The State Teacher Retirement System of Ohio (STRS) oversees the retirement benefits of teachers and faculty hired by the state’s school districts. Covering 174,036 active members and 156,225 retired teachers, STRS plays an integral part in securing the retirement of Ohio’s educators. The state’s retirement system has innovated in the public retirement space by offering new hires several retirement plan options, allowing STRS the flexibility to serve an evolving workforce. However, like most other government-sponsored pension plans, the system has faced significant funding challenges over the past two decades, and additional pension reforms are warranted.

Ohio’s prudent cost-managing reforms in 2012 have greatly improved the position of the State Teacher Retirement System, which is currently enjoying a better financial trajectory than most other state-run pension plans.

Still, with taxpayers continuing to foot the bill of expensive public pension debt and the potential for another significant stock market setback always looming, state lawmakers need to take the time to reexamine the long-term financial security of STRS. Policymakers should also reevaluate STRS’s defaults, which could help the plan better meet the evolving needs of the modern workforce of newly hired teachers.

The Advantages of Choice in Retirement Plans

The State Teacher Retirement System of Ohio offers new hires a choice between three retirement plans:

- The defined benefit (DB) pension plan reflects the traditional pension structure with guaranteed lifetime benefits and places funding shortfalls on the shoulders of current and future taxpayers.

- The defined contribution (DC) plan offers a 401(k)-style alternative with the advantage of flexibility for teachers who may not spend their entire careers in the state’s system, but the plan places all investment risk on employees.

- The third option is a mix between the first two. The STRS Combined Plan is a hybrid that directs most of the employee’s contributions into a defined contribution account while sending all of the employer’s contributions, and a small portion of the member’s, to the defined benefit fund. The hybrid option offers some of the flexibility and advantages of an individual account while providing a partial pension benefit.

The choice between these three retirement designs gives STRS an advantage in serving a wider range of employee types. Teachers who want the flexibility to explore other careers (or even the same career in a different state) can choose the DC or hybrid options. If a newly hired teacher does not make an election, they default into the DB plan.

Defaults have an enormous impact on plan elections, so it is no surprise that the defined benefit plan heavily outpaces the other two options. According to STRS reporting, 90% of current active members are enrolled in the DB plan, 6% selected the DC plan, and 4% chose the hybrid combined plan.

This choice-focused structure also has the advantage of reducing the risks of runaway costs that have pervaded state public pension systems since the early 2000s. The 6% of active teachers in the defined contribution plan do not add to the state’s ongoing struggle with unfunded pension obligations, and the 4% in the hybrid only do so at a reduced rate.

Runaway Debt and Ohio’s Response

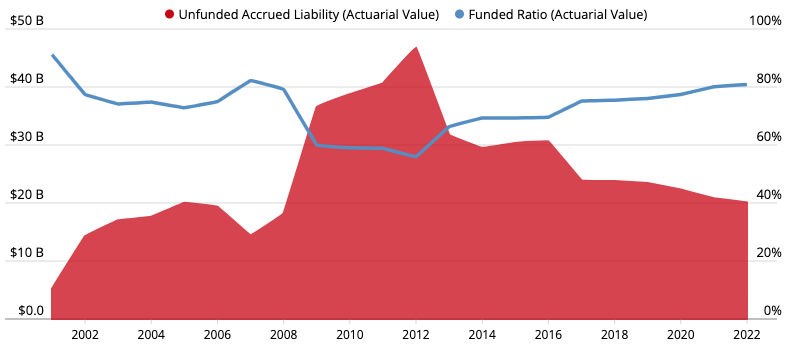

Despite the risk-reducing advantages of STRS’ choice framework, the system faced a major pension funding problem after the Great Recession. From 2007 to 2012, the STRS’ unfunded liabilities grew from $14.5 billion to $46.8 billion. State teachers saw their pension plan fall from 82% funded to 56% funded over just five years. In other words, by 2012, STRS only had the funds to pay for 56%, just over half of the benefits already promised to workers and retirees.

Figure 1: Ohio STRS Pension Funding History

Source: Pension Integrity Project analysis of STRS annual financial reports.

Ohio lawmakers responded to this pension debt explosion with cost-saving changes to the state’s public pensions, including STRS. In 2012, the Ohio legislature passed Senate Bill 342, which increased the age of retirement and service requirements, reduced the benefit multiplier, increased member contributions by 4%, extended the years that were used to calculate final average salary, and reduced annual cost-of-living adjustments (COLAs) for retirees to 2%. The legislation also gave authority to the retirement board, the governing body overseeing the management of STRS, to make further changes to contributions or benefits in the future as needed.

These sweeping changes had an immediate impact on the trajectory of STRS. Plan actuaries indicated that the cost-saving measures set the pension system on a path to eliminate its pension debt within 30 years. Within one year, the pension reform reduced STRS’ unfunded pension liabilities by $15 billion (from $46.8 billion to $31.8 billion), mainly as a result of the changes to benefits and the increases in teacher contributions.

Using its newly minted authority to adjust cost-of-living benefits according to funding needs and seeing a slower-than-expected progression to full pension funding, the Retirement Board stopped annual COLAs for retirees in 2017. They revisited this benefit in 2022, eventually giving STRS retirees a one-time 3% cost-of-living adjustment that year but leaving the question of future COLAs as a perennial political skirmish between retired teacher advocacy groups and lawmakers. This arrangement gives little predictability to retired teachers and results in little forethought in how to fund annual adjustments in advance.

Now, with more than 10 years passed since the initial push for reducing STRS pension debts, the system stands at around 77% funded, slightly higher than the national aggregate 75% funding figure calculated by the Reason Foundation’s Pension Integrity Project. Plan actuaries estimate that STRS can eliminate its unfunded pension liabilities within 11.5 years if its assumptions on investment returns and other factors prove accurate.

However, state policymakers should not rest on their laurels regarding STRS’ pension debt. After all of the state’s cost-saving efforts, STRS is only back to its 2008 funding levels, and there is still a long way to go before the state can say it has fully funded the pension promises made to its teachers. Furthermore, a glimpse into the future suggests that the pension system could face significant funding challenges again if efforts aren’t made to bolster the pension fund from more potential market downturns.

STRS Is Still Vulnerable to Market Volatility

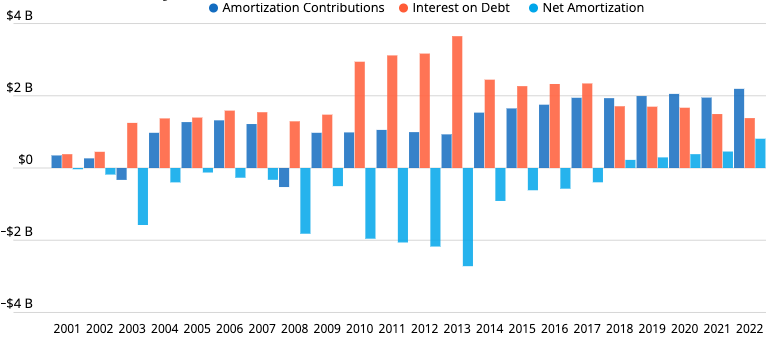

The fallout from the Great Recession was a clear example of how a public pension benefit could cost much more than initially estimated. The unfunded liabilities generated from STRS’ massive loss in asset value came at a significant cost to state employers and taxpayers. Unfunded liabilities work just like any debt in that they accrue interest. Due to the historic jump in STRS’ unfunded liabilities in 2008, the interest on that debt grew to the degree that it even exceeded the amortization (or debt servicing) payments made annually. That meant that despite annual contributions rising above what was needed in the early 2000s, this was still not enough to counteract the massive interest that was accruing on the pension debt (see Figure 2). It took Ohio an entire decade to turn the corner to begin making a dent in STRS’ unfunded liabilities.

Figure 2: History of STRS Debt Payments

Source: Pension Integrity Project analysis of STRS actuarial valuations.

Interest on pension debt is very expensive and lasting. Reason Foundation’s Pension Integrity Project analysis finds that about 75% of STRS’ existing unfunded liabilities can be attributed to interest on the pension debt that has accrued since 2001.

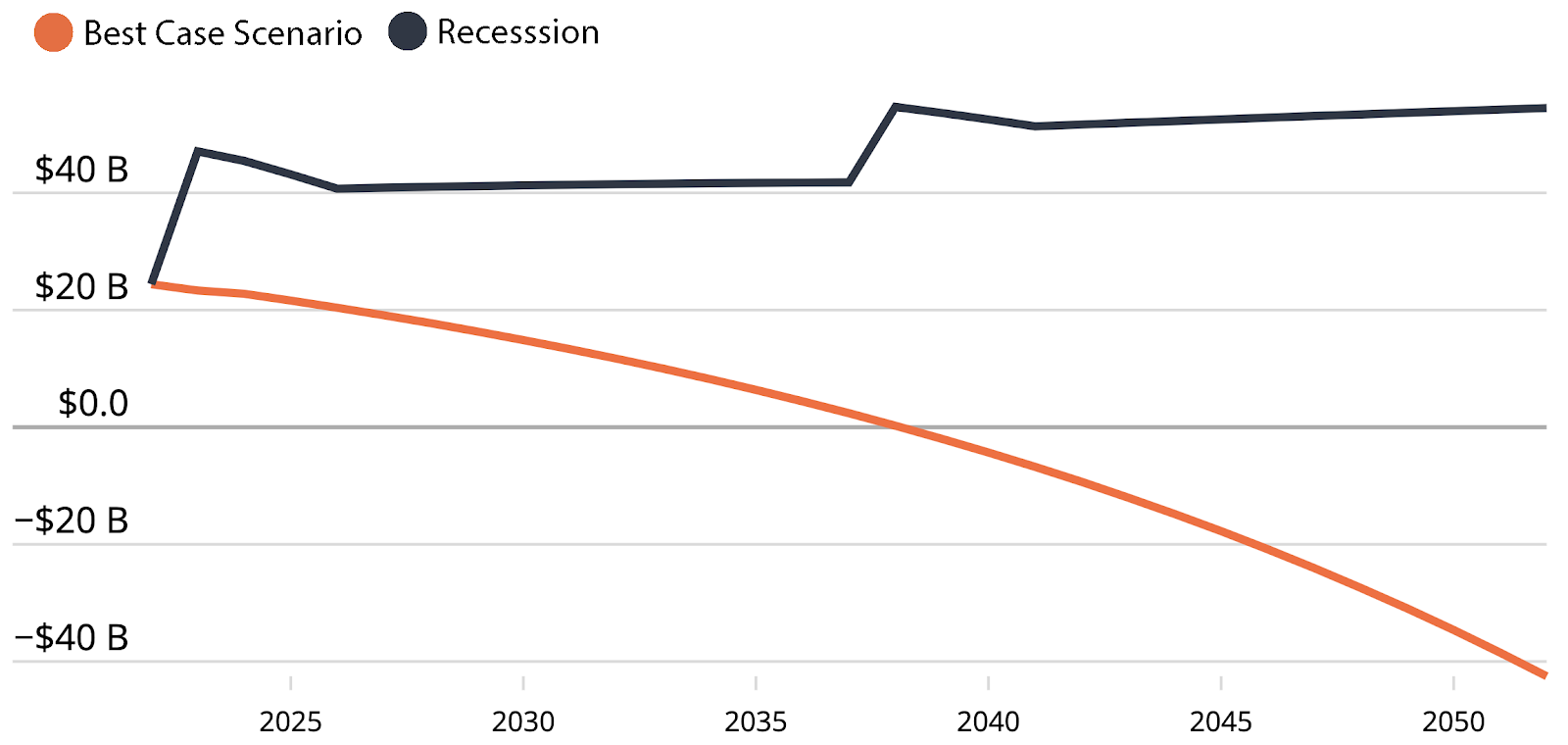

Pension Integrity Project modeling of STRS reveals that the pension system would not be able to withstand similar market stress in the future, nor would it reach full funding as suggested by the somewhat idealized best-case assumptions and modeling used by the system. While the pension system today appears to be on a trajectory to eliminate its public pension debt within the next 15 years, this outcome will require that all of the plan’s investment return assumptions prove accurate, which would be a different experience from the last few decades. In other words, the system remains vulnerable to continued debt challenges, as another major recession during that time would massively degrade STRS funding.

Figure 3: STRS Unfunded Liabilities Would Rise Under Another Recession

Source: Pension Integrity Project actuarial modeling of STRS. The stress scenario applies two Dodd-Frank recessions, one in 2024 and another in 2039.

Despite the state’s laudable efforts to manage the costs and funding of STRS, it remains vulnerable to future market downturns, so much so that it could again see unfunded liabilities exceeding $40 billion and funding again falling to dangerous levels. While the teachers’ pension plan appears to be on track to achieve full funding under the best-case scenario, it is not resilient to potential future recessions.

Policymakers should take the opportunity now to shore up the system against potential market and economic downturns. Waiting until another recession to make the necessary adjustments could lead to another lost decade and billions in avoidable costs to taxpayers.

What Can Ohio Do to Make STRS Resilient

Ohio uses an annual contribution rate that is set in statute. This rate currently exceeds the amount that actuaries say is necessary to achieve full funding, and because of this aggressive contribution policy used by the state, STRS is on an accelerated path to full funding.

However, this policy of using a static and statutorily set rate could work against system funding efforts if the pension were to face another recession. As the modeling analysis above shows, a recession would suddenly require contributions above the current rates set in statute, and failure to respond to those needs would inevitably lead to significant growth in pension debt.

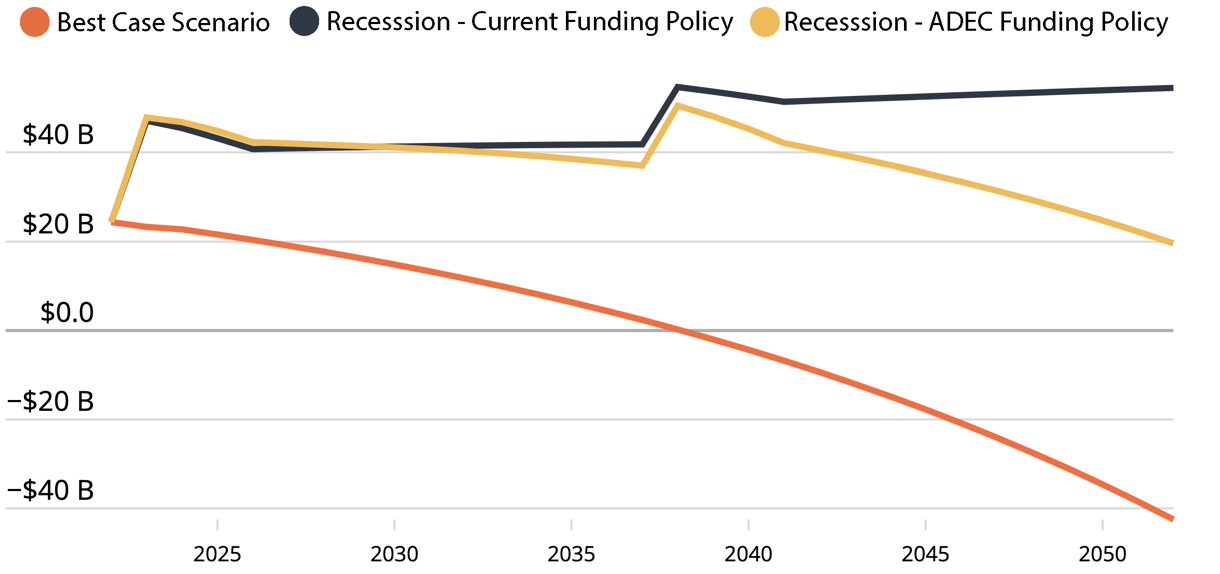

Policymakers in Ohio should consider keeping the current statutory rates that have STRS on a path to full funding within 15 years but should adopt a contribution floor that is based on the annual rates that are already calculated by plan actuaries (commonly known as actuarially determined employer contributions, or ADEC). This would ensure that should the need arise, contributions coming from the state would be responsive in a way that would keep STRS on track and away from expensive and avoidable interest on pension debt (see Figure 4).

Figure 4: STRS Unfunded Liabilities with the Proposed ADEC Floor

Source: Pension Integrity Project actuarial modeling of STRS. The stress scenario applies two Dodd-Frank recessions, one in 2024 and another in 2039.

The other policy Ohio lawmakers should explore is a change in the default plan for newly hired teachers. As mentioned before, Ohio’s retirement systems already offer an exceptional level of choice to new hires, and the two alternative retirement plan choices (hybrid and DC) can be valuable tools for risk reduction.

The modern generation of teachers is increasingly mobile and less likely to remain with the same employers for their entire careers. With that in mind, it would be prudent to switch the default option to the defined contribution retirement plan or hybrid plan to better match the needs of the majority of new hires. Pension benefits often favor teachers who end up sticking around for the entirety of their career, but the larger share of teachers who end up moving to other employment options within five-to-10 years don’t get to take part in these advantages and are better off in a DC or hybrid plan in most cases.

Making the defined contribution or hybrid plan the default selection—meaning the option selected for new teachers who do not make an active election—would keep the pension option open to new teachers but would bring a larger number into the plan options that better fit most of the modern workforce, while gradually reducing the state’s future exposure to the runaway costs that have come with pensions.

Conclusion

Ohio policymakers have made great strides in offering retirement options to teachers and funding those promises despite several challenging years of expensive interest on pension debt. While the funding of STRS appears to be on the right trajectory, lawmakers should be looking ahead and preparing for the unpredictable.

Stakeholders need to prepare now to avoid another lost decade of growing public pension costs with diminished benefits, and it is time to adjust default offerings to match an increasingly mobile population of teachers.