In a press release yesterday, Arizona Gov. Doug Ducey announced that the credit rating agency Moody’s Investors Service is upgrading Arizona’s credit rating from Aa2 to Aa1, the second-highest rating Moody’s offers. In addition to citing an increased tax base—due in large part to recent economic growth—as the main driver behind this latest change, the rating agency also cited “below average” pension liabilities in the announcement.

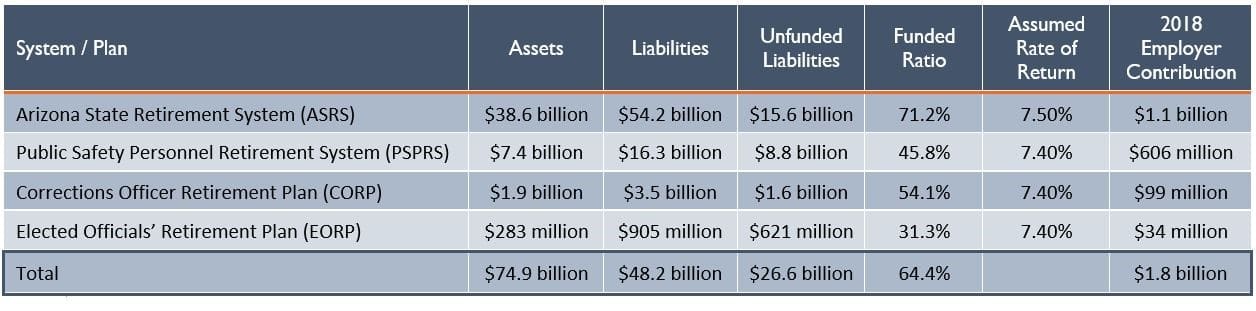

With $27 billion in unfunded pension liabilities today in its four major pension plans—and school districts and local governments struggling to keep up with rising pension costs that are crowding out public service delivery and prompting tax increases—“below average” must be a relative term for Moody’s.

Overall, a credit upgrade is nothing but good news for Arizona and should be celebrated. But citing below-average public pension liabilities as a contributing factor ignores the systemic issues that increased Arizona’s pension debt to historic levels despite a historic, decade-long bull market and prompted several waves of pension reform efforts that are—and, being incomplete, need to remain—ongoing.

Arizona has some daunting pension gaps to close, as illustrated in the following table.

Further, in its most recent annual report on public pension funded ratios, the Center for Retirement Research at Boston College found the average funded ratio across all public pension plans in the U.S. to be at 72.8 percent—a level higher than the Arizona State Retirement System (ASRS), Public Safety Personnel Retirement System (PSPRS), Corrections Officer Retirement Plan (CORP), and Elected Officials’ Retirement Plan (EORP).

Funded ratios aside, other stakeholders who monitor the impact that public pensions have on state finance debt levels also disagree with Moody’s characterization of Arizona’s pension challenges.

The Segal Group, a benefits consulting firm hired by ASRS for an actuarial audit this year, reported to the ASRS board that their modeling suggests ASRS is unlikely to meet its long-term investment return goals. When ASRS, or most other defined-benefit public pension plans, are unable to meet investment return expectations, pension debt levels rise, funded ratios fall, and required contributions from taxpayers increase.

In May, a different ratings agency, Fitch Ratings, released its own report ranking Arizona as the number one risk-taking state when it comes to pension investments, citing Arizona’s 86 percent allocation to equities and alternatives as the highest among U.S. states. The risk-taking isn’t working either, as Fitch ranked Arizona in the bottom-10 worst-performing states in terms of investment performance. With Arizona’s largest public pension plans continuing to rely heavily on unrealistic investment returns, the funded ratio and debt levels will continue to flatline during up-markets and tumble when the market falls.

An analysis published by the Pension Integrity Project at Reason Foundation spotlighted the driving factors leading to ASRS’s poor funding level, including underperforming investments, undervaluing debt, and not properly paying down that debt.

Gov. Ducey and other key public pension stakeholders should celebrate the recent credit upgrade for the savings it will bring to large public works projects and the like across Arizona. But those savings, along with the additional revenue being generated from the state’s economic expansion cited by Moody’s, should be used by policymakers to address the systemic issues the Reason analysis shows are holding Arizona’s largest public pensions back from full funding and long-term solvency.