The interest rate pendulum plays a well-known role in public pension funding. Traditionally, high-interest-rate periods are celebrated for reducing the need to hold riskier investments, offering instead the security of stable returns in fixed-income markets. On the other hand, low-interest-rate environments often compel funds to seek higher investment returns outside fixed income by taking more risk, a practice called “gambling from redemption,” to borrow a term from fiscal policy.

The past decade of near-zero interest rates drove many public pension funds to seek higher-yielding investments. These alternative investments, such as private equity, real estate, high-yield credit, and emerging markets, now comprise one-third of pension assets—substantially increasing from less than the one-tenth allocated to them just two decades ago. The flight to alternatives has been driven mainly by pension funds striving to meet their financial objectives in an era of lower-than-expected returns on traditional investments.

The recent growth in the allocation of alternative investments on pension portfolios raises a question for pension systems, retirees, and taxpayers: Could it change how pension funds are exposed to interest rate risk?

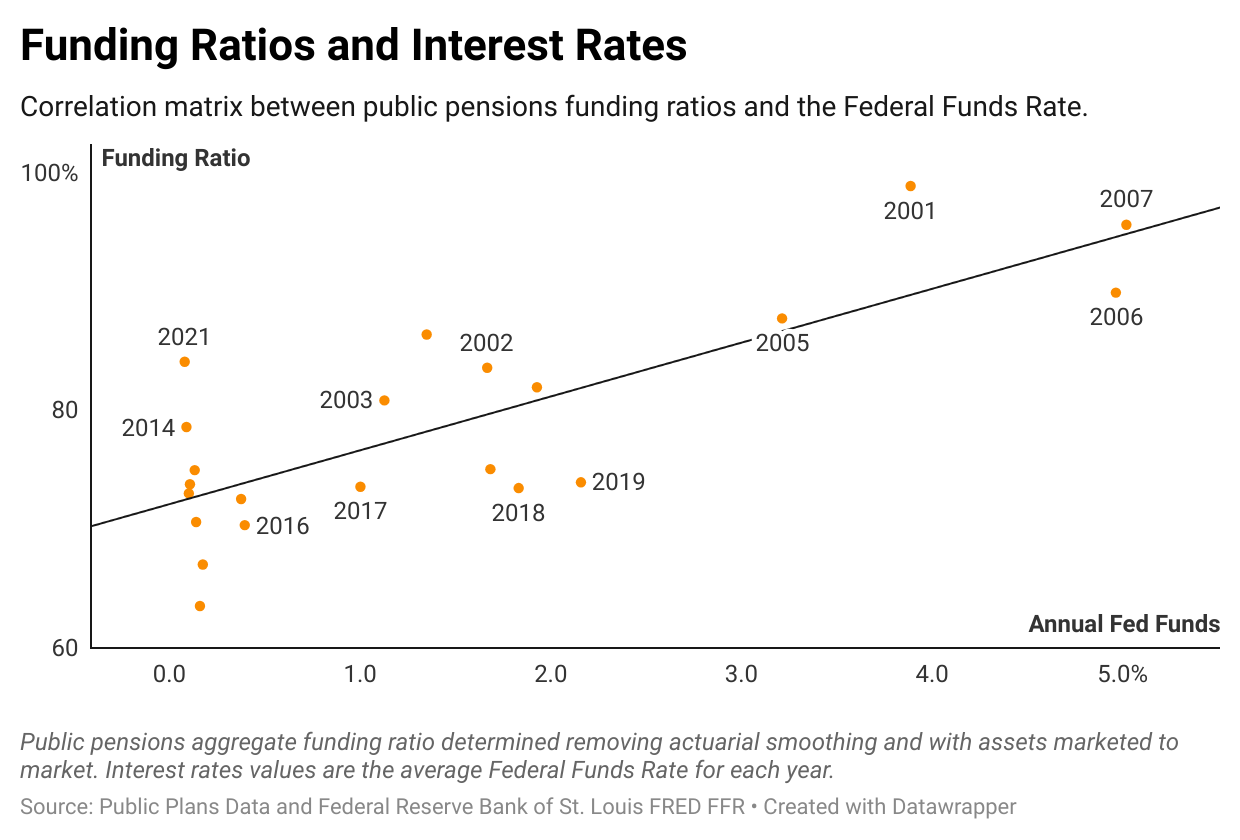

Interest Rate and Public Pension Funding Ratios

Evaluating the past 20 years of annual Federal Funds Rate and public pension funding ratios, a trend becomes evident: interest rates and public pension funding ratios—the ratio of a pension plan’s assets to its liabilities—tend to move together.

Much nuance is needed when evaluating the impact of interest rates on any portfolio. Attributing price correlations to interest rates themselves can be misleading. The Federal Reserve sets rates to be countercyclical, hoping to steer the economy back to an ideal level of inflation and unemployment. Because short-term rates are arbitrarily determined by the Fed in response to markets, interest-rate shifts will correlate with financial cycles and asset prices.

Rather than simply appearing correlated, interest rates are determined by what stage in economic cycles the Federal Reserve perceives the economy is in. Simply, the Federal Reserve is reacting to market conditions when setting rates, and the conditions themselves can have a more significant impact on the portfolio than the rate change, especially as rate expectations are constantly priced in and forecasted in asset pricing. It is essential to take all of this into account and not to mistakenly attribute the asset price fluctuation that led to the shift in rate as its cause.

The correlation between improvements in public pension system funding ratios and high interest rates is mostly attributed to the environment that warrants a hike in rates, the financial booms, rather than the impact of interest rates on asset pricing. At least until recently.

Interest rate shifts impact valuations for some asset classes more than others. Historically, the positive correlation between high interest rates and public pension funding has been evident and indicative of the cyclical nature of contemporary markets. However, the recent surge in alternative investments puts this dynamic into question.

Interest Rate Risk and The Rise of Alternative Investments

One in every three dollars owned by public pension funds is now allocated to assets that tend to be sensitive to interest changes. Alternative investments depreciate sharply in high-interest-rate environments. This shift challenges the traditional wisdom regarding the benefits of high-interest rates for public pension plans, as assets such as real estate, high-yield or distressed credit, and private equity tend to lose value in times of elevated interest rates.

The long-term causal relationship between returns and interest rates is unclear for traditional investments such as corporate equity, bonds, and treasuries—the same skepticism cannot be extended to alternatives.

From mortgaging a two-bedroom house to raising money for a billion-dollar buyout acquisition, high interest rates make it difficult and less attractive to purchase anything, including alternative investments. With the rise in the cost of capital, it becomes increasingly challenging to trade or raise more funding. The drop in buying power, valuations, and liquidity go hand-in-hand.

Beyond constraining potential buyers and reducing valuations, high interest rates also tend to increase the cost of repaying existing debt for firms. Many private equity funds were unhedged against floating rate risk and witnessed the liability agreements made during times of low rates rise significantly in the past year. That has consumed many firms’ liquid margins and profits, not only further lowering valuations but even bankrupting some of those who didn’t have enough revenue to afford the unexpected rise in the interest rates of their loans.

Perhaps most importantly, changes in interest rates lead to a generalized repricing of risk in the market. As the return on treasury notes “trickles down,” the market premium for risk rises as investors become less willing to expose themselves to risks in times of high interest. This dries up all markets, to an extent, but especially for the riskiest assets—such as alternatives.

The largest public pension funds in the country are already seeing the impact of the high interest rate environment on investment returns, signaling potential challenges for pension funds nationwide. For example, the Arizona Public Safety Personnel Retirement System was expecting a return of 16.47% on private equity investments year to date, but amidst high interest rates, the system only realized a return of 1.89%. During the same period, the expectation for public equities was 16.17%, but a return of 15.5% was realized.

The past decade of near-zero interest rates provided venture, real estate, and private equity a prosperous environment for growth—with plenty of liquidity and capital. The recent shift in the interest rate environment has revealed how sensitive alternative investments are to interest rates.

The allocation of pension investments into alternatives might have significantly changed pensions’ exposure to interest rate risk, an effect that might only be revealed retroactively because, due to the nature of private equity and venture capital agreements, investments are locked up until the maturity of the deals, with the actual rate of return often materializing a decade or more in the future.

The evolving landscape of pension investments calls for a reevaluation of assumptions. The rise of alternatives challenges the once-clear relationship between interest rates and pension fund performance. Understanding the material impact in risk exposure of rising high-yield investment strategies is crucial. As such, this trend has been reshaping the retirement landscape across the country, with the real consequences likely to be felt by retirees and taxpayers in the decades to come.

The Impact on Investment Returns and Funding Ratios

Beyond directionality, the growing allocation of riskier and less liquid investments within public pension funds raises concerns about funds’ new sensitivity to interest rate shifts. That is, if interest rates will now have a more significant impact, or correlation, with pension investment returns.

If, indeed, it becomes the case that many of the investments made by funds underperform their expected returns in a high-interest environment, this would decrease overall annual public pension investment returns—and, as a consequence, their assets and funding ratios.

The precise impact of interest rates on pension funds and the broader economy has become increasingly challenging to estimate. But, in the wake of this surge in alternative investments, the conventional wisdom of public pensions benefiting from interest rate hikes is becoming less convincing.

If new investment trends increase public pension funds’ exposure to interest rates, this could increase the risk of public pension systems failing to meet their often overly-optimistic investment return expectations, burdening current plan members and future generations of taxpayers with even larger unfunded liabilities than expected.