The COVID-19 recession is putting large fiscal stress on state governments, including major negative impacts on their transportation budgets and underfunded pension systems. One tool that may help is called asset monetization, sometimes referred to as infrastructure asset recycling. As practiced in Australia and several other countries, the concept is for a government to sell or lease revenue-producing assets, unlocking their asset values to be used for other high-priority public purposes. The asset continues in operation under new professional management.

This study focuses on the potential of state-owned toll roads as candidates for this kind of monetization. There have been five U.S. leases of toll roads under a long-term public-private partnership concession agreement.

The best-known of these are the public-private partnership (P3) leases of the Chicago Skyway and the Indiana Toll Road. Although both of those toll facilities are part of the Interstate Highway System, like all of that system, they are not federally owned: the Skyway is owned by the city of Chicago and the Toll Road is owned by the state of Indiana. In both cases the entire set of lease payments was made in a lump sum at the start of the long-term concession term, providing a major windfall that was used in the first case to pay down debt and in the second case for major capital investment in other highways.

This study explores the potential of long-term P3 leases of nine state-owned toll road systems:

- Florida’s Turnpike

- Illinois Tollway

- Kansas Turnpike

- Massachusetts Turnpike

- New Jersey Turnpike

- New York Thruway

- Ohio Turnpike

- Oklahoma Turnpike

- Pennsylvania Turnpike

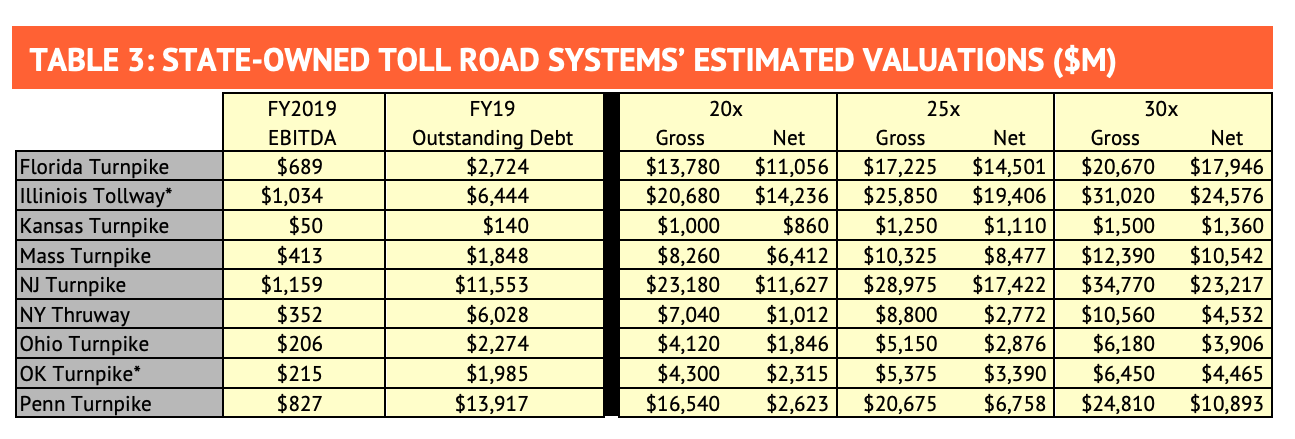

The study draws on data from a number of overseas toll road P3 transactions in recent years to estimate what each toll road system might be worth to infrastructure investors. The gross valuation is what would apply globally. But in the United States, a change of control (such as a long-term lease) requires that existing tax-exempt bonds be paid off. Hence, the net value of each toll road is the gross value minus the value of its outstanding bonds. The estimated net values in this study ranged from $1.1 billion to $19.4 billion.

Since P3 toll road leases are still uncommon in the United States, this study provides a brief history of long-term franchises for investor-financed toll roads. It then discusses the three categories of likely investors in U.S. toll roads.

First is the growing number of global toll road companies that operate extensively in Europe, Latin America, Australia, and Asia. The second group is numerous infrastructure investment funds that have raised over $1 trillion to invest in revenue-generating infrastructure during the last 15 years. And the third category is public pension funds, which have been increasing their investments in infrastructure in recent years, seeking to reverse the decline in their overall rates of return on investment.

All three types of investors have long time horizons and are comfortable investing in and further developing assets such as toll roads.

The study explains that if the proceeds from the lease of a toll road area are paid in a lump sum upfront (as often occurs), that windfall should be used to strengthen the state’s balance sheet, rather than being used for short-term operating needs. It discusses three potential uses:

• Invest the proceeds in needed but un-budgeted infrastructure;

• Use the proceeds to pay down existing state debt, potentially improving the state’s bond rating; and,

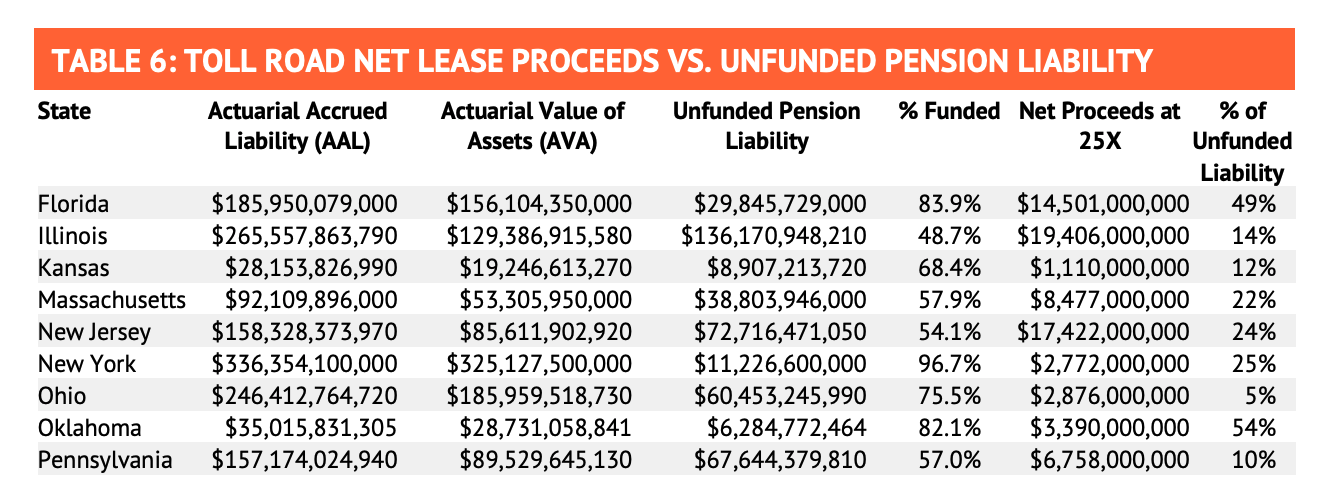

• Use the proceeds to reduce the state’s unfunded pension system liabilities. On the last of these points, the study compares the estimated net toll road P3 lease proceeds with the state’s unfunded pension system liabilities.

If, on the other hand, the lease payments are made annually over the long term of the lease, they would constitute a kind of annuity that could be dedicated to an ongoing purpose such as transportation infrastructure.

The relative attractiveness of using lease proceeds for each of the above purposes will likely depend on the specific situation and needs of the state in question. A state with a pressing need for an unfunded infrastructure project or program may find that use the most attractive, while a state where unfunded pension liabilities threaten either large tax increases or something akin to bankruptcy may prefer using its toll road windfall to shore up its pension system.

The study’s first section reviews the long history of investor-owned turnpikes, the invention of the superhighway in Europe, and the revival there of the investor-owned turnpike model after World War II.

Part 2 then explains the adaptation of this model in the United States, via long-term public-private partnership (P3) projects for new highway projects, as well as five cases of P3 leases of existing U.S. toll roads.

Part 3 compares and contrasts the state toll agency model and the investor-financed long- term P3 lease model on a number of dimensions.

Part 4 then draws on international data to estimate the potential lease value of the nine state-owned toll road systems selected for this study.

And Part 5 provides information on the three categories of investors that typically form consortia to bid on such P3 leases: global toll road companies, infrastructure investment funds, and public pension funds.

Part 6 takes a closer look at the potential role of pension funds as toll road investors, suggesting that their participation could alter the politics of this category of asset recycling.

And Part 7 provides U.S. examples of the three principal uses of the proceeds of long-term toll road P3 leases.

This study finds that, based on valuations of overseas toll roads in recent privatization and P3 transactions, the large majority of the nine states studied here would have significant net proceeds after paying off outstanding tax-exempt toll road bonds (as required by U.S. tax law).

Since fiscal prudence dictates that a large windfall be devoted to strengthening a state’s balance sheet, rather than dealing with short-term budget-balancing, states considering leasing their toll road systems should weigh the trade-offs among three alternatives as they work to recover from the COVID-19 recession. The wisest alternatives are to:

- Invest the windfall in needed infrastructure that cannot otherwise be funded in the post-pandemic environment;

- Strengthen the state government’s balance sheet by paying down existing debt, potentially increasing its bond rating by doing so; or

- Put the windfall into the state’s underfunded pension system, bringing that system closer to solvency, while preserving current tax revenue for ongoing government operations.

Alternatively, if lease payments were to be made annually, the most direct use would be as a kind of annuity to support ongoing investment in the state’s transportation system. The best choice will depend on the circumstances each state finds itself in during the economic recovery.

Full Study: Why States Should Lease Their Toll Roads

News Release — Study: States Can Lease Toll Roads to Fund Other Infrastructure, Pay Off Debt

Frequently Asked Questions — Why Should States Consider Leasing Their Toll Roads?