Social Security, an important pillar of the New Deal, was established during the Great Depression to provide financial security to Americans in retirement. However, today, Social Security is facing critical challenges and looming insolvency.

A few states have declined to have their public employees participate in Social Security, and while some states have still yet to figure out their role in providing retirement income for their public employees, the state of Alaska has put forth an effective blueprint for an alternative to Social Security.

The Alaska Supplemental Benefits System Annuity Plan (SBS-AP) is offered to all state employees (excluding teachers) in 23 political subdivisions. Compared to other states’ plans, SBS-AP stands as a beacon of innovation and effectiveness. Alaska’s supplemental retirement savings plan offers a model that addresses the contemporary challenges of retirement savings much better than Social Security.

The trust funds that support Social Security are on track to be depleted by 2033. This is not just an abstract future risk; it’s a countdown to a reality where beneficiaries could receive only a portion of their promised Social Security benefits if reforms are not implemented. The root causes of Social Security’s impending insolvency are deeply embedded in demographic trends. An aging population in the U.S., longer life expectancies, and a declining birth rate are converging to create a perfect storm.

Fewer workers are coming in to support an expanding pool of retirees, a shift that fundamentally undermines the deeply flawed pay-as-you-go funding model of Social Security. This demographic imbalance is like a seismic fault under the foundation of Social Security, threatening to disrupt the retirement plans of millions.

In contrast, the Alaska Supplemental Benefits System Annuity Plan is a plan that’s grounded in the principle of personal control and investment choice. Unlike Social Security, the SBS-AP allows individual employees to have direct control over their retirement investments. Participants can choose how their contributions are invested from a range of options, tailoring their individual investment strategies to their personal risk tolerance and retirement timeline. This level of autonomy is empowering and contrasts starkly with the one-size-fits-all approach of Social Security.

Secondly, the Alaska SBS-AP can provide substantially higher returns on investment than is given to participants of Social Security. Since SBS-AP participants can choose diverse investment portfolios, they can benefit from the higher yields typically associated with equity and other high-risk/high-reward investment options. This feature is particularly relevant in today’s era of longer life expectancies, where the ability to grow retirement savings is crucial.

In contrast, Social Security benefits are not directly tied to market performance because the assets are invested only in U.S. Treasury securities. These assets often don’t keep pace with inflation, let alone provide significant investment growth potential.

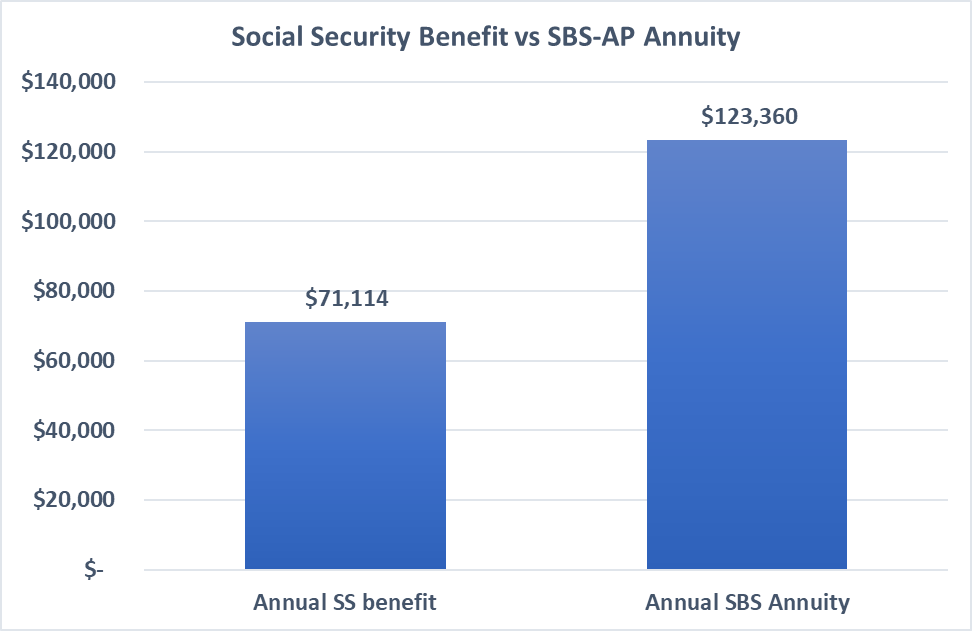

Exhibit A displays the expected annual benefit provided by Social Security compared to the expected annual annuity from SBS-AP. This example uses a teacher hired in Alaska today at age 30, with a starting salary of $60,000. It also assumes the teacher will begin drawing their Social Security benefit and annuitize their SBS-AP assets at age 67. From Reason Foundation’s calculations, the SBS-AP would provide a new teacher with a retirement income that is 73% greater than Social Security would provide.

Exhibit A

Moreover, the financial sustainability of the SBS-AP is another significant advantage for workers. The challenges threatening Social Security’s long-term solvency are well-documented, and the strain on the program’s funds is only going to increase. Unlike Social Security, the SBS-AP’s structure as a defined contribution plan means it doesn’t face the same demographic pressures.

SBS-AP contributions are invested, and benefits are directly tied to these investments, making the system more accountable and financially sustainable in the long run. If an employee leaves Alaska state employment, their SBS-AP assets go along with them as well.

In addition to these financial benefits, the SBS-AP also offers greater transparency and predictability. Participants receive regular statements showing the value of their investments, allowing them to make informed decisions about their retirement planning. In contrast, Social Security’s future benefit levels and the overall health of the trust fund are subjects of political debate and uncertainty, making long-term planning more challenging.

However, it’s important to acknowledge that the SBS-AP, like any investment-based plan, carries some risks. The value of investments can fluctuate, and poor investment choices can lead to inadequate retirement savings. This risk underscores the importance of financial literacy and access to sound investment advice for participants in the plan. This literacy risk is mostly mitigated by the plan’s default investment options. For example, new entrant contributions are automatically invested in one of the Alaska Target Retirement Trusts or the Alaska Balanced Trust. These trusts function similarly to a target date fund where the mix of assets automatically adjusts to become more conservative as the target retirement date approaches. Having said that, it would be almost impossible, barring a decades-long recession, for an employee in the default SBS-AP plan to earn less on their assets than Social Security earns on its assets.

While Social Security remains a critical component of the retirement landscape in the United States, the Alaska SBS-AP offers a compelling alternative model that addresses many of the limitations of the federal program. Its emphasis on personal control, higher investment returns, financial sustainability, portability, and transparency position SBS-AP as a superior option for ensuring financial security in retirement.

As policymakers and stakeholders grapple with the challenges of providing adequate retirement benefits to public workers in a changing demographic and economic environment, the Alaska SBS-AP serves as a valuable case study in innovative retirement planning.