The Pension Integrity Project at Reason Foundation recently shared an analysis of Alabama’s pension funding challenges, which found that the state’s public pension maintains a higher-than-average return assumption. The Retirement Systems of Alabama (RSA) issued a response defending its procedures and arguing that Reason’s analysis should be “disregarded or discounted.” While Alabama’s pensions have adhered to counseled actuarial standards, Reason’s analysis—and the state’s ongoing challenges with growing pension debt—suggest those procedures may not be sufficient.

To set market return assumptions, the RSA relies on the recommendations of three independent actuarial firms that conduct five-year experience studies. In the last experience survey, actuaries recommended lowering RSA’s assumed rate of return by 0.25%. RSA followed that recommendation, lowering its assumption to 7.45%. But even after that reduction, Alabama maintains a return assumption well above the national average of 7%.

Reason’s analysis of assumptions and the probability of achieving these returns (based on market advisors’ forecasts) finds that RSA’s probability of achieving its 7.45% assumed rate of return over the next 20 years ranks 47th among all states. Reason’s analysis does not rely on a specific window of historical outcomes, but on the long-term expectations of market advisors reported by Horizon Actuarial Services.

The RSA’s response includes a chart showing returns over periods ranging from one year to 40 years, with particularly strong performance over shorter windows. This misses the fundamental point. Pension assumptions shouldn’t be based on past performance. They should reflect informed future projections. Capital market assumptions from major investment firms, actuarial organizations, and pension consultants have consistently projected lower long-term returns. That’s why every state pension system in the country, including Alabama’s, has lowered its assumed return over the past 15 years.

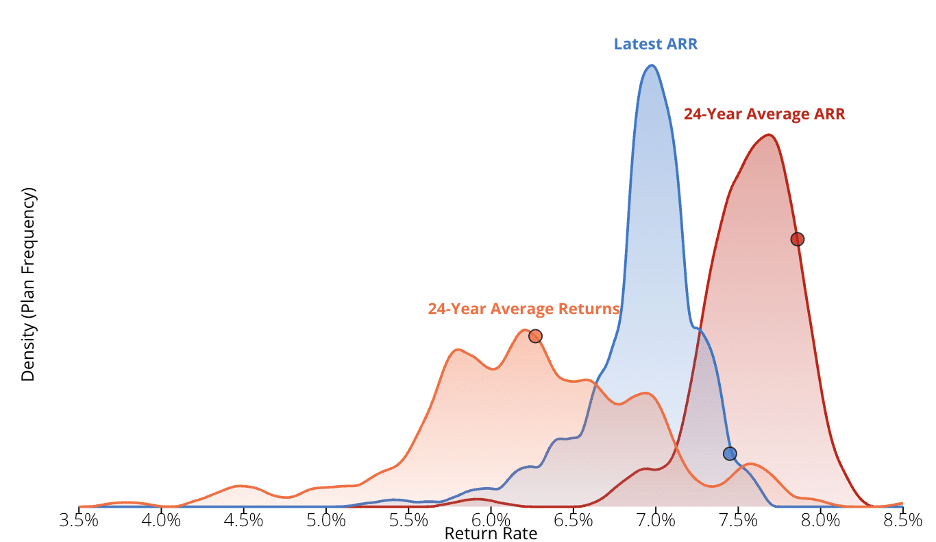

Pointing to 30-year or 40-year historical returns that include the bull markets of the 1980s and 1990s doesn’t justify an assumption that needs to hold true for the next two decades. The RSA may have earned strong returns in the past. But that doesn’t matter if a 7.45% assumption misses the mark of what investment professionals project going forward. By that measure, Alabama’s assumption remains on the high end nationally. Reason’s Annual Pension Solvency and Performance Report illustrates where Alabama’s assumed and achieved returns stand in comparison to those of other public pensions across the country. The red distribution plots the 24-year average assumed rates of return, while the orange distribution plots 24-year average realized returns. Additionally, the blue distribution plots the latest assumed rates of return held by the 315 government-run pensions included in the report. As shown in the chart, compared to other pensions, Alabama has consistently assumed, and still assumes, a rate of return above that of most public pension plans, while achieving only middle-of-the-pack investment results.

Alabama’s position in the distribution of pension plan assumed and experienced returns

Source: Figure 8 of the Reason Foundation Annual Pension Solvency and Performance Report, with “Alabama” selected as the state.

On methodology, RSA correctly notes that, for our state-by-state comparisons, the Reason Foundation readjusts all plans to be in a 20-year amortization benchmark and uses the market value of assets rather than the plan’s smoothed asset values. The RSA then claims Reason overstates Alabama’s unfunded pension liabilities, because Alabama amortizes its unfunded liabilities over a longer period. In reality, the universal adjustments made are to enable comparisons across all states, ensuring an ”apples-to-apples” analysis, not to overstate pension liabilities.

Actuarial assumptions have been, and will continue to be, subject to consideration and debate, but the critical facts to evaluate a pension’s status are all available in annual actuarial reports. Alabama’s unfunded pension liability has grown from $14.4 billion in 2012 to over $24 billion today. Despite rising contributions, its funded ratio has failed to recover, falling from 66.2% to 64.5% over the same period. The debt burden relative to covered payroll, calculated from RSA annual reporting, has grown from 151% to 183%.

RSA argues that much of this growth stems from fiscally conservative changes it has made, such as lowering the assumed return, updating mortality assumptions, and moving to a closed amortization period. Indeed, some of the unfunded liability growth does reflect adopting more realistic assumptions, which is exactly what they should continue to do.

The purpose of Reason Foundation’s analysis is to provide an independent perspective that helps policymakers and the public understand whether current policies are sustainable and to identify when reforms are needed, not just regarding return assumptions, but also funding policies and the design of retirement benefits.

Overly optimistic investment assumptions undermine sound funding by understating required contributions, deferring costs, and increasing tomorrow’s taxpayer burden. Alabama ranks near the bottom of the country in the probability of meeting its pension return assumption, meaning there is a high probability that the annual costs will rise beyond what is currently being estimated. Policymakers need to be aware that the state is at risk of underestimating required contributions and feeding future runaway costs for both government employers and Alabama’s taxpayers.