mothers, who are more exposed to career interruptions and cannot rely on a second household earner to accrue retirement benefits during eventual periods out of the workforce. It is estimated that one in five mothers in the US is a single mother.

This concern is especially relevant for Black mothers, about half of whom are single mothers. According to a Federal Reserve Bank of Boston paper, this is partly why Black families tend to hold substantially less retirement wealth than white families.

Flexible retirement benefits promote gender equality

Claudia Goldin, whose work on gender and labor markets earned the Nobel Prize, argues that the final step toward economic equality between the genders is increased workplace flexibility.

Conventional employment structures were designed with men’s lives in mind. Greater flexibility on all fronts—such as remote work and flexible hours—would enable higher productivity for women after birth. Workplaces that adapt will not only get more out of their current female employees but will also likely attract better talent and retain them for longer. Retirement systems should be part of this institutional adaptation. Flexible, portable retirement benefits complement modern labor markets and better reflect how women actually work. The private sector has largely adapted; the public sector still needs to catch up.