Public pensions are monitored by actuarial firms, which provide frequent projections on what actuarial liabilities, or promised benefits, will cost. Using publicly available actuarial valuation reports, Reason Foundation’s Pension Integrity Project has updated its 2017 report on these firms and finds a surge in the magnitude of unfunded liabilities of public pension systems overseen by the major actuarial firms.

Actuaries, in essence, possess little capacity to enhance or exacerbate the state of public pension plans’ unfunded liabilities aside from offering recommendations for adjustments in assumptions. Any escalation in unfunded liabilities is not a reflection of the actuary’s actions or expertise but rather a result of the decisions made by the sponsoring government that hires these advisors. Nevertheless, the data from these actuarial firms is valuable in tracking their overall market share and the evolving challenges they face.

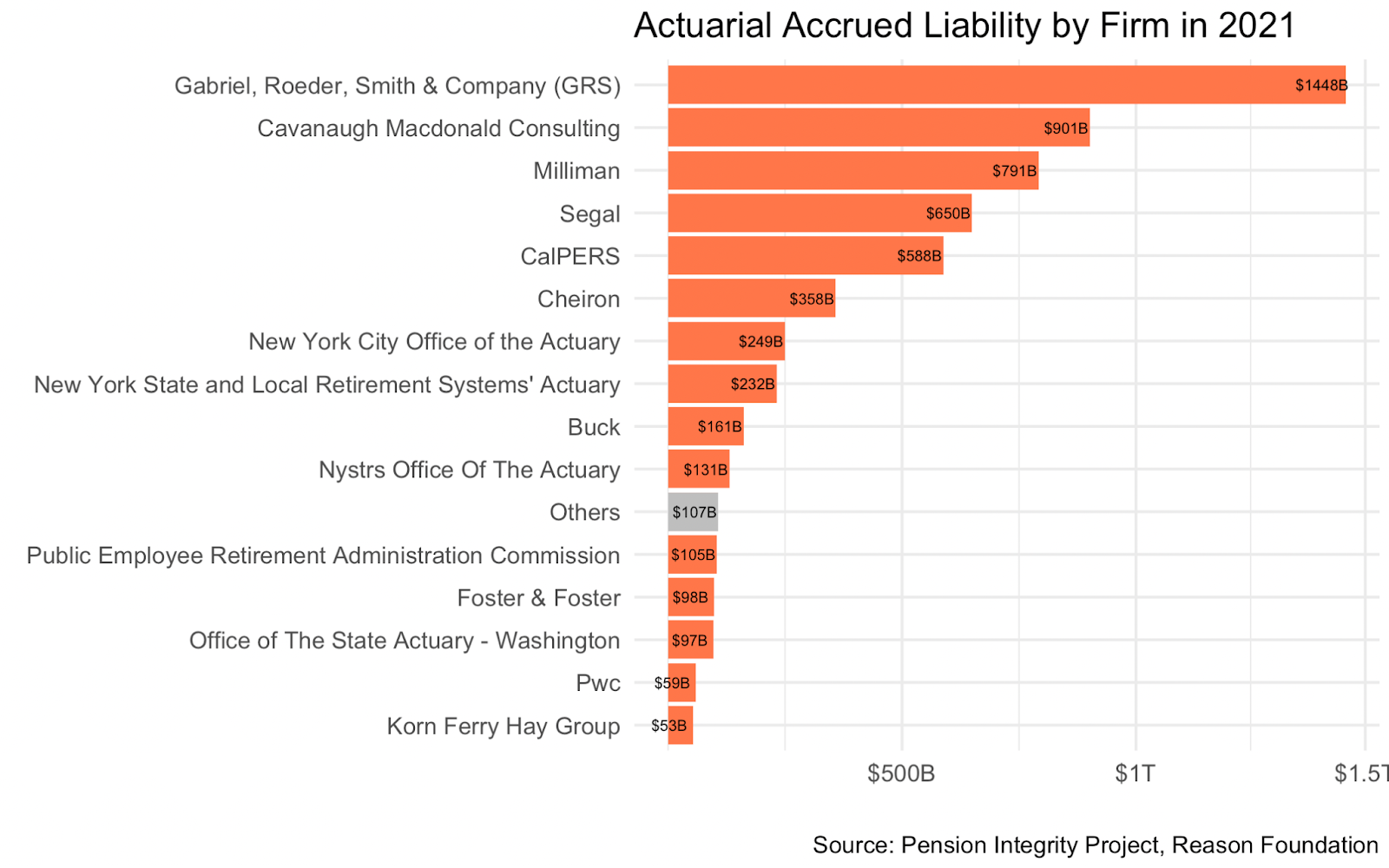

The 209 major public pension plans examined in Reason Foundation’s analysis—selected based on size and availability–make up 91% of total U.S. public pension assets. This group of plans contracted with 32 actuarial firms. Gabriel, Roeder, Smith & Company (GRS) remained in the top position, working with 55 plans, an increase of two public pension plans since 2016. In total, GRS oversees public pension plans with a combined actuarial accrued liability figure of nearly $1.5 trillion.

GRS, as the leader in the field, covers one-quarter of the total actuarial accrued liabilities amount among public pension plans. The three most prominent plans under GRS’s oversight were the Teacher Retirement System of Texas, with $228 billion in accrued liabilities, the Wisconsin Retirement System, with $125 billion, and the Ohio Public Employees Retirement System, with $118 billion in liabilities.

Just behind GRS, Cavanaugh Macdonald Consulting covers 34 public pension plans with slightly more than $901 billion in actuarial accrued liabilities.

The largest plans covered by Cavanaugh Macdonald Consulting were the Teachers Retirement System of Georgia, with $116 billion in liabilities, and the Virginia Retirement System, with $107 billion.

The next group of sizable actuaries includes Milliman, Segal, and the California Public Employees Retirement Fund (CalPERS), which cover actuarial liabilities amounting to $791 billion, $650 billion, and $588 billion, respectively.

CalPERS held the fifth position based on its in-house oversight of $588 billion in liabilities.

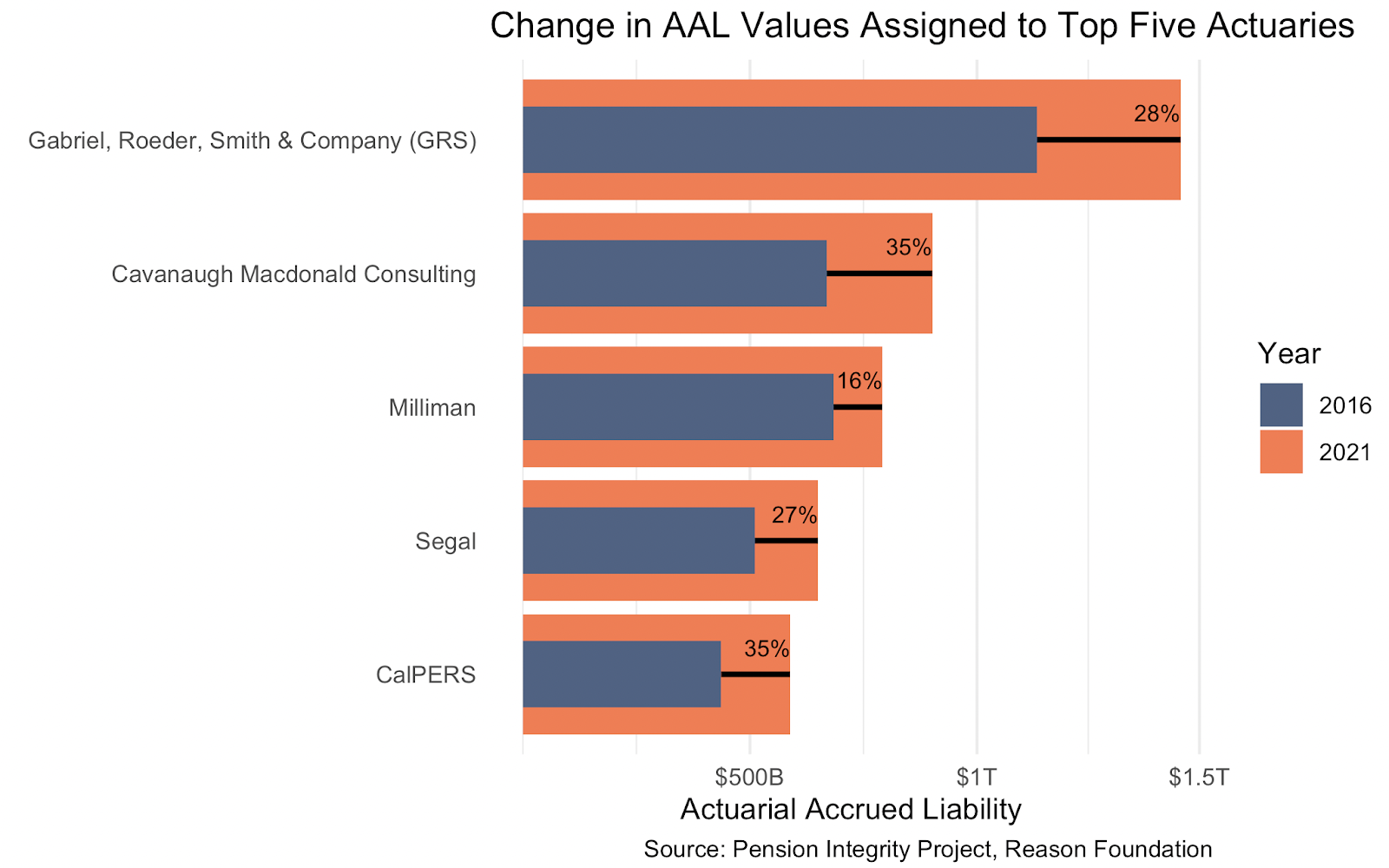

From 2016 to 2021, all of the top five actuarial firms observed an increase in the total actuarial accrued liabilities of the public pension plans they managed, which is unsurprising considering the growth of pension liabilities nationwide. As the firm overseeing the most liabilities, GRS predictably saw the most substantial leap in absolute actuarial accrued liabilities (AAL) value. In terms of percentage changes in AAL amount, both Cavanaugh Macdonald and CalPERS experienced a 35% increase, GRS a 28% increase, Segal 27%, and Milliman 16%.

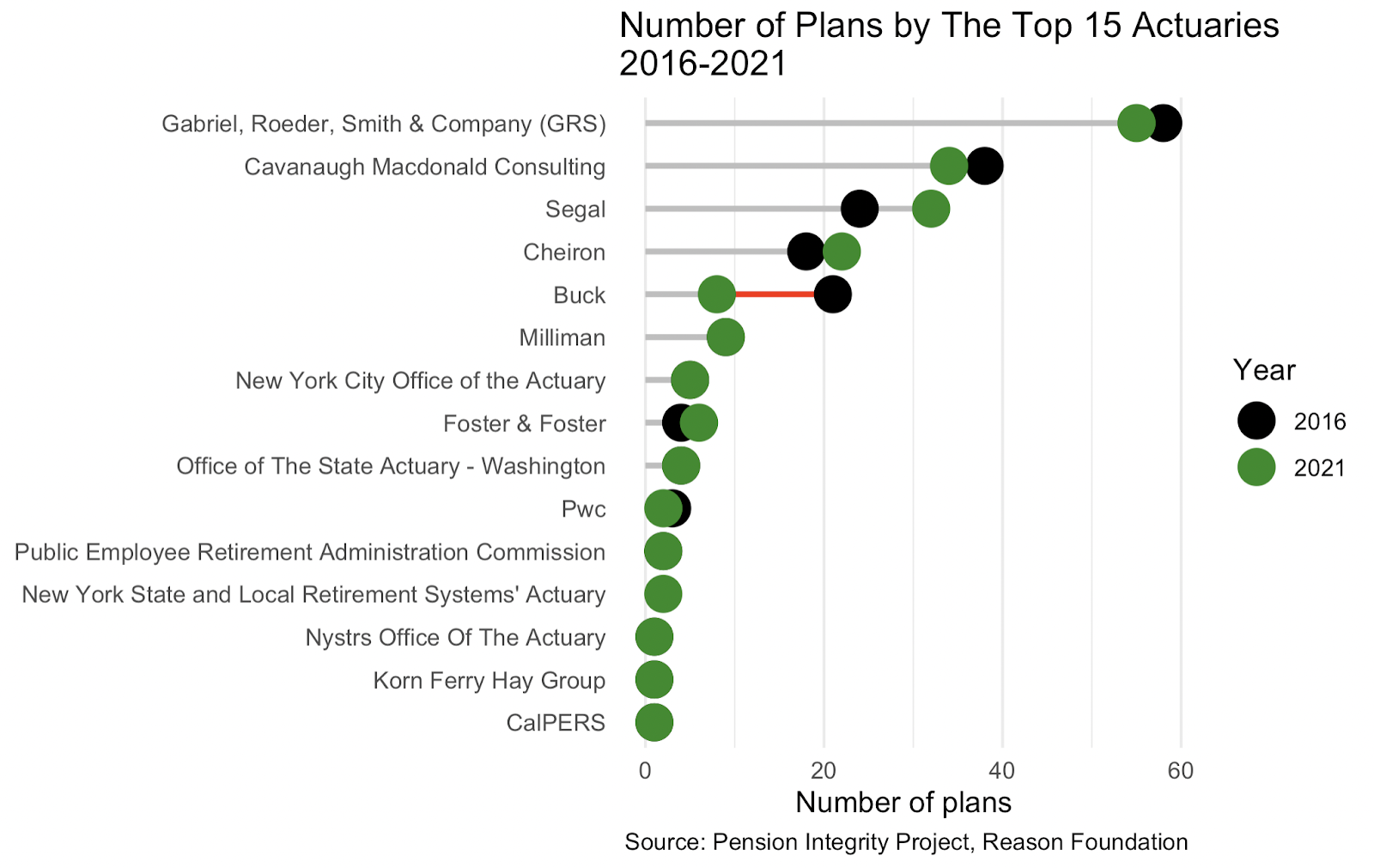

In terms of the number of plans overseen, most firms have expanded their portfolios of covered pension systems, with Segal taking the lead by adding eight new plans since 2016. Following behind were Cheiron with four additions and Foster & Foster with two new pension plans. Since Reason’s last study, Cavanaugh Macdonald Consulting dropped from 38 to 34 covered plans. GRS covered three fewer plans than they had in 2016.

Significantly, Buck’s contracted plans saw a marked decrease, plummeting from 21 plans in 2016 to eight by 2021. Out of these 13 plans that swapped actuarial vendors, five plans went to Cavanaugh Macdonald Consulting, another five to Segal, with the remaining three contracted with Hooker & Holcombe, Definiti, and Cheiron.

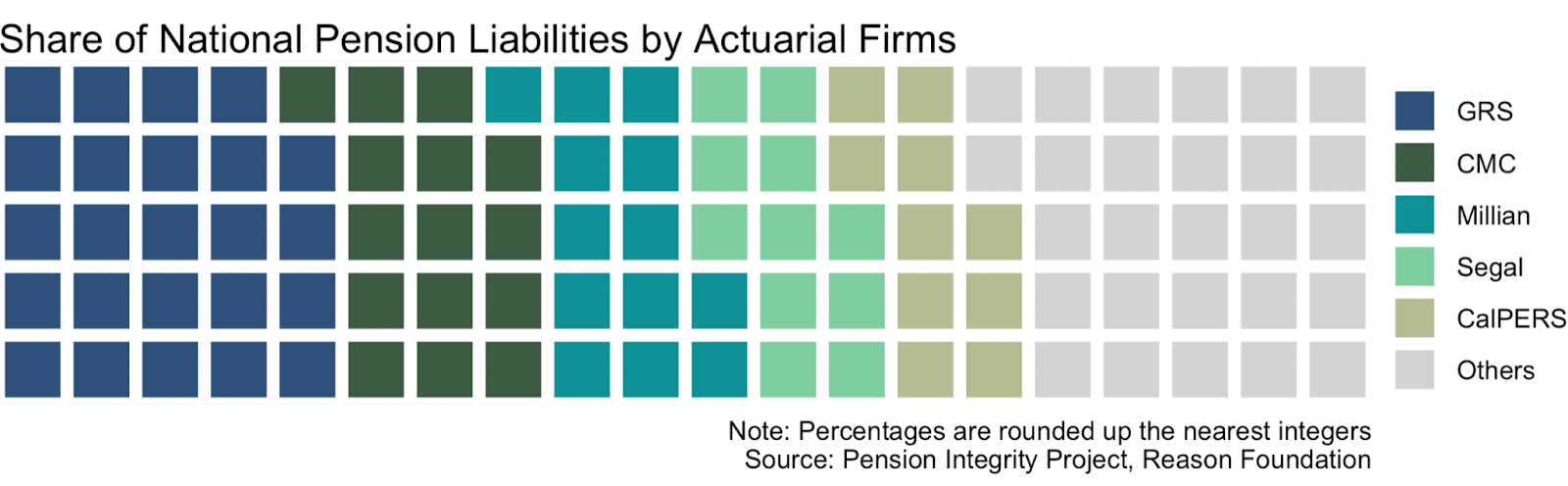

The top five actuarial firms jointly accounted for approximately 73% of all studied public pension liabilities in 2021. This distribution was as follows: GRS at 24%, Cavanaugh Macdonald Consulting at 15%, Milliman at 13%, Segal at 11%, and CalPERS at 10%. The other 27 firms shared the remaining 27% of accrued liabilities.

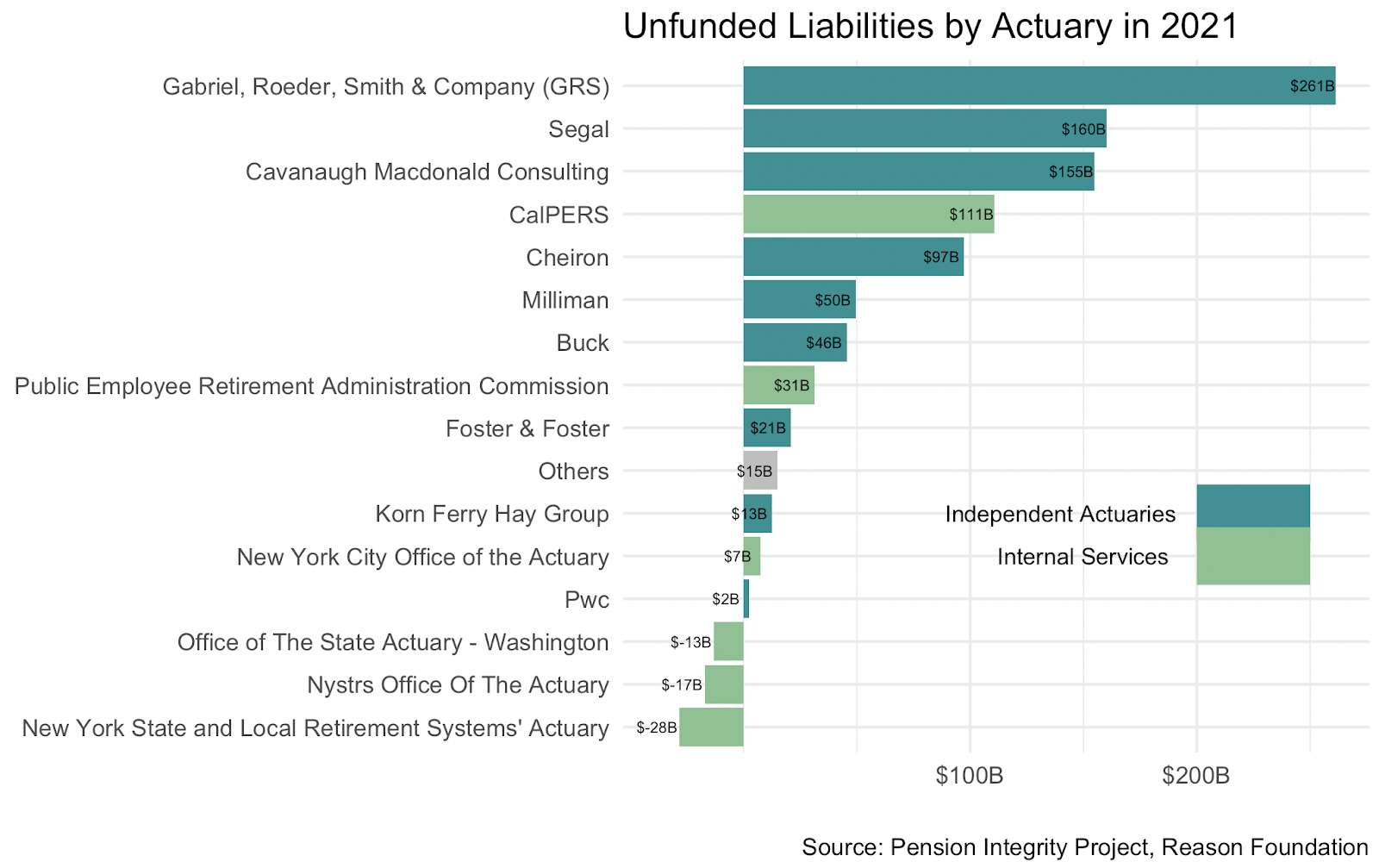

Actuarial firms are not responsible for the unfunded liabilities of the public pension plans who hire them. It is interesting, however, to see how these pension debts are distributed between the major advisors to gauge what unique challenges they may face. When speaking to unfunded liabilities, GRS again holds the top position, while Segal secures the second spot. Cavanaugh Macdonald takes third, and CalPERS claims the fourth spot. Notably, Milliman, which is among the top three in total liabilities, is tasked with overseeing only the sixth most unfunded liabilities.

In 2021, 44 overfunded pension plans were distributed among various firms. The net overfunded plans were primarily concentrated within three actuarial offices: the New York State and Local Retirement Systems’ Actuary, the New York State Teachers Office of the Actuary, and the State Actuary of Washington.

While unfunded public pension obligations continue to grow, these actuarial firms are responsible for conveying to the sponsoring governments—and their assigned pension boards—the need for more funding through higher annual contributions. Actuaries are also tasked with advising pension sponsors on the investment return rate assumptions that will be used to project obligation costs, significantly impacting the accounting of liabilities owed to employees and retirees by their government employers. Ultimately, actuaries are merely advisors, with the challenge of growing costs and risks falling to the sponsoring governments and their assigned boards.