It’s time for North Dakota to get serious about runaway pension debt. For decades, North Dakota’s elected officials have structurally underfunded the state’s largest pension plan for public workers. That almost changed in 2021 when both legislative chambers passed pension reform legislation, but disagreements between House and Senate conferees over the details of how to address pension underfunding caused the reform bill to die in the conference committee process. This has left the issue of growing pension debt unresolved.

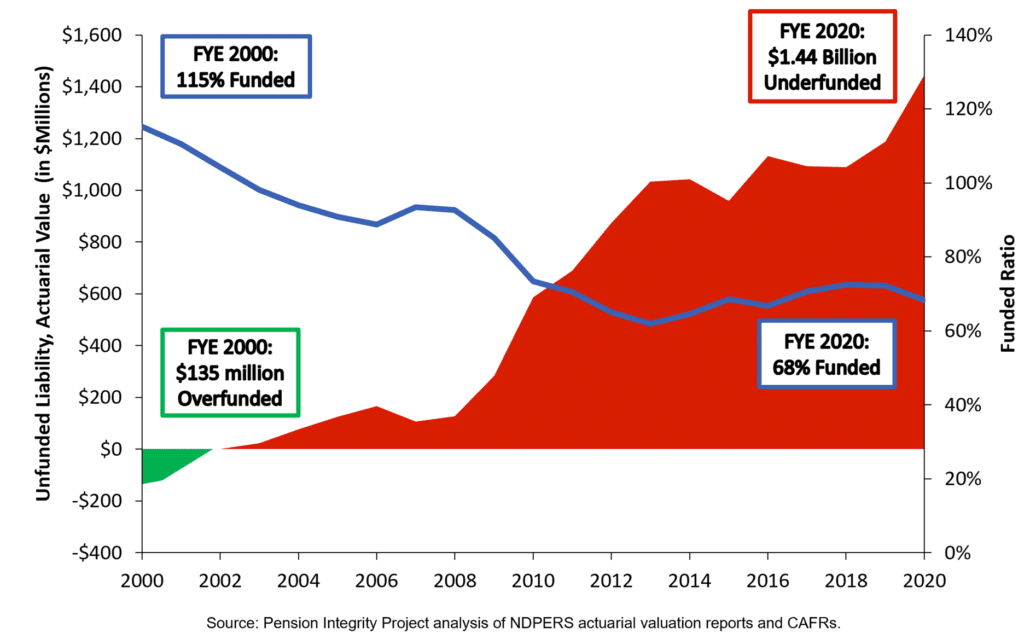

In 2000, the North Dakota Public Employees Retirement System (NDPERS) boasted a 115 percent funded ratio and a $135 million surplus of funds to pay for public employee retirement benefits. Since then, NDPERS has accumulated $1.4 billion in unfunded liabilities. This debt is driving up future costs for taxpayers via debt service and the system has plummeted to only 68 percent funded today (see Figure 1).

Figure 1. A History of NDPERS Solvency (2000-2020)

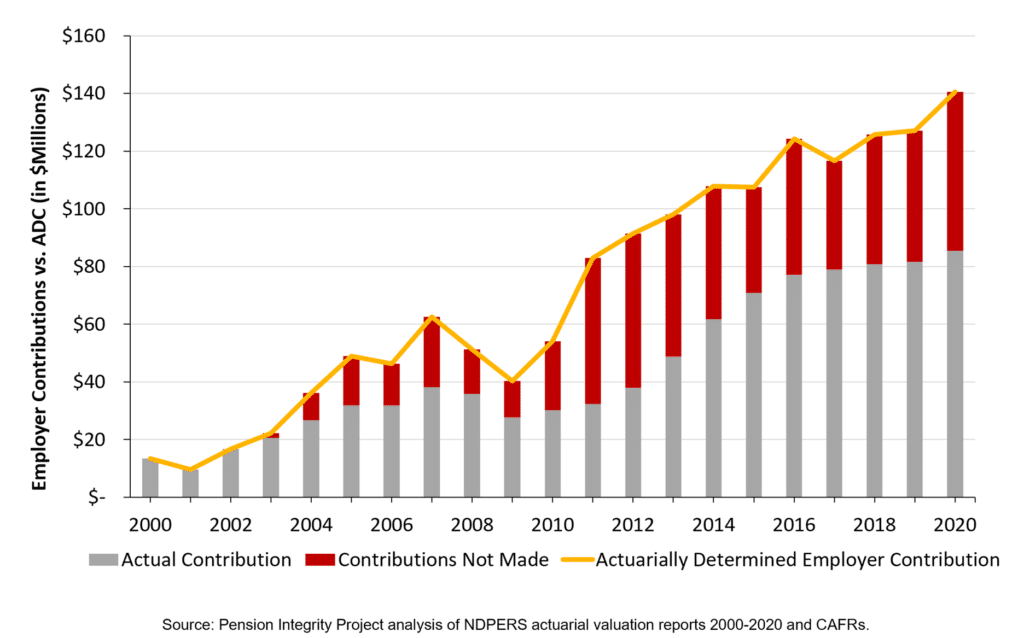

NDPERS’s structural underfunding is primarily driven by the legislature’s historical use of fixed, statutorily set contribution rates that have consistently been set below the amount actuaries calculate is needed to fully fund all earned retirement benefits. This means that for 15 years the state has consistently failed to pay the actuarially required amount to keep the plan solvent (see Figure 2). For the 2020 fiscal year, the deficit between actuarially required contribution rates and the statutory rates was 5.87 percent of payroll or about $67.6 million in missed contributions.

Figure 2. Actuarially Determined Employer Contribution History, 2000-2020 Actual v. Required Contributions

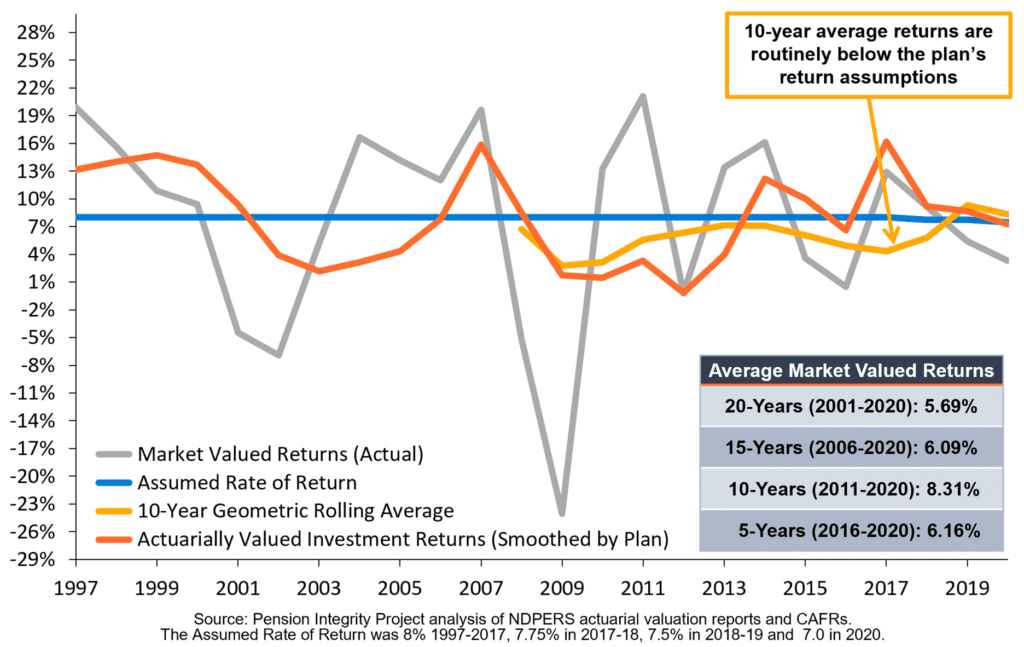

In addition to inadequate contributions, NDPERS investment returns have failed to meet expectations and this shortfall has contributed to the growth of unfunded liabilities. The investment return assumption for the plan was an unreasonably high 8 percent until 2016 when it was reduced to 7 percent. For every year investment returns fail to meet the return assumption, unfunded liabilities grow. The system has fallen short of even a 7 percent return on average and earned an average investment return of 6.1 percent over the last 15 years, and despite a decade-long bull run in the capital markets, NDPERS never fully recovered from the Great Recession (see Figure 3).

Figure 3. NDPERS Investment Returns History, 1997-2020

During North Dakota’s 2021 legislative session, legislators were poised to tackle the state’s pension underfunding and considered several pieces of reform legislation, including a bill to transform the retirement plan design. This bill passed both chambers but failed to get resolved in the conference committee.

That failure to reach a bicameral consensus was unfortunate, but with some simple and straightforward tweaks to the reform legislation, legislators can build on the momentum created in 2021 to enter the 2023 legislative session with a coherent and sustainable plan to improve NDPERS’s solvency and promote stakeholder equity.

Lawmakers’ previous attempts to update the benefit structure for new hires and improve how the state funds the pension system manifested in several different pension bills that attempted to address North Dakota’s pension challenges in different ways. Most focused on the current plan’s funding policy while one—Senate Bill 2046—made provisions for additional funding for the legacy NDPERS defined benefit plan while directing all new hires into the state’s long-established primary defined contribution retirement plan choice.

The Pension Integrity Project at the Reason Foundation provided technical assistance to numerous state lawmakers in North Dakota both in advance of and during the 2021 session, utilizing our in-house actuarial modeling of NDPERS to assess the financial and fiscal impacts of potential reform solutions.

In the preliminary stages of the legislative process, one of the bills, House Bill 1209, was a simple plan to address the chronic underfunding of NDPERS by switching from statutorily established contribution rates to the actuarially recommended contribution rate. As originally introduced, HB 1209 embodied best practices for properly funding NDPERS by stopping structural underpayments that significantly hindered the system’s ability to grow assets to meet the promises made to public workers for decades. For years, contributions based on statutory rates were woefully insufficient according to both our independent analysis and NDPERS’ own actuaries. The Pension Integrity Project provided testimony regarding these issues during the initial House committee hearing on HB 1209, but the bill was subsequently transformed into a study bill.

House Bills 1342 and 1380 would also have increased contributions in different ways. HB 1342 would have increased employer and employee contributions by 2 percent of payroll each (for an aggregate 4 percent increase), while HB 1380 would have transferred 5 percent of the earnings from the state’s sovereign wealth fund to the NDPERS pension fund as one of several dedicated appropriations. These bills would have both improved the funding status of NDPERS but neither were comprehensive reforms that would have prevented future unfunded liabilities from accruing.

Senate Bill 2046 ultimately became the primary legislative vehicle for pension reform proposals. Originally a simple proposal to increase the NDPERS statutory employee and employer rates by 1 percent of payroll, for a combined total of 2 percent, SB 2046 evolved into a more comprehensive reform effort that included:

- Closing the current defined benefit plan to new workers (except those in public safety positions and judges)

- Enrolling all new hires in the currently optional 401(a) Defined Contribution (DC) plan

- $50 million in biennial legacy fund contributions

- A one-time $100 million cash infusion

- The separation of plan assets/debt by municipal and state employment

The Pension Integrity Project’s preliminary evaluation of SB 2046 found the measure to be lacking in many crucial objectives of good pension reform.

The reform did not properly amortize debt or sufficiently address the state’s problems with annual contributions below the actuarially determined amount. Actuarial modeling showed that over a 30-year period SB 2046 created a serious risk of bankrupting the NDPERS defined benefit system, findings that were further corroborated by analysis from the system.

Although SB 2046 failed in the conference committee during the last week of the 2021 session, there were several positive developments resulting from the process. NDPERS stakeholders were able to successfully explore and debate the state’s pension issues and took the conversation from the periphery to a burgeoning legislative priority. Policymakers, stakeholders, and taxpayers are now more aware of the issues at hand.

However, increasing awareness is not enough. To save taxpayer dollars and return NDPERS to a path towards full solvency, future efforts to reform NDPERS will need to include policies that address all the challenges that face the beleaguered system, especially those associated with long-term funding. Future changes need to address employer, taxpayer, and employee needs.

Examining Potential NDPERS Reform Options

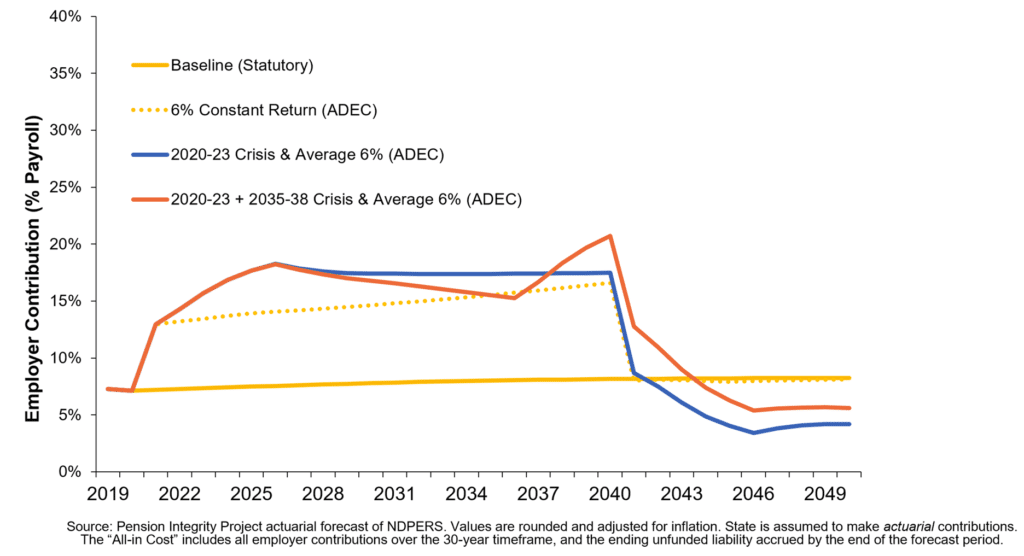

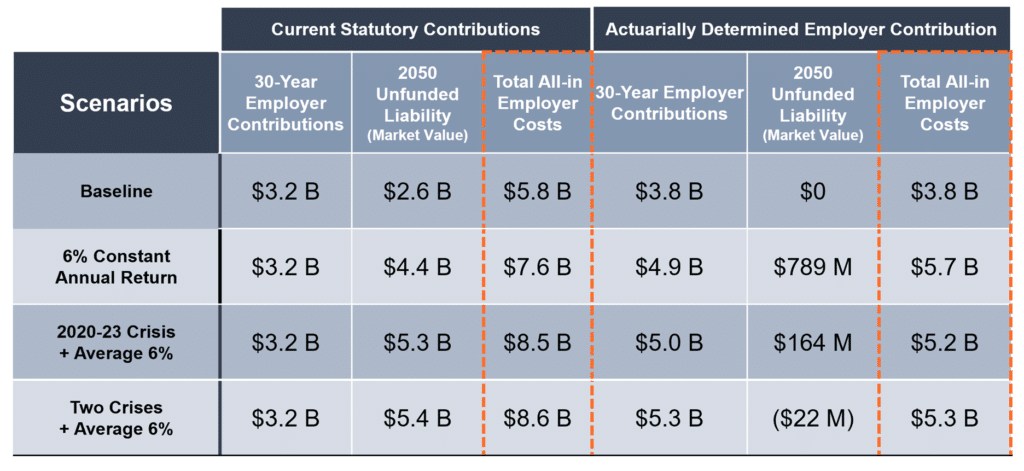

At the heart of good pension reform is a commitment to paying an actuarially based contribution rate. Setting contributions to align with actuarial recommendations would require higher annual contributions in the near term but doing so would dig NDPERS out of a dangerous funding situation (see Figure 4). As seen in Table 1, paying the actuarially determined contribution (ADEC) each year could reduce long-term costs by over $3 billion by reducing expensive interest on pension debt.

Figure 4. How a Crisis Increases NDPERS Costs

Table 1. Scenario Comparison of Employer Costs—ADEC Reform

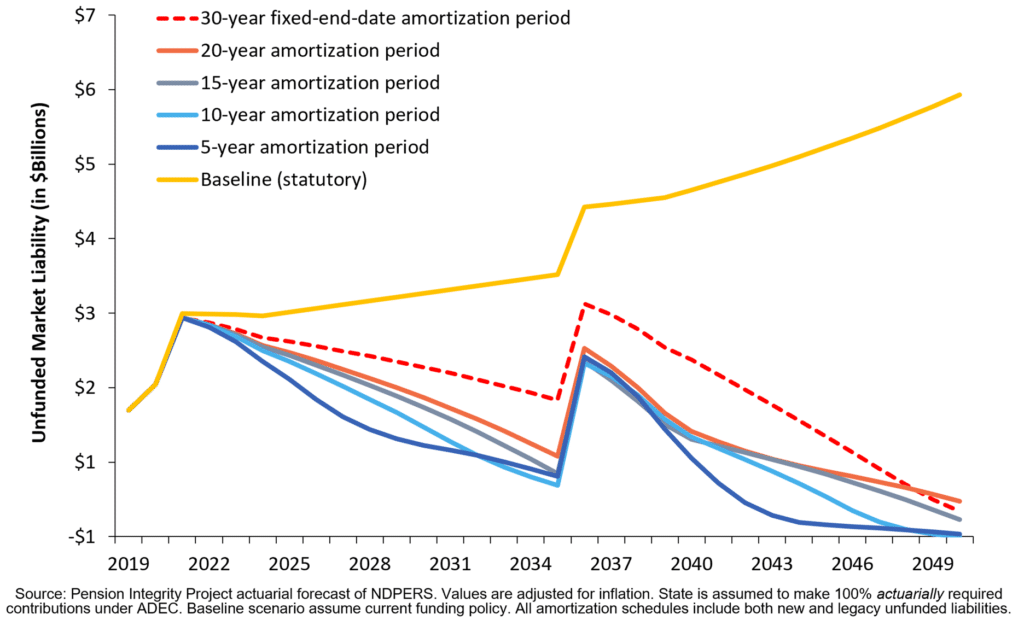

Implementing ADEC would ensure that the state contributes at a level that fully funds all accrued retirement benefits regardless of market volatility (see Figure 5). While this commitment would amortize current NDPERS debt on a fixed schedule—ideally less than 30 years—to avoid runaway interest driving up unfunded liabilities and perpetuating intergenerational inequities should also be included in any future reforms.

Figure 5 shows that when paired with an actuarially determined employer contribution (ADEC) funding policy, shorter amortization periods reduce plan debt and lower overall cost, especially during difficult economic conditions (see Table 2). Amortizing any future years’ worth of NDPERS debt on schedules of 20 years or less significantly reduces the risk of runaway debts in the future.

Figure 5. How a Two Recession Crisis Impacts Debt Amortization Schedules

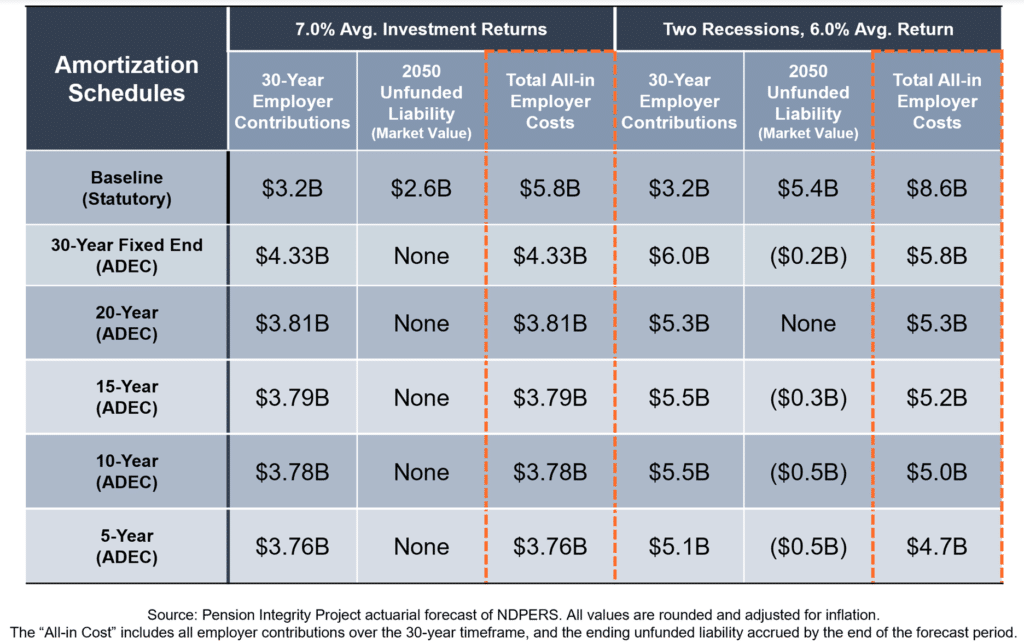

Table 2. Scenario Comparison of Employer Cost—ADEC Reform + Short Amortization

The use of ADEC funding policy and short amortization schedules are both best practices that should be adopted whether the existing defined benefit plan remains open or not, as these policies would essentially address the current $1.4 billion hole North Dakota currently finds itself in. That said, additional proactive reforms would still be necessary to ensure the system avoids future runaway costs, such as lowering the NDPERS assumed rate of return on investments to limit the system’s exposure to market volatility.

Managing Future Risk through Expanded Retirement Choice

State policymakers should also explore policy reforms to offer new retirement options that better match the needs of today’s mobile modern workforce, which is poorly served by retirement designs that rely on long career tenures.

The simplest way for North Dakota to slow the growth of unexpected costs in the future would be to improve the retirement plan choices available to public workers in North Dakota today, which currently consist of the traditional, default defined benefit (DB) pension plan and the NDPERS defined contribution (DC) retirement plan option available only to non-classified workers by written election today.

According to the North Dakota Office of Management and Budget, there were 7,860 benefited state employees in March of 2021. Only 926, or 12 percent of benefited employees were eligible to join the NDPERS defined contribution plan, and even these 12 percent currently default into the NDPERS defined benefit pension, rendering the current “choice” moot, in effect. The results of this restriction and enrollment method heavily favor the defined benefit plan and basically creates an illusion of choice where little exists.

Unlocking the availability of the state’s existing DC plan to all new workers and flipping default enrollment to the DC plan would substantially limit the ability of NDPERS to incur future debt. This move would provide more choice to new workers who are increasingly mobile and less likely to stay under public employment long enough to enjoy the long-term benefits of the defined benefit plan.

Improving the NDPERS Defined Contribution Plan

Currently, the NDPERS DC plan boasts very healthy contributions rates of an aggregate 14.12 percent of salary, which is aligned with industry best practices. However, there is still room for improvement to make the DC plan a more attractive choice for employees.

North Dakota’s DC plan objectives are currently not clearly defined. Although the plan seeks to provide retirement income, it does not set an income replacement goal or cost targets. This makes it hard to tell if the plan is achieving retirement security for members. Also, the DC plan’s standard distribution method is a lump sum, and the plan doesn’t offer a lifetime annuity option. Without a default annuity option, there’s a heightened risk that DC plan members may prematurely exhaust their retirement fund.

In future efforts, the legislature could also consider a choice-focused retirement reform that could keep a defined benefit option for new workers instead of permanently ending it, as SB 2046 attempted. This could be achieved by creating a new risk-managed pension benefit tier for new hires with cost and risk-sharing features incorporated into the fundamental design that naturally winds up as the legacy NDPERS pension tier in effect today winds down through attrition over time.

This new tier should include a 50/50 cost-sharing provision to help reduce the risk for public employers and taxpayers. Cost-sharing means that employees would match every dollar an employer contributes to the fund. A new reduced-risk tier would also need a firm commitment to paying the actuarially required contribution rate to avoid debt, more conservative actuarial assumptions, and a short amortization schedule to ensure any new debt is quickly paid off.

It’s important to responsibly pay off the current legacy NDPERS pension liabilities no matter what happens with new-hire retirement benefits. Amortizing unfunded liabilities associated with any legacy pension plan over total state payroll (legacy pension participants + new and existing defined contribution participants)—as Oklahoma, Arizona, Florida, Utah, and other states have done in similar situations—ensures that legacy unfunded liabilities are paid down in a fiscally prudent manner.

Conclusion

North Dakota’s retirement system has a clear need for reform. We’ve outlined a few options that would ensure fiscal solvency, reduce long-term risk for taxpayers and maintain attractive retirement options for state workers. Despite the lack of legislative changes in 2021, momentum for reform is clearly building. It’s important to build on this interest during the interim to ensure the 2023 legislative session is more successful. Policymakers should keep in mind that of all the possible outcomes, leaving NDPERS’ problems unaddressed will end up being the most expensive and least secure option for North Dakotans, and this challenge will only become more difficult to address as time passes.