This newsletter from the Pension Integrity Project at Reason Foundation highlights articles, research, opinion, and other information related to public pension challenges and reform efforts across the nation. You can find previous editions here.

In This Issue:

Articles, Research & Spotlights

- Proposed Pension Reform in Alaska Comes with Major Risks

- Improving Transparency for Teacher Retirement Sytem of Texas

- ESG Investment Challenges for Public Pension Funds

- Years Like 2021 Are the Exception, Not the Rule, for Investment Returns

- Asset Windfalls Are an Opportunity to Reduce Pension Risk

News in Brief

Quotable Quotes on Pension Reform

Data Highlight

Contact the Pension Reform Help Desk

Articles, Research & Spotlights

Alaska Bill Threatens State’s Pension Progress

In 2005, Alaska policymakers implemented public pension reforms in response to significant pension cost and funding issues. Now, state legislators are considering a pension bill that would undo many of these changes and reestablish a defined benefit pension plan for public safety workers. Analysis shows that this proposed legislation would introduce the state budget to the same risks that existed in the past. In this one-pager, the Pension Integrity Project at Reason Foundation establishes that a successful retirement plan splits the cost of benefits equally between the employee and employer and mitigates risk through realistic investment return assumptions. Since the legislation under consideration in Alaska fails to sufficiently achieve these goals, this proposed reform falls short in establishing a pension plan that would shield the state from significant long-term risks.

Texas’ Teacher Retirement System Needs More Transparency

In 2020, the Texas Sunset Advisory Commission offered several recommendations to improve the security and transparency of the Teacher Retirement System (TRS) of Texas, but legislators have yet to enact them. Reason’s Steven Gassenberger reviews these proposed policies and outlines why they are necessary when using a high-risk investment strategy like that employed by TRS. This analysis also explores the growing need for transparency and details the type of data and public reporting that would effectively implement the recommendations of the commission’s report.

Public Pension Plans Need to Consider the Risks of ESG Investing

Many public pension plans are applying environmental, social, and governance (ESG) investment strategies to avoid assets that are purported to be detrimental to society. In practice, this means institutional investors exclude securities issued by companies engaging in flagged behavior and/or apply ratings to construct an ESG-friendly portfolio. These methods have tradeoffs for pension plans, however. Reason’s Marc Joffe says ESG classifications can be inconsistent and ratings tend to be very subjective and easy to manipulate. What is more, prioritizing environmental, social, and governance interests at the cost of lower returns or reducing risk is a violation of a pension plan’s fiduciary responsibility.

The 2021 fiscal year saw historic investment returns for public pension plans across the country. In this commentary, Reason’s Jordan Campbell notes that several public pension plans are lowering their investment return assumptions, despite the last year’s results far exceeding expectations. Still, some policymakers appear to be considering this as an opportunity for pension benefit increases, which Campbell argues is ill-advised for pension plans that are still facing unfunded liabilities.

Pension Plans Can Use 2021’s Great Returns to Reduce Future Investment Risks

Following a historic year in investment returns, pension plans have an opportunity to strengthen their funds in preparation for the lower investment returns expected going forward. By lowering their assumed rates of returns and their discount rates, pension plans reduce the risk of further accruing unfunded liabilities due to market results below expectations. Using the example of Louisiana’s pension system for public workers, Reason’s Anil Niraula demonstrates how reducing investment return assumptions uncovers hidden costs, but also bolsters the fund from future funding challenges. Waiting to make these adjustments has added significant costs to the Louisiana pension fund and others, so public pension systems should strive to be proactive in adjusting their investment return assumptions.

News in Brief

Analysis Highlights Access and Participation in Public DB and DC Plans

A new issue brief from Mission Square Research Institute uses data from the U.S. Bureau of Labor Statistics to examine the benefits that are offered to state and local public workers. Their analysis finds that 86% of public employees have access to a pension, compared to the 38% who have access to a defined contribution plan. Of those who do have access to a defined contribution benefit, approximately half select this option. On average, employees contribute 7.2% of their pay to the defined benefit plans, while employers pay 11.7% of total employee compensation. The full brief is available here.

Report on Fiscal Status of Cities Singles Out Pension Debt

Truth in Accounting recently released its Fiscal State of the Cities 2022 report, which compiles government financial reporting for the 75 most populous cities in the U.S. Their analysis finds that in 2020 these cities reported $357 billion in total debt, most of which is unfunded pension ($180 billion) and other post-employment benefit ($160 billion) obligations. The report also evaluates the time each city takes to release reporting, counting the days it takes to submit required reporting after the end of their fiscal year. This puts a spotlight on several tardy cities that are 200-to-400 days late to release their 2020 reporting. The full report is available here.

Quotable Quotes on Pension Reform

“Aggressively prepaying at least $1 billion now will save taxpayers hundreds of millions of dollars in debt service — more than $400 million saved over the next five years.”

—Kansas Attorney General Derek Schmidt on proposed legislation to make a supplemental payment into the state’s pension fund, cited in “House Panel Begins Examination of Possibly Transferring $1 Billion into KPERS,” Kansas Reflector, Feb. 9, 2022

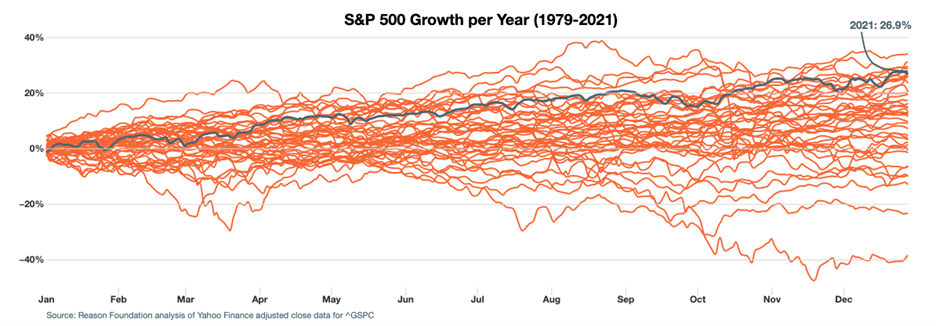

Each month we feature a pension-related chart or infographic of interest generated by our team of Pension Integrity Project analysts. This month, analyst Jordan Campbell created a visualization that shows historic annual S&P 500 growth. This analysis is useful for contextualizing the latest year of pension asset returns with general market trends going back to 1979. You can access the tool here.

Contact the Pension Reform Help Desk

Reason Foundation’s Pension Reform Help Desk provides information on Reason’s work on pension reform and resources for those wishing to pursue pension reform in their states, counties, and cities. Feel free to contact the Reason Pension Reform Help Desk by e-mail at pensionhelpdesk@reason.org.

Follow the discussion on pensions and other governmental reforms at Reason Foundation’s website and on Twitter @ReasonPensions. As we continually strive to improve the publication, please feel free to send your questions, comments, and suggestions to zachary.christensen@reason.org.