Unfunded retirement benefits held by municipal governments pose a growing challenge to states, namely through requests for state taxpayer funding to keep up with growing local costs. In response to the rising concern of compounding pension debt among cities and counties, Michigan passed Act 166 in 2022, which, combined with Act 202 of 2017, introduced an innovative approach—a “closed-loop” system that streamlined the disbursement of state funding. The program required pension units receiving state grants to adhere to a binding correction plan. Michigan’s initiative represents more than a transformative step for its fiscal landscape—it offers a potential model for other states grappling with similar challenges.

In a unanimous move, the Michigan legislature passed a robust package of 16 bills establishing a system to promote municipal pension solvency—the Protecting Local Government Retirement and Benefits Act 202 of 2017. The initiative aimed to address Michigan’s $18 billion in unfunded pension obligations by targeting the system’s most underfunded local pension units. Robust monitoring mechanisms were established, and municipalities that failed to reach a 60% funding threshold were placed on corrective action plans to shore up their plan finances. Through Act 166, $553 million in grants were dispersed to cover municipalities with the direst unfunded liabilities—under the condition that awarded pension funds would follow certain practices conducive to reaching long-term pension solvency.

The cleverness of Act 202 and Act 166 lay in the leveraging of additional taxpayer funding in the present to avoid even larger payments in the future. If the existing unfunded liabilities were left unaddressed, the debt would have continued to compound at an escalating rate. This would have progressively amplified the pressure debt payments applied on annual budgets, further impairing municipalities’ credit ratings and ability to raise capital through municipal bonds.

The grant accomplished two aims: First, it remedied a debt Michigan was—and still is—already liable for by paying it off earlier and avoiding large amounts of compounding interest. Second, it prevented the formation of novel unfunded liabilities by implementing sound accounting practices. With both facets in mind, the pension grant drastically reduced the expected fiscal expenditure that governments would have needed in its absence, promoting present and long-term fiscal solvency and, as the name suggests, retirement security across Michigan.

Act 202 and Act 166

As uncovered by the Reason Foundation’s data initiative UnfundedMichigan, at the time of Act 202’s passage in 2017, the median pension funding ratio in Michigan’s counties was around 72%, with a few local municipalities facing disproportionately poor funding levels. The city of Westland, for example, had only enough to cover 14.3% of their expected liabilities, short an estimated $355 million to achieve full funding.

Act 202 and Act 166 targeted the most vulnerable retirement units in two steps. It first established standardized mandated reporting and disclosure requirements, enabling Michigan’s Department of Treasury to monitor the levels of public pension solvency across the state. The pension unit reports were made available to the public for further monitoring and accountability. Secondly, it leveraged this robust reporting by offering funds with a verified funding ratio lower than 60%, a one-time state grant–only disbursed if they agreed to follow certain sound managerial practices.

To oversee and execute Act 202, the Municipal Stability Board (MSB) was instated. Part of the Treasury Department, the board was tasked with guiding the funding process for municipal pension funds and retiree healthcare plans. Beyond overseeing municipal pension funding levels, the MSB offered a corrective action plan for local government units at risk of insolvency, something we can call an intrastate closed-loop intervention mechanism to rescue the most insolvent pension units in the state.

The Intrastate Closed Loop

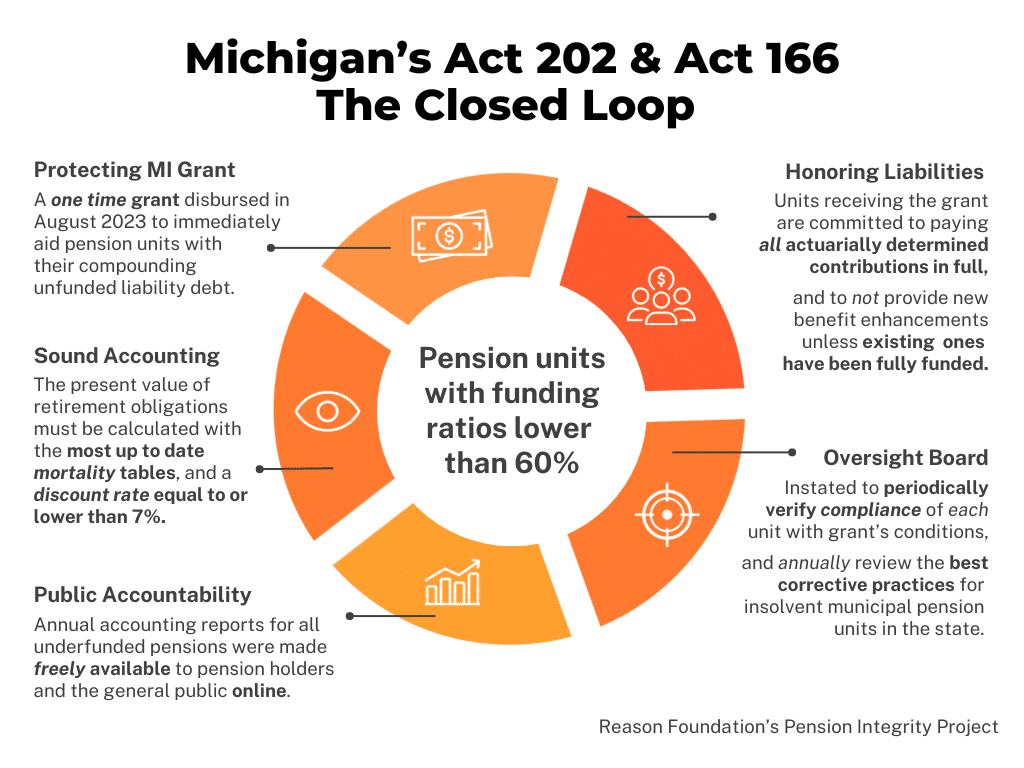

The funding mechanism initiated by Act 166 was named the Protecting Michigan Pension Grant Program. It targeted municipal pension units with funding ratios lower than 60%, that is, units that owned less than 60% of the assets needed to fund the retirement benefits already promised. Those who qualified could apply for a share of a $553 million grant, aiding those units in bringing their funding ratios closer to 100%.

To receive the grant, local units must sign an affidavit agreeing to follow certain practices. As set by the Public Act 166 of 2022, Section 979a(2)(a-f), upon receipt of the grant award, units are committing to:

- Pay all actuarially determined contributions in full;

- Not provide new benefit enhancements unless the already promised benefits are fully funded;

- Have a discount rate/assumed rate of return equal to or lower than 7%;

- Adopt the most updated mortality tables appropriate for the unit’s population; and

- Other potential corrective monitoring actions by the Municipal Stability Board (MSB) for five years following receipt of any grant award.

After a year-long application timeline, grant payments were finally disbursed in August 2023. Awards were calculated by multiplying the qualified retirement pension system’s liabilities by 60% (0.6) and subtracting the qualified pension system’s assets (fiduciary net position ending). The amount was capped at $170 million, with only one retirement system reaching the ceiling: the city of Flint.

Westland, mentioned earlier, with its dire 14.3% funding level and $355 million in unfunded liabilities, received its calculated portion—$26 million—in grants. So did 126 other pension units in the state, from cities, villages, counties, townships, and road commissions, who now have a head start on closing the unfunded liability gap.

The Municipal Stability Board is set to meet at least every two years to certify each participating retirement unit’s compliance with the act and the commitments in the signed affidavit. If a public pension plan is not in “substantial compliance” with Act 202, it must answer to the board detailing the specific reasons for non-compliance and present a time-bound corrective action plan.

Finally, the MSB is also set to annually update a list of best strategies to assist underfunded pension systems in developing corrective action plans.

A Model for Other States

Michigan’s grant program required a substantial fiscal sacrifice, offering nearly half a billion dollars in grants—hoping to nudge public pension systems to improve the over $18 billion in unfunded pension obligations. The government entities that promised these retirement benefits to public employees are “on the hook” and contractually obligated to fulfill these promises, which essentially means taxpayers are ultimately responsible for paying for public pension debt and promises.

Public pension reform can be counterintuitive. It demands a departure from entrenched partisan narratives and a willingness to embrace nuance, a combination of political and data-driven solutions. Michigan’s reform journey illustrates the transformative potential of pension reform that accounts for the hurdles and interests of local pension units, offering them a viable solution. Rather than simply paying off public pension debt, Act 202 and Act 166 created a clever mechanism to monitor and target incentives to locally managed pension systems, collaboratively nudging them toward solvency.

Beyond its impact on the retirement security of public workers, Act 202 expanded the awareness and monitoring of pension systems, generating publicly available reports on different pension units. The instituted transparency enables oversight beyond Michigan’s Treasury Department, empowering advocacy groups, public sector unions, and retirees to monitor the solvency and performance of their pension units.

Researchers at Michigan State University were able to leverage the transparency of Act 202 and compile the data into a comprehensive report revealing pertinent public finance trends in the state. For example, the study revealed that most of Michigan’s unfunded pension liabilities are concentrated in cities rather than townships or councils, with 69% of the total unfunded pension liabilities in city pension plans. The public data released by the Treasury Department also enabled researchers to identify more granular trends, such as pension plans sponsored by cities with populations exceeding 200,000 have the highest per capita unfunded pension liabilities, a staggering $4,338 per taxpayer.

The impact that Act 202 had on improving transparency and long-term fiscal resilience played a role in earning Michigan a credit rating upgrade from S&P Global in 2018, moving the state’s credit standing from AA- to AA.

The innovative management and intervention mechanism created by Act 202 and Act 166 should be considered by lawmakers in other states with municipal pension units with comparably dire funding ratios. By creating a monitoring loop within the state, the Treasury Department can now monitor and nudge local municipal pension units back on a path to self-sufficiency and full funding. The closed-loop initiative targets the rehabilitation of retirement units on both ends, pushing accounting practices to avoid generating new debt while also avoiding compounding interest costs by paying off part of the public pension debt early—leveraging present taxpayer funding to avoid even higher taxpayer costs in the future.

11/2/2023: This piece has been updated to add information and clarify the differences between Act 202 of 2017 and Act 166 of 2022.