Labor unions representing state and local government employees across the country have long supported traditional defined-benefit pension plans for their members to the exclusion of other retirement plan types. While defined-benefit (DB) pensions have many positive qualities and have served some public sector employees well for many years, there is little question that they no longer meet most public employees’ lifetime financial security needs. Actuarial data from the public pension systems themselves bear this out.

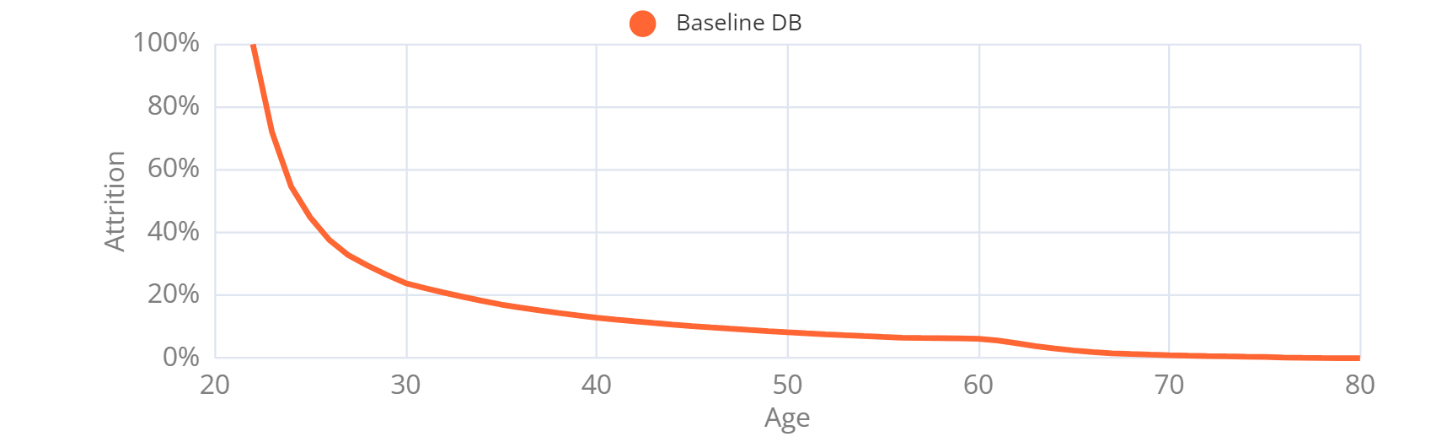

In North Dakota, for example, only 33% of employees beginning service at age 22 still participate in the pension plan at age 27. Employees leaving before the five-year vesting requirement keep only their contributions, lose the employer contributions, and receive no pension benefits. In other words, two-thirds of newly hired North Dakota public employees will receive little or no retirement benefits from their North Dakota public employment once they reach the end of their working careers.

Employee Retention: North Dakota Public Employees Retirement System

Data provided by North Dakota Public Employees Retirement System actuarial reports and compiled by the Pension Integrity Project at Reason Foundation.

The data for public workers looks similar in other states. According to Reason Foundation’s analysis of public reports, the Montana Public Employees Retirement System expects only 30% of employees hired at age 22 to still participate in the system at age 27.

Another example is the school division of the Colorado Public Employees Retirement Association (PERA), where a Pension Integrity Project analysis in 2018 showed that only 37% of Colorado teachers hired at age 25 remain in the system after five years of service.

The reality that state and local government employees have become a more mobile group—frequently switching between several employers during a working career—has been known for years. This pattern is consistent with the broader U.S. employment marketplace, and job mobility is only increasing within the modern workforce. Current employment trends, like working from home, add to this mobility.

So, very few of today’s younger public employees will see a meaningful benefit from participating in a state or local government pension plan. Similar participation patterns in public pension plans throughout careers (i.e., moving from covered employment to non-covered employment or another shorter stay in a different public defined benefit plan) will leave an employee in desperate straits come retirement. Retiring with inadequate savings or benefits from public pension participation will place an even greater burden on personal savings and Social Security. Since many state and local employees do not participate in Social Security, the burden may fall on other publicly funded social service programs.

Given this reality, why do public employee retirement systems, the unions representing state and local government employees, and the organizations that carry their messages continue to advocate for these traditional defined benefit pensions and shun other retirement plan design options? Isn’t it their responsibility to seek solutions that provide adequate retirement benefits (based on the employee’s employment tenure at that employer) to the most employees possible, and shouldn’t it be their objective to secure good post-employment income for all new hires, not just the ones who stay in jobs for decades?

One oft-cited reason these groups give is not a defense of the DB plans but rather a condemnation of defined contribution (DC) plans. They posit pension reform efforts as a binary choice between traditional pensions and 401(k)-like defined contribution arrangements. To their point, there are many reasons to oppose using a typical 401(k) design as a core retirement plan. These could include employee-centered risk, lack of focus on income, and inappropriate and expensive investment choices. The 401(k) was designed to supplement a primary retirement plan in the corporate sector, not to be the entire retirement plan.

A recent National Education Association article promotes some of these points perfectly, but it does not mention that few employees in a defined benefit pension system will stay long enough to see a meaningful retirement benefit. The article also fails to make the distinction that most defined contribution plans for public workers, while often described to be 401(k)-like, are not exactly like 401(k)s and usually do not suffer from the same shortcomings with savings and investment guidance. One novel approach introduced by the Pension Integrity Project is the Personal Retirement Optimization (PRO) Plan, which focuses on meeting individual participant needs while focusing on guaranteed lifetime income.

What public employee advocates often overlook is that there is no reason to frame public retirement plans into a binary framework. Plan designs other than traditional DB pensions or the typical 401(k) DC are available, and some can fit a government’s unique retirement plan needs. Plan sponsors should frame their decisions on what plan design provides the best risk-managed benefit to the broadest number of employees, irrespective of their tenure with that employer. The plan design should also aid the employer in meeting workplace goals. Perhaps the most important is recruiting and retaining quality employees from the marketplace. The plan that positively benefits the most employees is most assuredly the plan that will best meet employer needs as well.

Promoting traditional pensions as the only appropriate retirement system for state and local government employees by unions, plan sponsors, and associated groups may stem from a need for more awareness about how other retirement plan options could benefit so many workers. When considering these crucial pension policy implications, lawmakers and policymakers should focus on long-term financial security for the broadest cohort of public employees. Fortunately, several excellent solutions are available today that would not leave today’s new hires with inadequate retirement savings when they reach that stage.