In This Issue:

Articles, Research & Spotlights

- Webinar: Public Finance Experts on Managing State and Local Debt

- California Bills Could Add Major Costs and Risks

- New York’s Pensions at the Center of Budget and Reform Proposals

- Connecticut Pulls Funding from Pensions to Pay for Preschools

News in Brief

Quotable Quotes

Data Highlight

Reason Foundation in the News

Contact the Pension Reform Help Desk

Webinar: How State and Local Governments Can Manage Their $5 Trillion in Debt

State and local governments have a total of over $5 trillion in long-term liabilities, mostly in the form of unfunded public pension obligations, unfunded retiree health care benefits, and bonded debt. Join public finance experts for a discussion on how governments can manage their growing debt costs, fully fund pensions, manage financial risks and improve financial reporting. Speakers include:

—Andy Matthews, Nevada State Controller, and former assemblymember, Nevada Legislature

—Elaine Lu, chair of the Association for Budgeting and Financial Management, and director of the Maxine Goodman Levin School of Urban Affairs at Cleveland State University

—Farhad Omeyr, program director of research and data at the National League of Cities, including NLC’s City Fiscal Conditions reports

— Don Boyd, co-director of the Project on State and Local Government Finance at the University at Albany, SUNY

—Mariana Trujillo, managing director of government finance at Reason Foundation

Date and Time

Thursday, May 21, 2026, and 2:00 pm ET / 11:00 am PT

Register to watch and attend via Zoom here. The panelists will take questions from attendees. Can’t join us live? Register, and we’ll send you the recording.

Legislation in California Could Increase Taxpayers’ Risks and Add Billions in New Costs

California lawmakers are considering several bills that could add major costs and burdens to the state’s already stretched taxpayers. Assembly Bill 1383 would grant a benefit sweetener to public safety workers, repeating some of the state’s past mistakes that created massive pension debts that persist to this day. Reason’s analysis warns that this move could add over $14 billion in new costs over 30 years. Another bill under consideration (Assembly Bill 1054) would create a new benefit for public safety workers who choose to continue working beyond their established retirement age, adding uncertain costs to a state pension system already $179 billion short on funding promises to public workers.

Interactive Analysis: CalPERS Monitor

The Costs of California AB 1383’s Undoing of Pension Reforms

Potential Costs and Risks of Proposed DROP in AB 1054

Lawmakers Should Not Politicize California’s Pension Funds

Mamdani Uses Pension Debt Gimmick To Balance Budget in New York

New York City Mayor Zohran Mamdani released his budget proposal, claiming to have closed the city’s deficit without reducing spending or raising taxes. The bulk of this strategy relies on aid from the state, but it also deploys a pension funding gimmick that will pass higher costs on to future budgets, writes Reason Foundation’s Mariana Trujillo. Mamdani proposes extending the pension debt payment target, delaying projected full funding by five years. This will reduce annual costs today, but the interest on the city’s pension debt will cost taxpayers more in the long term.

New York Doesn’t Have a Public Employee Recruitment and Retention Crisis

How Connecticut’s Pre-K Endowment Raises Pension Costs

Connecticut has made considerable progress in improving its public pension funding since adopting fiscal policies in 2017 to dedicate surplus revenues toward paying down this debt, but a bill passed in 2025 now threatens that progress by diverting some of these funds to pay for early childhood care programs. A new report from the Reason Foundation and the Yankee Institute for Public Policy estimates that the new Early Childhood Education Endowment (ECEE) could divert $300 million from crucial pension funding each year, potentially generating additional long-term costs of up to $900 million. The report also finds that the endowment is unlikely to generate enough to fully pay for the state’s current spending on early childhood education.

News in Brief

How Timely Are States at Reporting on Their Pensions?

A new analysis from Truth in Accounting grades the financial transparency of all states based on their Annual Comprehensive Financial Reports (ACFRs). A part of their grading examines the lag in pension liability numbers reported in state financial reporting. While nearly all public pensions publish their liabilities and funding annually, the timing of these plan-level reports varies. Consequently, many state-level financial reports use figures that may be years out of date. The analysis found that only four states (Indiana, Maryland, Massachusetts, and New Mexico) published annual financial reports that included pension liability data for the same year. It also identified three states (Kansas, Michigan, and Oklahoma) whose annual financial reports include teacher pension liabilities only partially, even though they are major contributors to these plans. Read the full analysis here.

Quotable Pension Quotes

“It puts a framework into statute that future legislators can incrementally sweeten up because of political pressure to make the system more beneficial for the recipients. And that’s a big hazard that’s easy to fall into.”

––Alaska State Sen. James Kaufman (R-Anchorage) on a bill to reopen pension benefits for the state’s public workers in “Alaska Senate budgeters advance overhauled public pension bill, setting up floor vote,” Anchorage Daily News, April 25, 2026.

“We are already paying in 2026 and 2027 for benefits earned almost two decades ago. … To further stretch this out, is asking future New Yorkers, it’s asking taxpayers in fiscal year 2033, 34 to balance today’s budget.”

––Ana Champeny, Citizens Budget Commission vice president for research, quoted in “Mamdani’s counting on pension restructuring to balance the budget. Will the unions let that happen?” City & State New York, May 14, 2026.

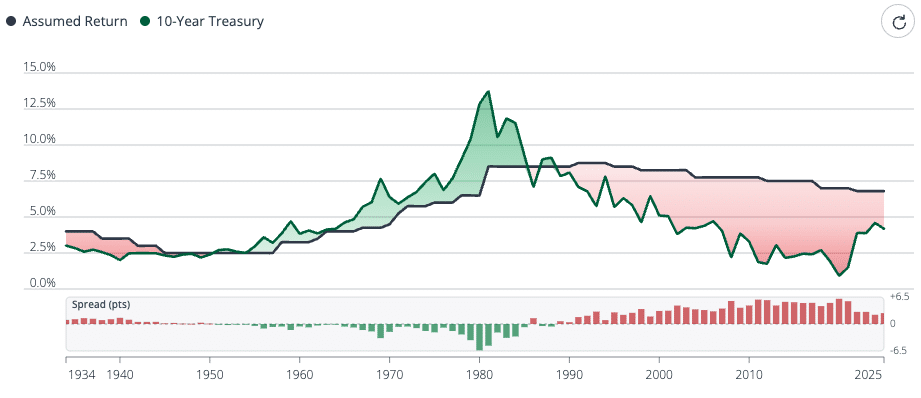

Data Highlight

Reason Foundation’s “CalPERS Monitor” tracks nearly a century of the pension’s investment assumptions in comparison to a 10-year treasury yield (used to measure what is considered a low-risk investment). The analysis illustrates the evolving environment for pensions over the decades. An 8.5% return assumption was once in line with “low-risk” investments, but this has not been the case since the early 1990s. See the analysis here.

CalPERS Assumed Return vs 10-Year Treasury (1934-2025)

Reason Foundation in the News

“Iowa ranked 33rd in the Reason Foundation’s measure of pension investment risk, where a higher ranking indicates greater exposure to higher-risk assets, placing it among the riskier US state retirement systems.”

—Reason Foundation’s Zachary Christensen quoted in “Iowa pension chief resigns amid concerns about performance figures,” Financial Times, May 9, 2026.