In 2011 and 2012, Alabama enacted major reforms to manage the runaway growth of the state’s public employee pension debt. The changes, including higher retirement ages, increased employee contributions, and reduced benefits for new hires, were some of the most extensive in the nation. While these reforms did reduce the growth of pension obligations, the state’s funding shortfalls have continued to grow to over $20 billion. Fourteen years later, the need for another round of reform is as great as ever.

The most common measure of a state’s pension health is the funded ratio, which compares what the system owes to retirees against what it has set aside to pay them. The three plans in the Retirement Systems of Alabama (RSA)—the Teachers’ Retirement System, TRS, the Employees’ Retirement System, ERS, and the Judicial Retirement Fund, JRF—have an aggregate funded ratio of 70.1 percent, according to Reason Foundation’s Annual Pension Solvency and Performance Report. This means the systems have only 70 cents set aside to pay for every dollar Alabama has promised its public employees, placing Alabama at 36th among all states for funding ratios.

In 2021, the state’s funded ratio was 75.2 percent, before dropping to 59.7 percent the next year. While Reason estimated this figure would recover to 72.7 percent in 2025, the volatility indicates a system that is heavily exposed to market swings.

The 2011 and 2012 pension reforms were substantive and brought about changes that significantly reduced projected future costs. These reforms also bought time. But solving the underlying problem is an entirely different matter, and the funded ratio trajectory since 2012 suggests that the structural gap has persisted.

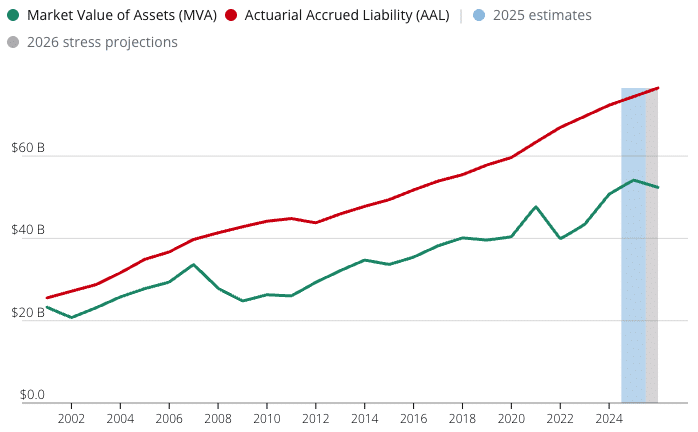

Alabama’s pension assets have not kept up with liabilities

Despite reforms, the burden of pension debt on Alabama taxpayers has continued to grow. In 2012, the combined annual cost of RSA across all three retirement plans totaled $15.4 billion, according to actuarial valuations published by the system. By 2025, these annual costs had grown to 27.2 billion. Taxpayers are paying more, not because benefits have improved, but because the underlying debt kept growing.

One major reason for this growth is a flawed assumed rate of return. This assumption determines how much the state is required to contribute each year. If the system maintains a high return expectation, required contributions remain low on the assumption that the returns will cover funding needs. If returns fall short of this expectation, this creates unfunded liabilities, and the funding gap widens. The RSA currently assumes its portfolio will earn 7.45 percent annually. Over the past 24 years, it has actually earned an average of 6.4 percent. That gap, compounded over decades, created unrealized losses that eventually became unfunded pension liabilities. Alabama ranks 47th nationally for the probability of achieving its assumed return, according to Reason’s annual pension report. Almost no state in the country is less likely to hit its return target than Alabama.

The flaw is not in investment management but in the assumption itself. Alabama ranks 26th in 24-year investment performance. Of the 25 states ranked above Alabama, only two have been able to achieve average returns above RSA’s assumption of 7.45 percent. Nearly every state system, including Alabama’s, has lowered its assumptions since 2008. But RSA’s adjustments have not been enough to match the system’s target with its demonstrated long-term performance.

In other words, there is likely still a significant amount of pension debt that Alabama will eventually realize as return assumptions continue to fall.

Alabama’s unfunded liability now sits at over $24 billion, up from roughly $14.4 billion a decade ago. Despite rising pension contributions, rather than shrinking, the debt has continued to grow, generating liabilities that compound the problem each year, even during periods of strong market performance.

Part of the reason the unfunded liability keeps growing is that the state just isn’t putting enough money into the system to close the funding gap. Alabama ranks 44th nationally in employer contribution adequacy rates, according to Reason. This ranking calculates the contribution needed to pay off unfunded liabilities over 20 years. Alabama’s actual contributions fall short of this benchmark. The state’s aggregate employer contribution rate is 13 percent of payroll, well below the national average of 21.6 percent, suggesting most states are contributing more to address their pension debt than Alabama. Low contributions today mean higher costs tomorrow, as debt continues to compound.

The path forward isn’t complicated, even if it comes with growing pains. Lowering the assumed rate of return toward something closer to the demonstrated long-term performance would increase the required state contributions and raise the measured unfunded liability in the short term, but it would give legislators and the public a more accurate picture of what the retirement system actually costs.

Alabama lawmakers made great strides in reforming the state’s retirement system for government workers back in 2012, but growing debt and runaway costs suggest the need for further reforms to the system’s market-return assumptions. Lowering return expectations to more realistic levels will require more from government employers up front, but it will slow the state’s current path of ever-growing annual contributions placed on the backs of taxpayers, driven by the ongoing realization of more pension debt. To get the state back on track with pension funding, policymakers need to enact lasting reforms that address the sources of the state’s growing pension shortfall.