The Arizona state legislature recently passed Senate Bill 1082, establishing an innovative contribution prefunding program for the state’s pension system for teachers and public workers. The program enables the Arizona State Retirement System’s (ASRS) employers—mostly local governments, universities, and school districts—to voluntarily pre-pay future employer pension contributions, with significant flexibility on how those dollars can be utilized. Employers who contribute to this program will improve their fiscal positions by prepaying their future contributions to enhance their future budget stability while also increasing the funded status of the total fund.

The Arizona State Retirement System is a cost-sharing, multiple-employer plan where participating employer and employee contributions are pooled. All assets, approximately $50 billion, of the plan are shared, pooled for investment, and used to pay for promised pension benefits. Every employer in the state pays the same contribution rate, as a percentage, for each employee. All liabilities are pro rata owned by every employer, who all share in paying for the normal cost and unfunded liabilities of the plan.

Under this fairly common contribution and liability structure, there is no way for any individual employer to “pay down” or accelerate the payment of their portion of unfunded pension liabilities. Any supplemental contributions from one employer would simply accrue to the entire employer pool.

What the passage of the contribution prefunding program (CPP) brings is a novel way for government employers to set aside surplus funds to offset future required contributions, essentially allowing them to budget for lower ASRS payments in the future, while continuing to pay the full contributions now.

The biggest benefit of the CPP is the ability for employer-prefunded contributions to earn the same investment return as the ASRS pension fund. ASRS will grant all pre-funded contributions an earnings rate equal to the actual annual rate of return on the ASRS pension investment portfolio, net of investment expenses. As an example of the return employers could expect to receive on their contributions to the program, ASRS has averaged an annual investment return of just over 9% since plan inception in 1975, although market outlooks in the near term posit a realistic return figure being somewhat lower.

The growth of individual employers’ funds in the contribution prefunding program will help offset future unfunded accrued liability (UAL) cash requirements and help the employer keep budget stability during poor financial times. Instead of having to cut funding to other programs when pension contribution requirements increase, the employer can simply pull dollars from the CPP to offset that increase.

The flexibility in this new program is also an important feature. The application of the money in the CPP is up to the employer, with three stipulations. One, for administrative reasons, the minimum prepayment contribution is $100,000. Two, the dollars must eventually be used to offset future pension contributions. And third, once ASRS reaches full funding and therefore has zero unfunded liabilities to be paid down, the plan will no longer accept additional funds into the CPP.

Apart from that, the employer can choose exactly how and when to use their CPP balances. There is no requirement that the employer must use the funds within a certain time frame, allowing the employer to take advantage of the compounding returns from the ASRS investment portfolio.

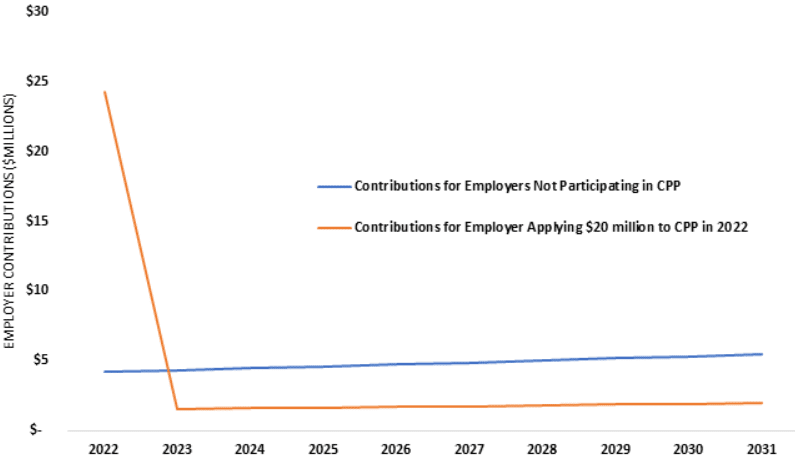

For an example of the possible employer savings from participating in the CPP, we use three hypothetical ASRS employers and assume each plan has a $100 million unfunded liability. For the purposes of this analysis, we assume:

- Each employer’s payroll begins at $52 million and grows at 3% per year.

- Employers have a payroll contribution of 8% to pay down the UAL.

- Two employers choose not to contribute any dollars to the CPP.

- The other employer chooses to contribute $20 million to the CPP in 2022.

- The CPP employer wants to amortize (use the dollars in the CPP) over a 10-year period to help offset future contribution requirements.

- CPP contributions are assumed to grow at ASRS assumed annual rate of 7%.

For the employers who decided not to join the contribution prefunding program, their 10-year total contributions would be $48,245,443. For the employer who decided to contribute $20 million to the CPP, and use those funds to offset future contributions, their 10-year total contribution would be $40,248,304. The annual contribution amounts are seen in the chart below.

Contributions for Hypothetical ASRS Employer

Under this scenario, the employers who neglect to join the CPP would pay roughly $8 million more over just that 10-year period. This is due to the compounding interest discussed earlier. The CPP employer’s $20 million, minus the amount used to offset each year’s contributions, is gaining 7% interest compounded annually.

Senate Bill 1082 is a win for Arizona, the Arizona State Retirement System, government employers, and taxpayers. It is another important step forward in the successful and ongoing process of improving the state’s public retirement systems. With the wave of investment volatility and the costs of the average pension plan rising, these prefunding programs could allow employers some desirable flexibility and budget stability as it relates to pension costs.