Nearly seven months after Florida Gov. Ron DeSantis released his “Freedom First Budget” recommending an improved defined contribution retirement benefit for teachers and most public employees statewide, House Bill 5007 (HB 5007), which grants a 3% benefit increase to all active plan members, is now law. Over 180,000 educators, administrators, and other government workers participating in the default Florida Retirement System Investment Plan are slated to receive the additional 3%, effective July 2022.

With this move, Florida continues to demonstrate its commitment to maintaining a retirement system that works for both taxpayers and public workers. It will align the state’s default defined contribution retirement option offered to most newly hired public workers with private-sector retirement contribution best practices. This will have the long-term effect of mitigating financial risk to taxpayers while improving employees’ ability to contribute to a secure, future retirement no matter how long they work in public service.

In combination with previous reforms, the Florida Retirement System Investment Plan (FRS IP) rate changes in House Bill 5007 make Florida a leader in providing attractive, choice-based, and affordable benefits to an increasingly flexible and diverse workforce. The change also improves the footing of the state’s defined contribution plan, which plays a critical role in addressing the financial risks borne by public employers and taxpayers.

The Pension Integrity Project at Reason Foundation played an integral role in thought leadership related to this landmark reform, educating policymakers on the issue for years. After reporting on the needs of the Florida Retirement System (FRS) in 2019, the Pension Integrity Project began communicating the importance of ensuring the benefit offered in the FRS Investment Plan—the state’s default defined contribution plan—meets best practices typical of private sector corporate retirement offerings. From there, we engaged in educational outreach with policymakers, detailing the problem and proposing potential solutions to help bring the FRS Investment Plan up to industry standards.

With the help of several key stakeholders in the state, including Gov. DeSantis’ office, legislative leaders such as State Sen. Jeff Brandes and State Rep. Jay Trumbull, and local groups like Americans for Prosperity-Florida, we were able to raise awareness of the issue in preparation for the 2022 regular session. We most recently testified on the subject before the Florida Senate Committee on Governmental Oversight and Accountability in October 2021. The collaborative effort was rewarded when Gov. DeSantis released his administration’s 2022 budget proposal, which included the recommended policy proposal that ultimately became law with the recent signing of HB 5007.

The Problem

Originally adopted during the 2000 legislative session as an alternative option to the state’s traditional defined benefit pension, the Florida Retirement System Investment Plan (FRS IP) has taken on increasing importance in Florida state and local government administration and now serves as the state’s primary vehicle for providing retirement security to most public workers.

Seeing that most public employees weren’t staying in the system long enough to maximize their pension benefits, Florida lawmakers appropriately switched the FRS IP to be the default choice for most new workers (excluding first responders in the “Special Risk” class) in 2016. Today, over a quarter of the FRS membership has either selected or defaulted into the Investment Plan, and its share continues to grow rapidly.

With so many teachers and public employees dependent on the FRS IP as a means to support a dignified retirement, it is crucial that the default retirement plan provide sufficient contributions to allow workers to make continuous progress toward saving for a healthy and comfortable post-employment lifestyle. Financial advisors and industry experts typically recommend total contributions into a plan like the FRS IP should total at least 10% of an employee’s pay—with many even preferring 12% to 15% percent to ensure benefit adequacy—for the eventual accrued benefits to be sufficient for retirement.

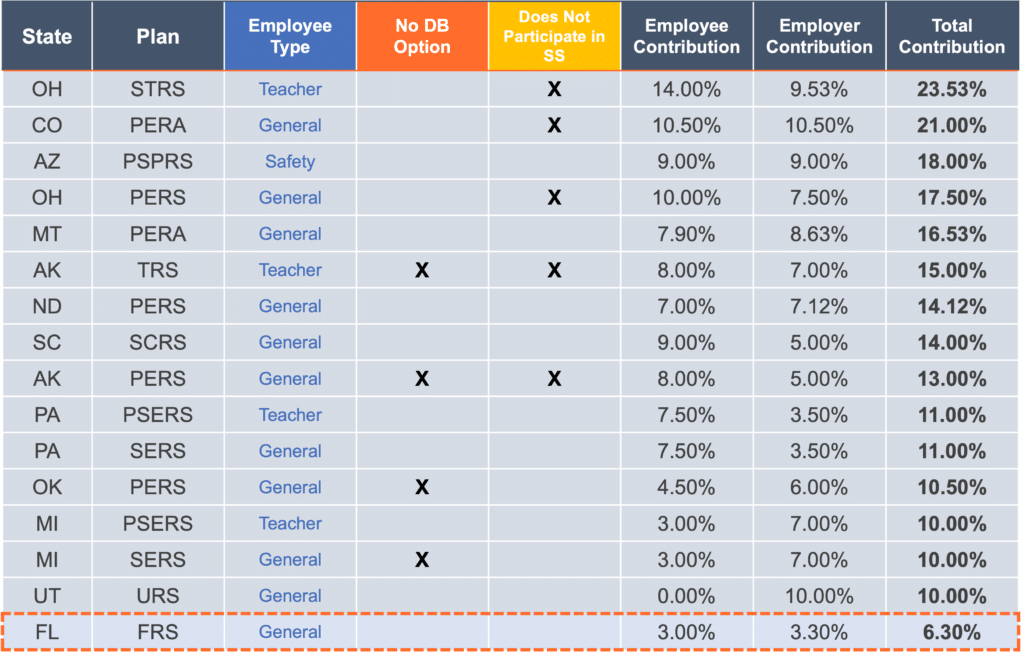

For over two decades, Florida’s public employers at the state and local levels were required to contribute 3.3% of an employee’s salary to their FRS IP account for the largest grouping of employees (the “Regular Class”), which includes teachers and most civilian government employees. Employees in turn contributed a fixed 3% of their pay to their FRS IP account to bring the historic savings rate of FRS IP members to 6.3%, far below industry standards. This contribution combination placed Florida well below other states who offer defined contribution plans, further highlighting the unique need to address the funding flowing into the IP (see Table 1).

Table 1. Contribution Rates for State-Run Primary Defined Contribution Retirement Plans

Insufficient contributions to a public retirement plan should be a major concern for employees, policymakers, and taxpayers alike. A generation of retirees inadequately prepared for retirement creates a risk of increased reliance on the state’s social safety net. This shortcoming also creates more immediate challenges that can impact many stakeholders. Benefits below industry standards and below those available in the private sector can significantly hinder the state’s ability to compete for talent—especially in areas like information technology and data security—to ensure the continued delivery of quality public services to Floridians. Before the governor’s recommendation and the subsequent policy enactment, public employers were at risk of falling behind in attracting qualified employees and creating a generation of retirees with benefits insufficient to outlast them.

The Reform: Summary and Evaluation of HB 5007

For FRS Investment Plan members, HB 5007 increases the employer contribution to employee IP accounts by 3% of payroll over current levels, covering all membership classes, meaning all present and future members of the FRS IP will see an equal increase. The largest grouping of employees—the Regular Class, which includes teachers and most non-public safety workers—will see the employer rates into their IP accounts rise from 3.3% of pay to 6.3%. In combination with their own 3% contribution, which will remain unchanged, the total contribution into the IP plan for Regular Class members will now be 9.3%. Those in the Special Risk class, which includes public safety officers—will see their total contributions rise from 14% to 17%.

According to the House’s fiscal analysis of the House Bill 5007, the 3% increase in employer contributions to the FRS IP is estimated to require an additional $249 million in the first year from all state and local government employers in aggregate.

With the passage of HB 5007, lawmakers have moved the state into a more competitive position by providing employees with more resources to meet their retirement needs. The increased amount employers will contribute to their employees’ FRS IP accounts comes on the heels of lawmakers also agreeing to a 5.38% across-the-board pay increase for public employees. For those participating in the FRS Investment Plan, this will bring the total increase in compensation to more than 8%.

As states around the country scramble to recruit qualified employees, HB 5007 and the FRS Investment Plan will make Florida a more competitive employment option for new workers, especially those highly skilled technical professionals the state expects it will need in the future.

This notable step also improves the long-term viability of the Florida Retirement System. The more the FRS IP membership continues to increase, the less the inherent risk of cost overruns associated with the alternative FRS Pension Plan, which remains $7.6 billion underfunded today. By bringing contributions up closer to industry best practices, HB 5007 ensures that the defined contribution plan will continue to be an attractive option for future public workers. This, in turn, will result in more members joining a retirement plan that, unlike the pension, has a steady and predictable price tag with no risk of runaway costs and debt.

House Bill 5007 also included an unrelated policy provision that expanded law enforcement officers’ access to an existing Deferred Retirement Option Program (DROP) for those participating in the traditional FRS pension system. Reason has not performed an in-depth analysis of this particular aspect of the bill, but there are many risks involved in DROPs that are frequently overlooked, and there are likely more efficient ways to improve the retention of public workers.

Conclusions and Next Pension Reform Steps

Through a collaborative effort grounded in Reason Foundation’s experience with best practices of retirement policy, House Bill 5007 changes the FRS IP in a way that is undeniably important for the long-term future of Florida’s taxpayers and retirees. While the 3% increase appears simple at face value, this reform marks a significant improvement in the retirement security of most incoming workers. It will also improve the ability to attract and keep quality employees at a time when this is a growing concern for state and local employers.

Another important, and quite possibly longest-lasting impact of the reform is that it bolsters the FRS IP so it can continue to be a valuable retirement option for employees while also working for employers—or taxpayers—by managing risks and runaway costs.

Florida policymakers and those involved in this reform process deserve credit for achieving meaningful and lasting change. This should not be the end of thoughtful improvements to the state’s retirement system, however. To build on this session’s success and remain competitive with the private sector, stakeholders should continue searching for ways the FRS IP can better serve public employees.

In the fall of 2021, the Pension Integrity Project testified before the Florida Senate Committee on Governmental Oversight and Accountability that, in addition to addressing the below standard contribution rates, there were a few other opportunities for the FRS IP to better serve its members:

- The first opportunity to expand on HB 5007 lies in the stated objectives of the FRS IP, or lack thereof. Currently, the Florida Retirement System as a whole is governed by a set of objectives, but the unique nature of its two retirement options presents an opportunity for additional mission clarity and transparency. Framing explicit language delineating the specific objectives of the Investment Plan—such as lifetime income and retirement security—could help communicate the goals of the plan to new and existing public workers.

- The second area of opportunity lies in the types of investments offered to those participating in the Investment Plan. Well-designed plans like the FRS IP should also offer the correct age-appropriate investment mix. This is generally accomplished by using target date funds that adjust investment risk to the employee’s retirement horizon. Given the serious role these funds play in the lives of public workers and their families, protecting the value of a member’s FRS IP account from market fluctuations as the worker nears retirement should be a high priority.

- Providing annuities to improve members’ retirement security has long been an established practice in the FRS IP, but it could still be improved. Offering annuitization at retirement allows retirees to use their accrued retirement funds to buy a stream of guaranteed lifetime income. Despite a lifetime annuity option being available to members already, distribution choices offered by the FRS IP are limited. Expanding those offerings to include deferred annuities could present an opportunity to further improve this offering to retirees.

- Lastly, the increases in HB 5007 brought total contributions nearly, but not quite, to the 10% minimum standard set by industry experts. Despite the prudent dedication of funds to address this pressing issue, Florida will still be below all other states in total contributions for most members of the FRS IP. There is still room for improvement in this regard, and it may be prudent to consider ways to increase the fixed employee contribution toward their own retirement. Lawmakers should recognize that with future efforts they can build upon the benefits that will come from this latest legislation.

Although there are still potential improvements to be made to the Florida Retirement System Investment Plan, there is no denying lawmakers took the most important step in HB 5007 by raising total contributions to be closer to the levels needed to provide for an adequate retirement. Gov. Ron DeSantis and members of the state legislature deserve recognition for their work to bring the Florida Retirement System one step closer to becoming a model for public retirement systems around the country.