Prepared for: Members of the Pennsylvania House State Government Committee

Prepared by:

Ryan Frost, Policy Analyst

Len Gilroy, Vice President

Date: August 19, 2021

Mr. Chair, members of the committee, I appreciate the opportunity to be a part of this hearing to discuss pension garnishment, forfeiture, and our overall outlook for Pennsylvania’s pension plans. My name is Ryan Frost, and I am a policy analyst with the Pension Integrity Project at Reason Foundation. Reason is a national 501(c)(3) public policy think tank, and the Pension Integrity Project offers pro-bono technical assistance to public officials and other stakeholders to help design and implement policy solutions aimed at improving public pension plan resiliency, promoting retirement security for public employees, and lowering long-term financial risks to taxpayers. Prior to joining Reason in 2019, I spent seven years as the Senior Research Manager for Washington State’s Law Enforcement Officers and Firefighters pension system, which is nationally recognized as being one of the top-3 funded pension systems in the country each year.

Pension Garnishment and Forfeiture in Pennsylvania

Pension garnishment and forfeiture are relatively unknown subjects because these policies are sporadically adopted across the country, and their usage is a relatively rare occurrence. In terms of definition:

- Pension garnishment is the policy of using a convicted elected official’s or public employee’s partially taxpayer-funded pension benefit to offset the cost of his or her incarceration, pay for restitution for bodily injury or loss of property, or to help pay settlements in a civil suit. Garnishment is typically the less severe punishment for an employee, as they are still eligible to receive any benefit above the amount owed due to their misconduct. In addition, any beneficiaries of that benefit would not be shut out from future payments.

- Pension forfeiture, on the other hand, is the policy of revoking any taxpayer-funded pension benefit the convicted member has earned in their civil service. Any potential pension payment the government employee would have earned is erased, and the pension system itself would absorb any contributions his or her employer (and thus taxpayers) made on their behalf. In some states, the public employee would be entitled to receive the amount they paid into the pension fund.

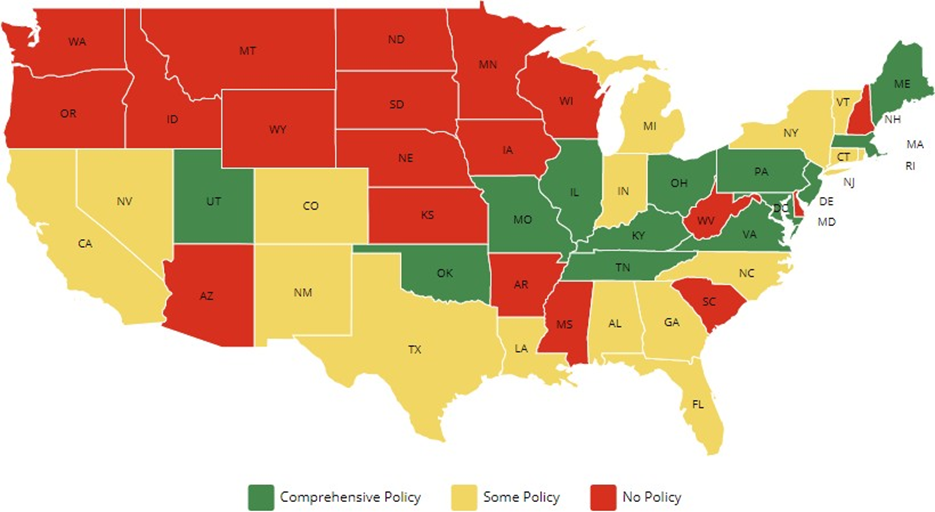

Pennsylvania is one of just 13 states that has what we refer to as a “comprehensive policy” when it comes to pension garnishment and forfeiture, adopted in 1978 as Act 140. A “comprehensive policy” is one that covers all public employees (including law enforcement officers), applies to any crime that relates to the employee’s position, and has guidelines for both garnishment and forfeiture. States with some policy, but not a “comprehensive” one, typically exclude law enforcement officers, or designate that the crimes committed by the public employee must only be of a financial nature to trigger garnishment or forfeiture.

Figure 1 – Garnishment and Forfeiture Policies by State

Pennsylvania has possibly the most clear-cut policy on this issue in the country. Act 140 does the following:

- No public employee, official, or their beneficiary will receive a retirement benefit of any kind if found guilty, or pleads no contest, to a crime related to their public employment.

- Refunds the employee’s contributions, without interest, if their pension is forfeited.

- The pension plan administrator may withhold employee contributions and the interest they’ve accrued to pay for any fines imposed on the pension fund due to the employee’s misconduct.

- The pension system shall not refund any contributions to the employee until the Auditor General and Attorney General have determined there has been no loss to the Commonwealth because of the misconduct.

A few of the state crimes that would trigger a forfeiture under Act 140 include:

- Theft

- Forgery

- tampering with records

- bribery

- perjury

- tampering with public records or information

- criminal attempt, solicitation, and conspiracy murder

- manslaughter

- aggravated assault

- corruption of minors

- distribution of computer virus; bomb threats

- and sexual offenses listed in Chapter 31, Subchapter B of the Pennsylvania Crimes Code.

Garnishing or revoking an individual employee’s pension will have a near-zero impact on the public pension fund’s solvency due to the sheer size of most public sector defined-benefit plans in the United States. Garnishment and forfeiture are better understood as issues of legality and morality, and the arguments surrounding these policies aim to address two questions.

First, are pensions part of compensation, or are they gifts from the state? Keith Brainard of the National Association of State Retirement Administrators (NASRA) posed this question back in 2012. If pensions are earned parts of compensation, they would typically follow the same policies and laws that govern other parts of compensation. Brainard, at the time, stated that “normally, an employer wouldn’t and probably couldn’t go claim back wages that were paid” and “pension benefits are part of the compensation just as much as wages.”

Second, does somebody who has committed a felony while performing a public sector job deserve to be supported in his or her old age at taxpayers’ expense? In Illinois, the state with the oldest forfeiture laws dating back to 1955, the Supreme Court answered this question by stating that the policy was designed for “ensuring the public’s right to conscientious service from those in governmental positions.”

Anecdotal evidence of pension forfeiture laws dissuading law enforcement officers from committing misconduct was found in a 2017 study in the Journal of Law, Economics, and Policy. The study concluded that “initial and admittedly casual evidence suggests that states with stronger pension forfeiture laws experience lower rates of police misconduct.”

Regardless of the justification for using pension garnishment and forfeiture policies, it is important that lawmakers understand the impacts and function of these pension policies. While these policies will neither help nor hurt the overall solvency of large public pension systems, they can add transparency, accountability, and be used as a deterrent from any misconduct by public employees.

Outlook on Pennsylvania’s Pension Systems

This is a momentous time in the public pension space, and your committee should be commended for proactively engaging the current policy discussion regarding the long-term solvency of your pension systems. The last decade has seen a significant amount of pension reform activity across the nation, as states and municipal governments in many regions reckon with the rising costs associated with servicing over $1 trillion of unfunded public pension liabilities nationally. Prudent elected leaders in several states—including the Commonwealth via your major reforms in 2017, have made large-scale reforms in the past five years, but there is much work that remains.

Most recently, Texas demonstrated a gigantic commitment to pension stewardship by annually allocating hundreds of millions of dollars in extra contributions to pay down debt faster in their pension plans, as well as moving all new hires into a risk-managed design that will limit future unfunded liabilities. CalPERS, the largest pension plan in the US, has also been a reform leader with a policy that is lowering their assumed rate of return, down to 6.8%, due to this past year’s extraordinary investment returns. Because of the large investment gains seen across public pension plans in this unique year for market returns, it is the perfect one-time opportunity to be looking at prudent changes that will leverage those gains to improve the solvency of your pension systems.

First, let’s look back at recent changes to your plans. After years of underperforming investment returns, a history of failing to pay the actuarially determined contribution, and prior reforms in 2010 having a limited effect on the growth in UAL amortization payments, this body passed meaningful pension reform in 2017 to ensure that future generations would not be faced with the burden of rising pension debt. That reform went a step further than other reforms we’ve seen by creating a commission to look at the fees paid to asset managers and used the savings from those findings to pay down unfunded liabilities.

Since those reforms, the plans have also lowered their assumed rates of return, down to 7.0% for SERS and 7.25% for PSERS. The assumed rate of return is the most important assumption in terms of its effect on a plan’s solvency, as investment returns have accounted for around 60% of all public pension assets over the past 30 years. Putting the plans ARR at a lower, more realistic number would drastically decrease the chance of unfunded liabilities accruing in the future but does have the near-term impact of temporarily making pension plans more expensive in the interest of lowering long term employer costs.

Luckily for Pennsylvania, you have two brand new pension tiers still in the asset accumulation phase, making the process of matching the plan’s ARRs to a near-term investment outlook much easier than a plan that has been open for longer.

Possible Additional Reform Recommendations

Paying the full actuarially determined contribution (ADEC) is also crucial for the extended success of your pension systems. From 2001-2016, the state paid less than the amount calculated by actuaries, leading to debt growing at an alarming rate. During the first half of the bull market run-up, from 2009-2016, Pennsylvania had the worst-funded status trajectory in the country, dropping from 61% in 2009 to 52% in 2016. Thankfully, employers have paid the full ADEC each of the last five years. Maintaining this recent funding discipline by requiring employers make the full ADEC payment each and every year as a requirement in statute would be a prudent step forward for your pension systems and is a common policy adopted in other states.

Additionally, the long amortization schedules the two plans use to pay down pension debt has greatly contributed to their inability to pull themselves out of underfunding. Current policy allows any actuarially experienced debt to be amortized over a 24-year, level-percent period. This is too lengthy and exposes taxpayers to the risk of worsening pension debt that compounds on very high interest rates. Meanwhile, public pension actuarial professionals — including the Society of Actuaries—have begun to recommend amortization periods of 20 years or less.

The level-percent method also contributes to future underfunding because it’s tied to a salary growth assumption, where plans pay less in the early years of the schedule due to assumed increases in plan payroll, but payments balloon to sometimes unaffordable levels at the end of the schedule. Moving to level-dollar amortization is a more viable strategy, as the plan would expect to pay the same dollar amount each year of the schedule, creating stable contribution rates and ensuring the ability to completely pay off the debt.

While an immediate shift of all legacy unfunded liabilities to level-dollar amortization would require additional contributions in the near term that may be a difficult fiscal challenge, a way to begin a slow shift toward more prudent amortization would be to pay off any new unfunded pension liabilities within 10 to 15 years of the date they accrue, on a level-dollar basis. This would ensure that any new pension debt will be quickly paid in full and save taxpayers hundreds of millions in avoided long-term interest. Because this policy would only affect new debt that hasn’t materialized yet, there would be no financial cost to adopting it.

Lastly, another prudent change to consider in the near term would be to increase the employer contribution to the DC-only retirement plans. Currently, members of those plans contribute 7.5% of their salary, while the state only contributes 2% in PSERS and 3.5% in SERS. This 9.5% does not meet the industry-recommended 10-15% of salary threshold that would be needed to fund a proper benefit for retirement for those employers participating in Social Security. Offering a higher employer match to the employee contribution in the DC— even up to matching the 7.5% employee contribution—would ensure greater financial stability for Pennsylvania’s future retirees.

The Pension “North Star” for Pennsylvania: Redesigning for Pension Resiliency

While experiencing market volatility, most US public pension systems find themselves watching whatever gains they achieved from the most recent run-up disappear. Taking aside what all observers expect to be a stellar year for one-time investment returns, industry capital market forecasts continue to suggest persistently volatile near-term investment returns that stand to only add to over $1 trillion in current pension funding shortfalls. Most near-term investment outlooks we’ve seen from pension boards across the country predict anywhere from a 6.0%- 6.3% return over the next 10 years.

Pennsylvania’s pensions are no different. The findings of a forthcoming Monte Carlo simulation analysis developed by the Pension Integrity Project based on pension system asset allocations and reported expected returns by asset class suggests that neither of your largest pension systems are likely to achieve even a 6.0% average return over the next 10 to 15 years, which suggests a high probability that unfunded liabilities get worse, not better, in the near term, making the long-term solvency challenge ever larger.

The current assumed rates of return used by the systems, which are 7.0% or higher, appear to have little more underlying supporting rationale than “reversion to the mean”—or put more simply, “a guess that assumes performance from the past continues,” despite past performance being universally recognized as no reliable indicator of future results. Given that the assumed rates of return are generally set at the 50th percentile to begin with—meaning the best chance you have if you hit every single actuarial and demographic assumption you set is a 50/50 chance of achieving long-term solvency—policymakers should be under no illusion that they can invest their way to solvency alone.

Systems taking another significant hit to pension assets before they were able to fully recover from the last recession leaves states and local governments with the challenge of finding additional resources to divert to their state-sponsored pension systems at a time when resources are extremely scarce.

If the last two global crises in 2008 and 2020 can offer anything from a policy perspective, it is that financial resiliency needs to be a primary aim for U.S. public pension funds in the 21st-century economy. Over $1 trillion in unfunded liabilities did not accumulate overnight, nor will they be paid off overnight. In fact, given the prospect for below-target returns over the next 10 to 20 years, it is unlikely that pension systems will be able to “invest their way” out of the current situation and more likely that unfunded liabilities worsen absent additional policy action.

The Pension Integrity Project believes that the “invest your way out” mantra will continue to poorly serve taxpayers, employees, employers, and retirees. This perspective needs to be replaced with a new operating principle designed to substantively impact both legacy and new unfunded liabilities in a realistic manner.

For example, if we are truly concerned about simultaneously protecting both pensioner and taxpayer best interests, then it would be prudent to reconsider maintaining 7+% assumed investment return assumptions when those are ultimately based on faith in a “reversion to the mean” over the next 30 years, an outlook we believe to be unjustified by 10- to 20-year capital market forecasts, as discussed above. From our perspective, it would be more prudent to hope for the 30-year returns to revert to a mean at or above 7%, while actually planning for a situation in which they do not.

In short, modern policy prudence in the arena of public pensions suggests that policymakers should hope for the best, but plan for the worst. After all, decades of doing the reverse have led to the current underfunding situation.

In an article last year, we suggested a need to rebuild our public sector retirement systems in the U.S. in a way that embraces the concept of pension resiliency, similar to how public infrastructure systems are being redesigned to accommodate and reduce the severity of unexpected weather disasters, for example. In general, we believe that resilient public employee retirement systems are those that:

- Rely on a governance structure designed to minimize the role of politics;

- Can take many forms but are designed to manage risk through autocorrecting features and policy guardrails;

- Use realistic assumptions and are disciplined in maintaining full funding of their pension plans;

- Create a path to lifetime income for employees while avoiding intergenerational equity disparities, public service crowd-out, and runaway taxpayer costs;

- Assess—and plan for—downside risk.

The Commonwealth has begun this process but has more work to do. Unfortunately, addressing these important issues will likely make the fiscal issue look far worse before any solution will take hold for the better. If, for example, U.S. public pension plans adopt more realistic accounting of their obligations by lowering their assumed returns—as the Pension Integrity Project would generally recommend for many plans— unaccounted for liabilities will increase when valuations are published, and contributions will necessarily rise as a result.

However, the sooner plans embrace modern day market realities, the better these important issues can be addressed over the long-term. With that mindset, they can begin to fortify weak areas of the system to prevent the current situation from ever happening again. The perfect time to embrace these realities is now, with these large one-year market returns opening the possibility of “buying down” the plan’s assumed rate of return assumptions, similar to what CalPERS just did last month.

Building resilient retirement systems that create a pathway to lifetime income for all employees while avoiding intergenerational disparities and the need to constantly mitigate financial challenges threatening the basic obligations of state and local governments should be the North Star that guides this committee. This legislative body should look to additional phases of reform in the arenas of improved funding policy, amortization of unfunded liabilities, and governance, given the good work done so far to start de-risking SERS and PSERS for the future via the introduction of risk-managed plan designs for new hires the last several years.

Thank you for your time, Mr. Chairman, and members. I would be happy to take any questions from the committee.