Dallas Mayor Pro Tem Tennell Atkins recently appointed the Ad Hoc Committee on Pensions to consider strategies to address the Dallas Police and Fire Pension System’s $3 billion of unfunded liabilities. Among the proposals to alleviate Dallas’ financial burden and secure the retirement of police plan members, interested parties are considering leveraging the pension debt by issuing pension obligation bonds.

A pension obligation bond is a taxable municipal bond issued to pay off public pension debt. The proceeds are invested in the market in the hopes the investment returns are higher than the interest paid to borrow the money. The upside, commonly referred to as “arbitrage,” is set to enable pension funds to profit from the spread between the principal’s investment returns and the interest paid for borrowing it.

The Myth of Debt Refinancing

A memorandum presented by the mayor’s committee cited the main concern with issuing a pension obligation bond (POB) as the “current interest rates.” Indeed, the current high-rate environment poses a significant threat to the profitability of pension bonds, but interest rate risk is just the first half of POB’s arbitrage spread risk.

When pitched by underwriters, pension obligation bonds are often misrepresented as a means of “refinancing your debt.” It might sound like POBs are exchanging the assumed rate of return, the “interest” on their debt, for a lower fixed rate (bond yield). That is not the case.

A pension obligation bond is a bet that by investing the money borrowed, a pension can make more than the interest they will need to pay. It is not like refinancing a mortgage; instead, it is analogous to taking out a second mortgage and investing the money on the stock market in hopes of making enough to use the net gains to pay off the original mortgage.

A pension obligation bond is not an interest refinance or an interest swap; it is leverage. A swap would entail a complete exchange of cash flows on a fixed rate for a variable one. POBs do not release pensions from the compounding of the investment rate “interest” on their liabilities, the original mortgage. The variable investment return and market risk, therefore, is not forgone; it is amplified.

Therefore, the risk is that interest rates will rise and investment returns won’t meet expectations. In practice, these bonds are a financial bet, a leverage on the investment portfolios, hoping to boost revenue to pay off unfunded liabilities.

Financial leverage is a widespread practice across financial markets. It is not inherently irresponsible. It is commonly used by speculative and actively managed investment funds desiring to take on positions more prominent than their current assets allow, hoping to reach extraordinary gains—and willing to tolerate extraordinary losses. Leverage amplifies the size of one’s investment, implying POBs are not swapping but, in reality, increasing exposure to investment risk.

The Funding Threat: The Inversion of Spreads

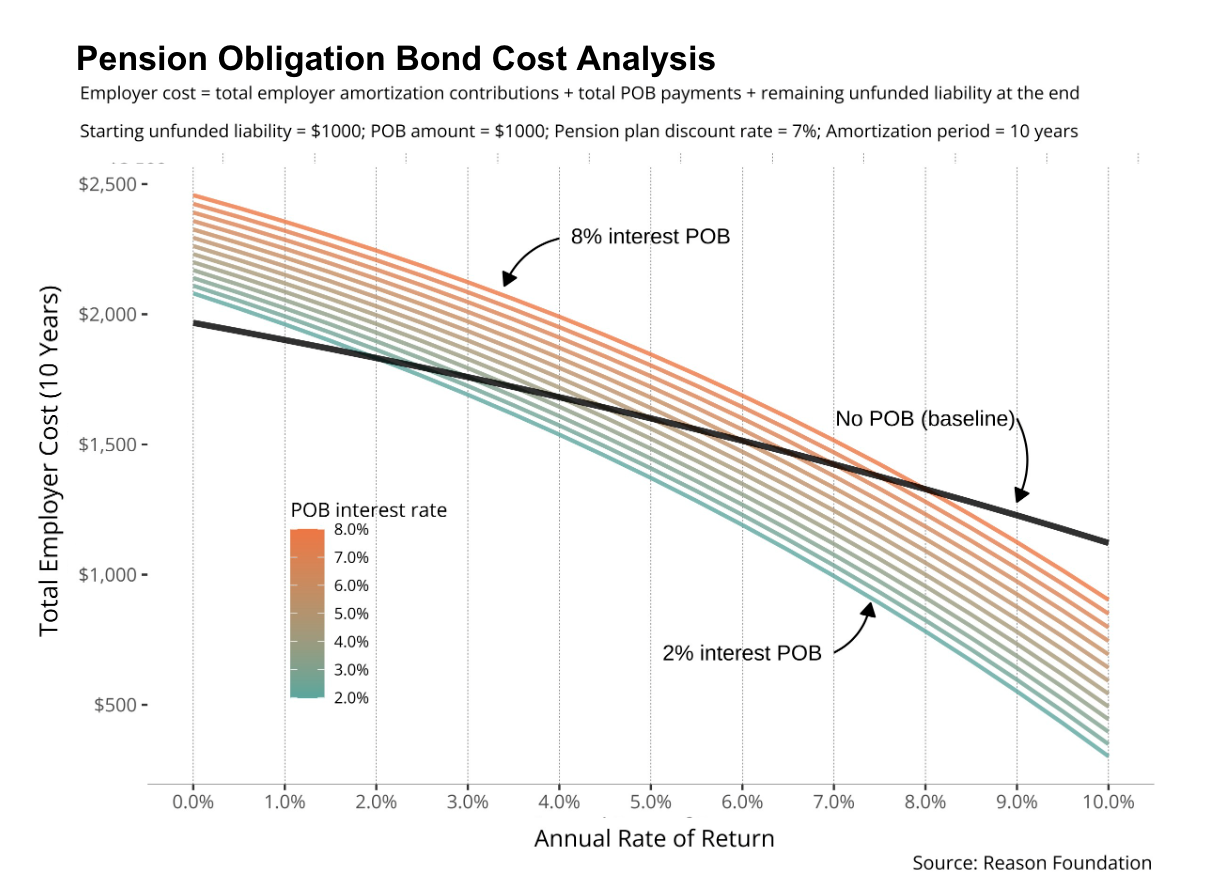

If the effective interest rate on the pension obligation bond is 5%, and a fund invests the lump sum proceeds raised expecting to earn a 7% return on investment, the spread of 7% – 5% = 2% is a novel profit that can aid in repaying the unfunded liability. Of course, the risk is if actual investment returns are lower than expected, say 4%, then the POB results in a loss of 4% – 5% = -1%, leading to an increase in costs and potentially the unfunded liability itself—an inversion of the spread.

The higher the interest rate in the pension obligation bond, the lower the chance of the POB reducing costs—and the higher the chances of it leading to a reversal of spreads, causing an unintended increase in pension debt.

Pension debt is, in itself, different from a mortgage or a car loan. Pension debt is an estimate. It is a very well-constructed guess, an estimation of how much pension funds would need today to cover promised retirement benefits fully. Even “paying off” the unfunded liabilities does not release its issuer from the liability itself. Reaching full funding status relies on all assumptions being met, enabling the plan to pay off the promised retirement benefits appropriately. This is a significant “if,” considering one of the main reasons American public pension funds grew underfunded for the past 20 years were deviations from actuarial and investment expectations.

Funding Ratio Illusions

Pension obligation bonds can lead to a misleading improvement in the funding ratio. They are not factored in as “accrued liabilities,” the present value of retirement benefits, as they are not part of the fund’s owed retirement benefits. In parallel, the assets purchased with the bond proceeds are factored into the funding ratio. Therefore, assets purchased with a POB can appear to generate the impact a grant would have on the funding ratio, but make no mistake, the fund still owes back the bond principal and coupon.

A pension’s funding ratio is the ratio of the plan’s assets to its liabilities (assets / accrued retirement liabilities = funding ratio). A value under 100% indicates that the projected value of the assets owned is not enough to cover the benefits promised; a value over 100% indicates the opposite: there are more assets than expected to be needed to cover the retirement obligations to members.

POBs are a liability to the employer, in this case, the government. They are an additional liability—as the promised retirement benefits are still owed, but the bond payments are now also owed. The revenue raised through the bonds is converted into assets for the pension fund in the hopes the arbitrage rate of return the novel assets will yield is higher than the interest paid for the bonds, leading to a net gain in assets.

With the proceeds from the bond issuance, funding ratios would immediately improve—not accounting for the obligation to pay back the amount borrowed through the bond eventually.

Concern Is Consensus

The emission of POBs is widely cautioned by academics and analysts from a multitude of backgrounds. Reports from S&P Global, Pew Trust, and the Center for Retirement Research at Boston College have analyzed historical outcomes and raised pertinent concerns against their issuance.

The Government Finance Officers Association condemns the practice, declaring that “State and local governments should not issue POBs” and citing five main concerns:

- Spread Risk: “The invested POB proceeds might fail to earn more than the interest rate owed over the term of the bonds, leading to increased overall liabilities for the government.”

- A Robust Risk Management Operation: “POBs are complex instruments that carry considerable risk […], which must be intensively scrutinized as these embedded products can introduce counterparty risk, credit risk, and interest rate risk.”

- Opportunity Cost of Debt: “Issuing taxable debt to fund the pension liability increases the jurisdiction’s bonded debt burden and potentially uses up debt capacity that could be used for other purposes”.

- Funding Cost Risk: “POBs are frequently structured in a manner that defers the principal payments or extends repayment over a period longer than the actuarial amortization period, thereby increasing the sponsor’s overall costs.”

- Credit Rating Risk: “Rating agencies may not view the proposed issuance of POBs as credit positive, particularly if the issuance is not part of a more comprehensive plan to address pension funding shortfalls.”

A Leveraged Bet

Pension obligation bonds pose a delicate spread that can reduce or increase a pension unit’s long-term costs depending on how the market unravels. It is a complex and highly speculative practice that does not replace the need for sound pension reform. A municipal bond issuance does not correct inappropriate state and employee contribution schemes or imprecise financial assumptions. The ruptures that created the unfunded liability remain—as convenient as it would be if they didn’t.

As stakeholders discuss viable proposals to address unfunded liabilities in Dallas, the speculative risk and funding nature of pension obligation bonds must be recognized. As correctly identified by the mayor’s ad hoc retirement committee, the spread-reversal risks of POBs are heightened in times of high interest rates with uncertain forecasts—escalating the risk of the bond leading to an increase, rather than a decrease, in the long-term costs of unfunded liabilities. The additional risk of investment returns not unraveling as expected and the illusory effect POBs have on funding ratios must also be recognized.

POBs are not a refinancing of pension debt. They are a mechanism that enables funds to leverage the fiscal credibility of their municipalities to borrow and reinvest in the market to make an investment profit on the spread. Like taking on a second mortgage to invest in the stock market in hopes of making enough to pay off the original, pension obligation bonds are an additional liability of pension units—a speculative mechanism to increase a pension unit’s exposure to investment profits and losses.