The University of Waterloo and Stand.earth, an environmental advocacy group, released a report in June claiming that the aggregate of six large U.S. public pension funds would have equity portfolios 13% higher if they had divested from publicly traded energy stocks from 2013 to 2022. This analysis uses an inappropriately limited timeframe, however, and thus should not be used as a justification to insert environmental policy into crucial retirement investment decisions.

The report concludes:

The results of the analyses demonstrate that the cumulative value of the company equity portfolio of pension funds would have been higher if they had divested from the energy sector ten years ago. The 22 average difference between the reference portfolio and the ex-energy portfolio is 13 percentage points. Even in a three-year perspective, the cumulative value of the ex-energy portfolios is only 2 percentage points smaller than the value of the original portfolios. However, share prices in the energy sector increased significantly. For the six funds analyzed using data obtained from the Bloomberg database, the total value of the ex-energy portfolios would have been $424.6 billion, while the value of the reference portfolios was $402.8 billion.

If the conclusion of this report held true over a long historical period spanning decades, it would be logical to discourage energy stocks. Of course, the period of analysis matters, and relying on short-term data to rationalize divestment decisions is unwise for public pension funds. The report even admits that looking at the most recent three years of results, the value of this hypothetical ex-energy portfolio is 2% lower than the original portfolios.

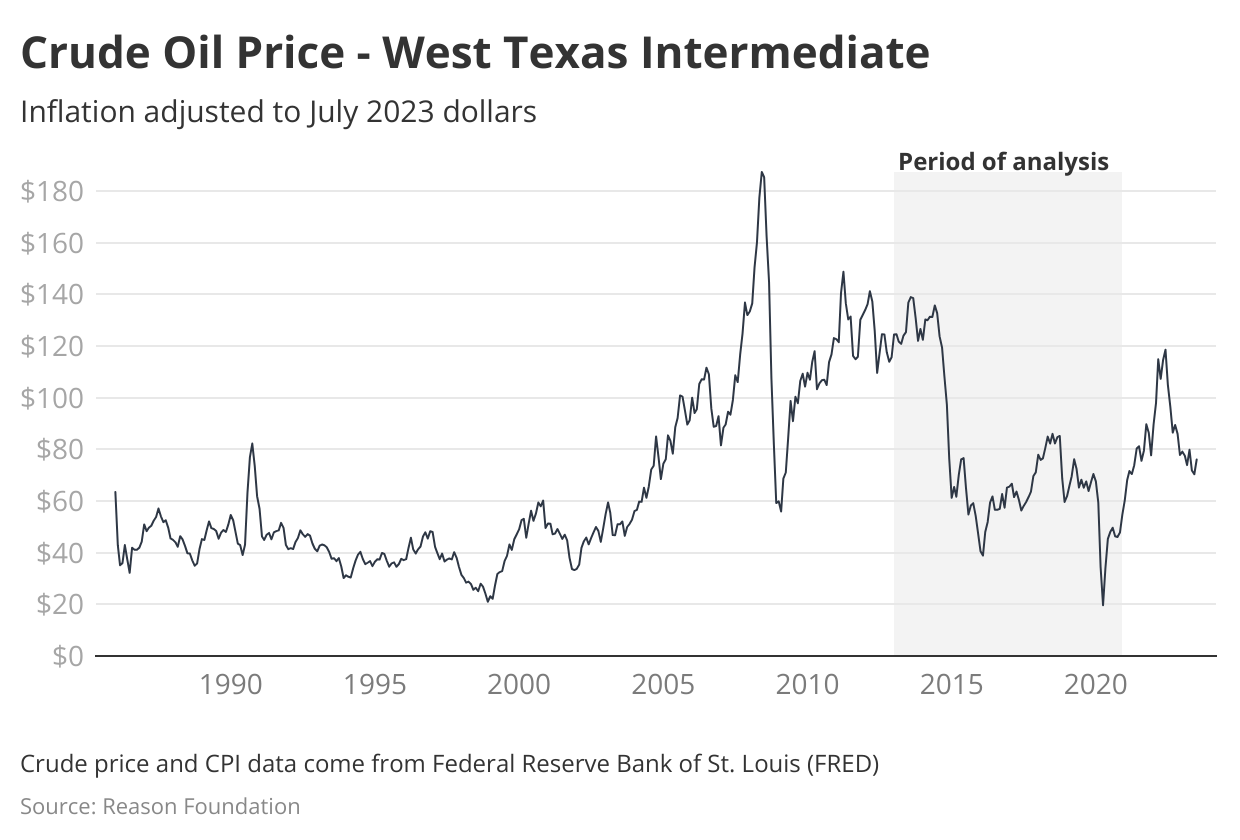

The poor performance of energy portfolios over the last decade is not surprising. This timeframe (2013 to 2022) includes a significant drop in the price of oil. Over the previous 10 years, West Texas Intermediate (WTI) crude oil prices declined dramatically, going from $124 per barrel to $78 per barrel in inflation-adjusted dollars.

Therefore, not surprisingly, when looking at the energy sector by industry, it’s clear that the oil and gas sectors were a consistent drag on performance over the 10 years the report chose.

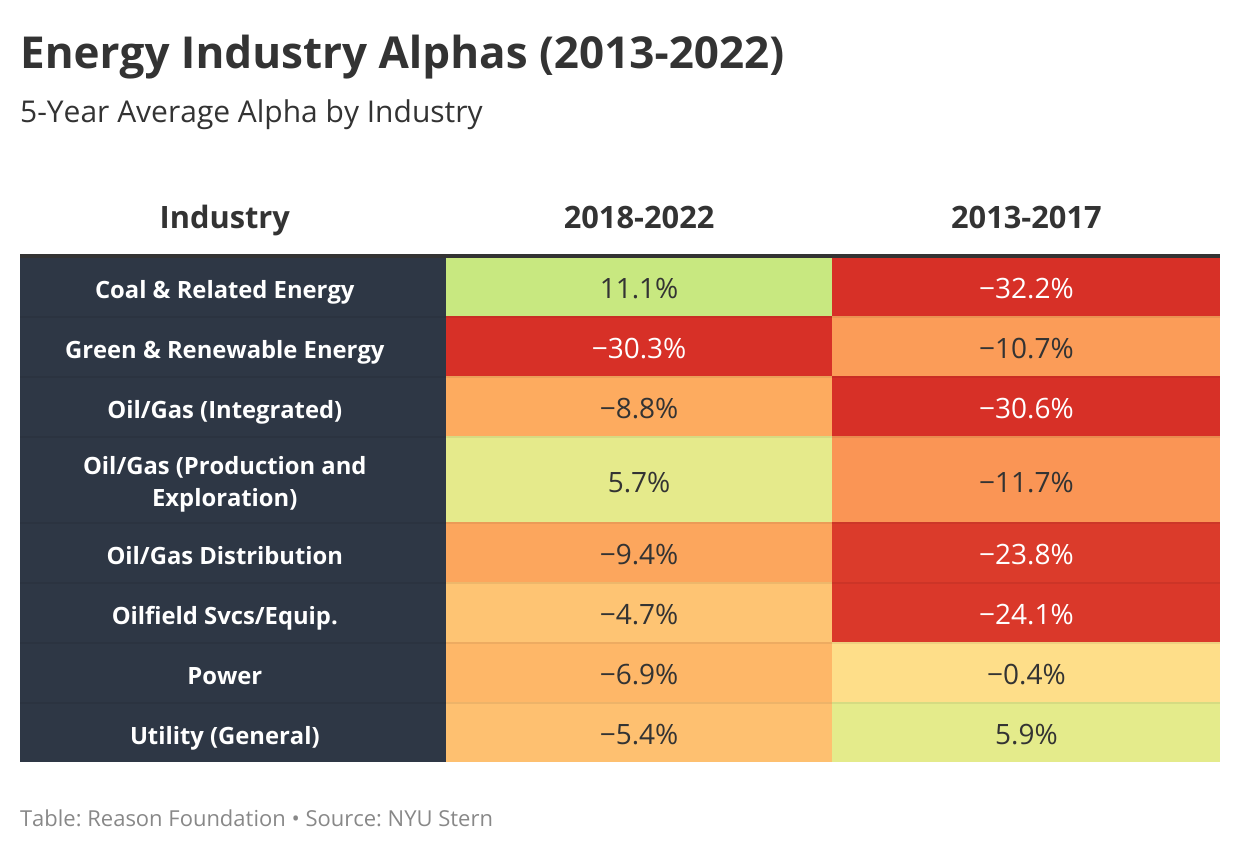

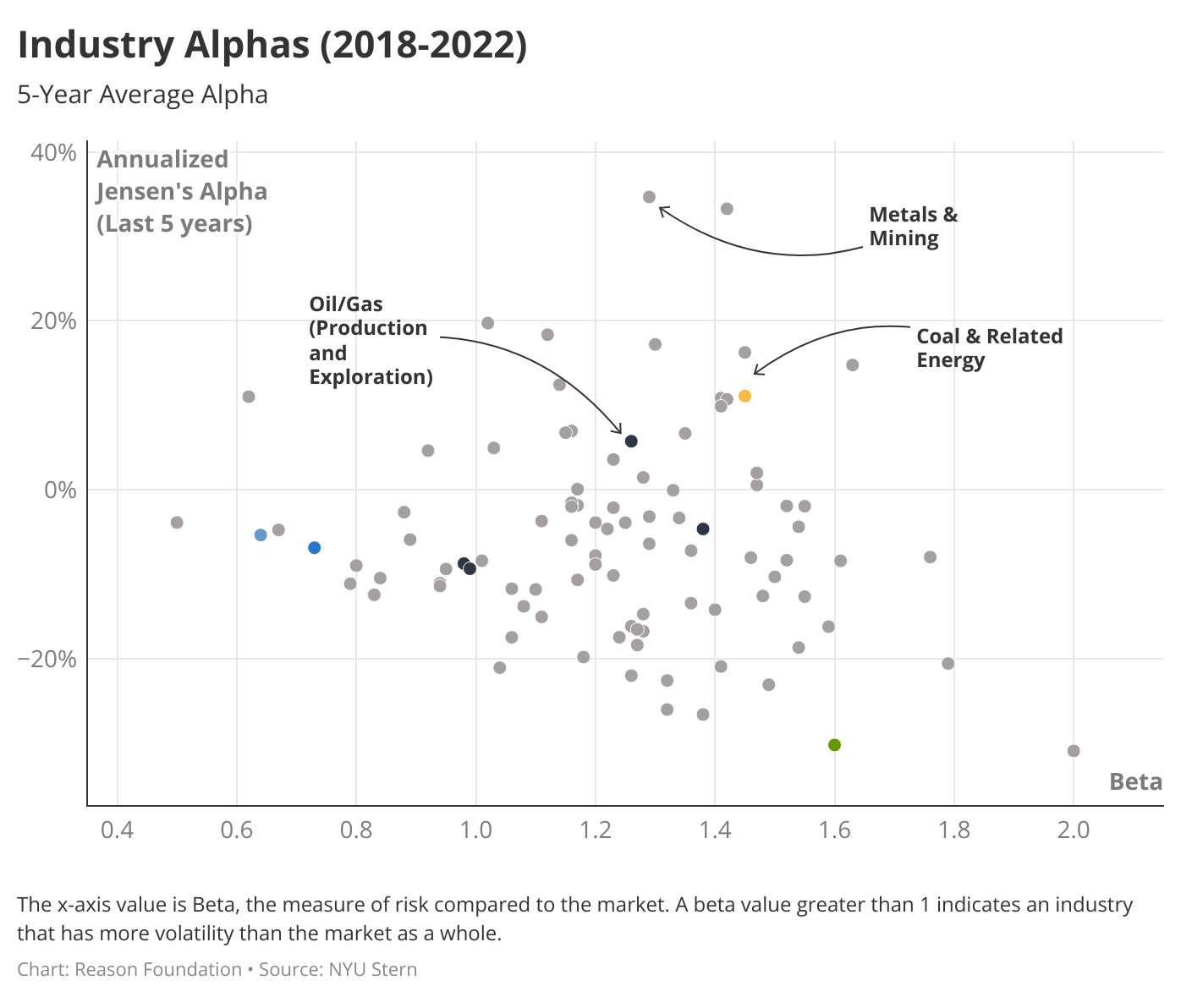

New York University Stern Professor of Finance Aswath Damodaran provides data on the five-year average of alpha generated in 96 different industries for the last 10 years. Damodaran also provides annual figures from 2002 to 2012. Alpha is a measure of risk and market-adjusted returns on a stock. A positive alpha indicates the investment has outperformed the market when adjusting for risk, whereas a negative alpha means the investment has underperformed.

However, the last 10 years, particularly for commodities, do not dictate the future performance. The global energy market, like other commodities, tends to go through drawn-out periods of highs and lows, commonly known as “supercycles,” so 10-year snapshots of these alphas likely don’t tell the whole story.

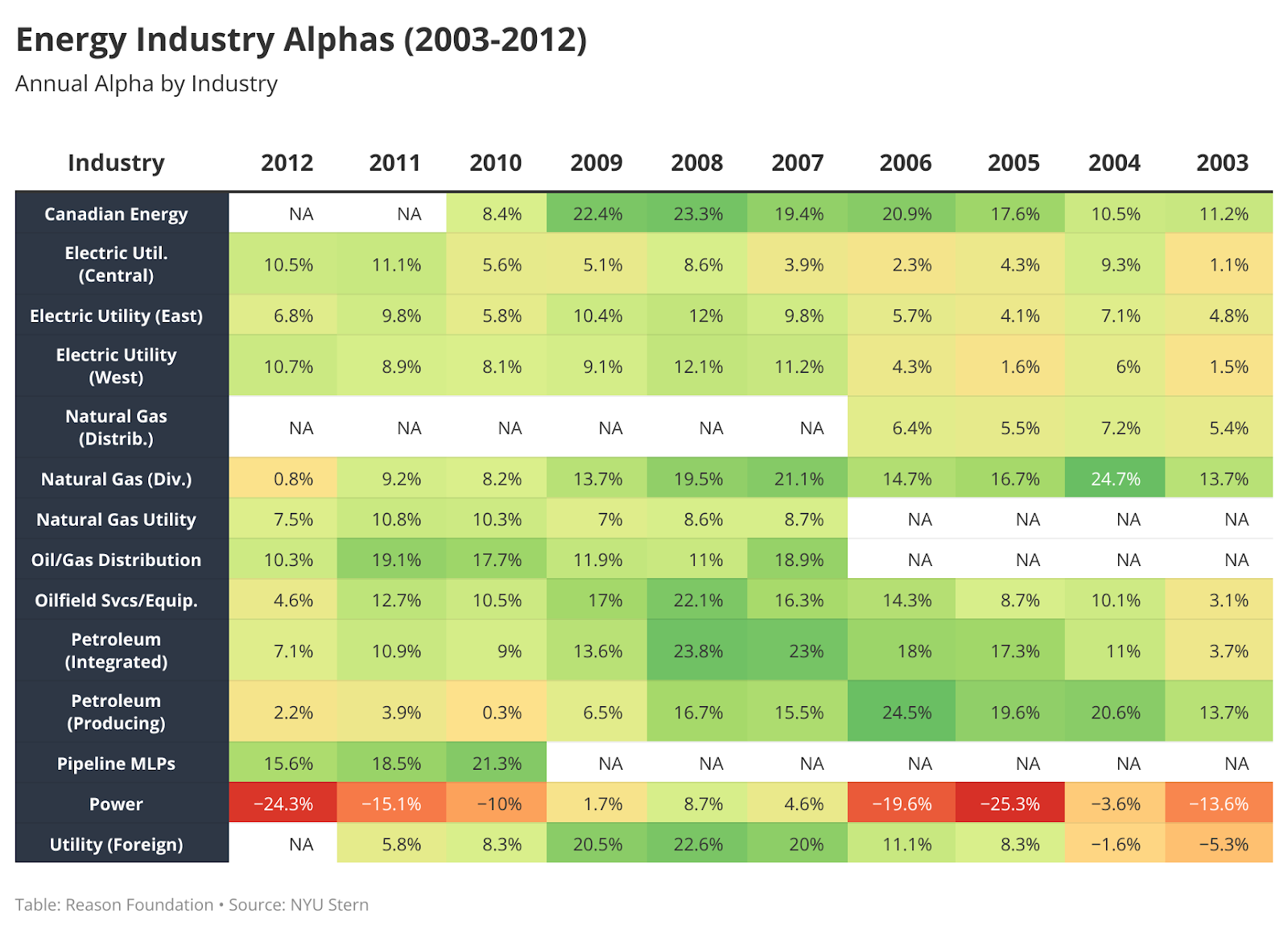

From 2003 to 2012, for example, energy sector industries nearly universally generated positive alphas year-over-year. Note that Damodaran’s data is formatted a bit differently in this older historical period: Alpha is reported as an annual figure, and the industry categories are somewhat different.

Only power and foreign utilities generated negative alpha values over this period, Damodaran finds. This broader history is essential to keep in mind when looking at post-hoc critiques of investment decisions or analyzing future investment decisions.

There are also suggestions the energy sector may be turning around. Jeff Currie, global head of commodities research at Goldman Sachs, believes we are in a commodities supercycle. In a Dec. 2022 report, Currie and colleagues wrote, “From a fundamental perspective, the setup for most commodities next year is more bullish than it has been at any point since we first highlighted the supercycle in October 2020.”

In a lecture published in Jan. 2023, Currie stated his belief that the market is in the second inning of a commodities supercycle, stating that they “probably have the strongest outlook of any asset class.”

Over the past five years, oil and gas production and exploration have generated a positive alpha of 5.7%. Coal and related energy had the 10th highest alpha of 96 industries, at 11.1%. Consistent with Currie’s thesis, metals and mining had the highest alpha average of the last five years.

As with any market forecast, Currie’s thesis may be wrong. But looking back on limited data from a short period, as the Stand.earth report does, shouldn’t be the basis for calling for hypothetical divestment from an entire sector of the economy.

Most importantly, public pension funds should not make ideologically or politically motivated divestment decisions and should focus on their fiduciary duty to make investments in the best financial interest of their members.