Foreword

A recurring premise in public management suggests that fiscal resources possess infinite elasticity, or that the State has no intrinsic limits on its level of spending. However, reality dictates that the public sector has no autonomous capacity to generate revenue; instead, public revenue must be extracted from taxpayers. Revenue can be extracted immediately through current taxes or in a deferred manner through issuing public debt, which represents a long-term tax liability. Ultimately, every state expenditure comes from the wealth generated by the productive actors of the nation.

Economic science is founded on the principle of resource scarcity, a basic concept that, paradoxically, is often omitted in the design of public policies under the belief that it is possible to increase the tax burden indefinitely without affecting the tax base. Argentina represents a paradigm of the consequences derived from this logic: An excessive tax burden has led a nation that showed signs of being a world power at the beginning of the 20th century through a long process of retrogression toward the tier of countries people refer to as “undeveloped.” Argentina’s case is not isolated, as globally there is a trend toward an increase in public spending relative to total output, which leads to a corresponding rise in the tax burden. As governments consume more of a nation’s resources, investment and employment decline, people turn toward informality, and capital flight accelerates toward more competitive jurisdictions—thus undermining both present and future tax collection.

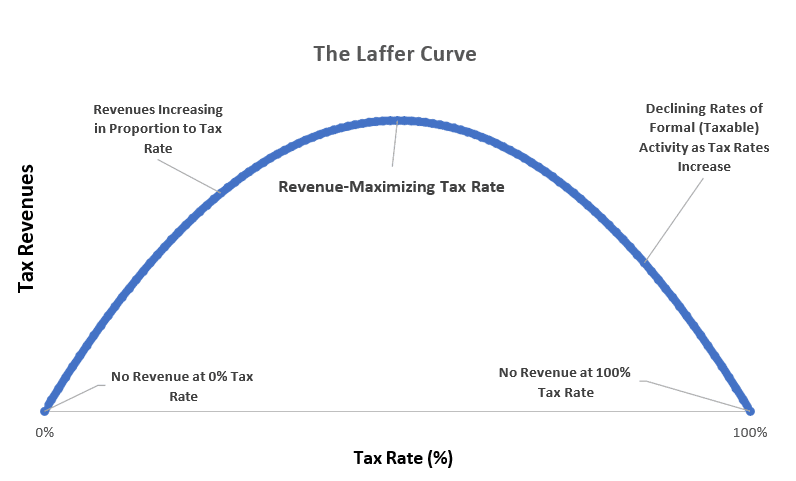

It is remarkable that, more than half a century after Dr. Arthur Laffer empirically demonstrated that excessively high levels of taxation can result in a reduction in public revenues, his postulate continues to be ignored by various decision-makers or their advisors, whether due to technical omission or political convenience.

In this context, Geoffrey Lawrence’s research acquires fundamental relevance by validating the conceptual soundness of the “Laffer Curve” through the analysis of specific data from the Republic of Argentina. His work both quantifies the effect of Argentina’s high tax rates on discouraging private-sector activity and uses Argentina as a “natural laboratory” to corroborate the validity of the Laffer Curve concept in empirical reality. Consequently, the present work constitutes essential reading both for economics students and for professionals with responsibilities in the management of public resources. Likewise, its final recommendations offer a critical roadmap for political and technical leadership, providing essential conclusions for the design of the necessary tax reforms that would allow the reversal of decades of structural stagnation in Argentina.

Aldo Abram

Executive Director, Libertad y Progreso

Executive summary

Argentina’s economic trajectory over the past century serves as a cautionary tale of how misguided policies can erode prosperity. Once among the world’s wealthiest nations, with per capita income surpassing France and Germany in 1910 and attracting waves of European migrants, Argentina now grapples with stagnation, hyperinflation, and widespread poverty. Today, Argentina trails regional neighbors like Chile and Uruguay in output per capita, and more than half its population is mired in poverty.

Very recently, Argentina grappled with the world’s highest rate of inflation, as it has many times over the past several decades. This prolonged economic decline stems from a persistent structural imbalance in public finances, where recurrent fiscal deficits have been financed through money printing. However, inflation is not the only factor of macroeconomic importance in Argentina. The country’s tax system is also profoundly distortionary and punitive to the extent that a large share of economic activity has fled to the underground to avoid these taxes. Nearly half the workforce works in informal, underground markets.

Of the 155 total levies assessed at the federal, provincial, and local levels, just seven account for 87% of all public revenues. This includes a value-added tax (VAT), payroll taxes, corporate and personal income taxes, provincial gross receipts taxes, a financial transaction tax, export duties, and import tariffs. Overlapping tax levies combine to impose an average corporate tax burden exceeding 106% of earnings, rendering full compliance impossible and eliminating all incentive for entrepreneurship. According to World Bank data, this is the second-highest effective corporate tax burden in the world out of the 238 countries for which it compiles data, behind only Comoros. For 197 of these countries, the effective corporate tax rate is less than 50% of earnings.

Due to the onerous tax burden, many firms and businesses simply opt out of the legal economy and operate clandestinely. Informality afflicts 44.1% of the employed workforce. Workers and firms opt for cash-based, unregistered arrangements to evade punitive levies, but these arrangements hinder economic growth. Unregistered businesses may not have access to courts to settle disputes, they have limited access to capital, and they cannot operate as efficiently as legal firms. As a result, labor productivity and real wages have stagnated.

Argentina’s high payroll taxes and cascading levies create a tax wedge between formal and informal employment arrangements. When combined with labor mandates like mandatory annual bonuses and generous severance rules, these costs add 97% to the cost of legal employment beyond wages—far exceeding the Latin American average of 19%. Both firms and workers may realize a financial gain by agreeing to an unregistered employment relationship to avoid these taxes, resulting in a shrinking of the tax base.

The Laffer Curve is an appropriate conceptual lens for Argentina. It illustrates that tax revenues peak at an optimal rate beyond which evasion or a reduction in effort shrinks the taxable base. Empirical analysis, leveraging variations in provincial gross receipts taxes and household survey data from 2022-2025, confirms Argentina’s tax rates are beyond the revenue-maximizing level in key sectors. Based on the empirical analysis, it’s possible to impute the actual revenue-maximizing tax rates, and they are substantially lower than the rates currently in effect in Argentina. Large hypothetical tax cuts modeled herein would theoretically yield roughly equal tax revenues by incentivizing Argentine businesses and workers to re-enter the formal economy.

However, any program of tax reform should be guided by fundamental principles of sound tax policy, including simplicity, transparency, and neutrality. Taxes should not cascade, or “pyramid” up the supply chain, and should consider the taxpayer’s wherewithal to pay. Argentina’s tax system violates these principles in many ways, especially through gross receipts taxes and taxes designed to make international buyers and sellers less attractive for Argentine businesses and consumers.

This study outlines a roadmap to tax reform using an iterative, data-driven approach in which each phase of reform is dependent upon a successful private-sector response to the prior phase. This approach mitigates risks by allowing behavioral changes to unfold gradually. The key components include the replacement of gross receipts taxes with retail sales taxes and the reduction of the VAT in a revenue-neutral manner.

Second, the broader revenue-sharing structure between federal and provincial governments must be reformed to realign taxing authority with spending authority. This recommendation aligns with Libertad y Progreso’s proposals to devolve the administration of personal income and certain other taxes to the provincial level rather than routing these taxes to the federal government and subsequently distributing the revenues to provinces. A temporary stabilization fund could be used to hold harmless provinces that currently benefit from enhanced distributions.

Third, taxes that isolate Argentina from international markets, including export duties and import tariffs (within MERCOSUR constraints) should be sequenced out.

Finally, longer-term reforms should see income and payroll tax rates reduced as revenues from surviving tax instruments grow. These tax reforms would more effectively induce formalization if accompanied by major reforms in the pension system that condition the receipt of benefits on contributions and a relaxation of labor mandates that make formal employment more costly than informal employment.

The linchpin to economic transformation in Argentina is to bring Argentines out of the shadows and into the formal economy, where they can contribute openly, access capital, and build productive supply chains. This would lead to greater public revenues through expansion of the tax base despite fewer overall taxes.

Moreover, it would represent a profound cultural shift in a country where people have escaped to the unmonitored margins of society. It would allow Argentines to slowly rebuild cultural norms of mutual trust and transparency that have been eroded by decades of policies forcing people to hide their lives and incomes.

By fostering an environment where legality yields rewards rather than penalties, Argentina can reclaim its heritage of opportunity, ushering in sustained prosperity for future generations.

Full Report: Out of the shadows: Tax reforms to formalize Argentina’s underground economy