Executive Summary

The COVID-19 pandemic has put new fiscal stress on some state and local governments. One tool that may help them cope is called “asset monetization,” sometimes referred to as “infrastructure asset recycling.” As practiced by Australia and a handful of U.S. jurisdictions, the concept is for a government to sell or lease revenue-producing assets, unlocking their asset values to be used for other high-priority public purposes.

This study focuses on the potential of large and medium hub airports as candidates for this kind of monetization. Under federal airport regulations, governmental airport owners are not allowed to receive any of an airport’s net revenue; all such revenues must be kept on the airport and used for airport purposes. Overseas, there are no such restrictions. Over the past 30 years, numerous governments have corporatized or privatized large and medium airports and received direct financial benefits from doing so.

In 2018, as part of legislation reauthorizing the Federal Aviation Administration, Congress created an important exception to the long-standing restriction. The new Airport Investment Partnership Program (AIPP) enables governmental airport owners to enter into long-term public-private partnership (P3) leases—and use the net lease proceeds for general governmental purposes.

This study explores the potential of airport public-private partnership leases for 31 large and medium hub airports owned by city, county, and state governments. It draws on data from dozens of overseas airport public-private partnership lease transactions in recent years to estimate what each of the 31 airports might be worth to investors.

The gross valuation is what the airport might be worth in the global marketplace. The net valuation takes into account a U.S. tax code provision that requires existing airport bonds to be paid off in the event of a change of control, such as a long-term lease. Hence, the net value estimate is the gross value minus the value of outstanding airport bonds.

Since P3 leases of airports are uncommon in the United States (the only existing example is the San Juan, Puerto Rico airport), the study explains three categories of likely investors in U.S. airports.

First is a growing universe of global airport companies, including the world’s five largest airport groups, which operate a growing share of the world’s largest airports by annual revenue.

The second is numerous infrastructure investment funds, which have raised hundreds of billions of dollars to invest as equity in privatized and P3-leased infrastructure facilities worldwide.

The third category is public pension funds, which are gradually expanding their investments in infrastructure in an effort to reverse declines in their overall rate of return on investments.

All three types of investors have long time horizons and are comfortable investing in and further developing these kinds of assets.

The study explains that proceeds from the lease of a major infrastructure asset such as an airport should be used to strengthen the jurisdiction’s balance sheet, rather than using such a windfall for short-term operating budget needs. It explains and provides examples of three potential uses:

• Invest the proceeds in needed but unbudgeted infrastructure;

• Use the proceeds to pay down existing jurisdictional debt; and/or

• Use the proceeds to reduce the jurisdiction’s unfunded pension system liabilities.

On the latter point, the study compares the net airport P3 lease proceeds with each jurisdiction’s unfunded pension system liabilities. It identifies several jurisdictions where the estimated net airport lease proceeds exceed total pension system liabilities, a number of others where the proceeds could significantly reduce those liabilities, somewhere the liabilities are so large that airport lease proceeds would have only a modest impact, and a handful where there would not likely be an airport lease, unless investors valued those airports higher than the conservative numbers used in this study.

The relative attractiveness of using lease proceeds for each of these purposes will likely depend on the specifics of the city, county, or state in question. A government with a pressing need for a major unfunded infrastructure facility may find that use the most attractive, while a jurisdiction where unfunded pension liabilities threaten either large tax increases or something akin to bankruptcy may prefer using an airport windfall to shore up its pension system.

Introduction

Across the United States, many airports are owned and operated as departments of city, county, or state governments. Airports are highly valuable business enterprises, linking cities to other cities across the country and, directly or indirectly, around the world. Airports serve passengers but also move a vast amount of high-value cargo.

In many countries, governments have restructured airports as commercial real estate assets, enabling airports to attract investment capital on their own economic merit. These changes have enabled larger airports to generate net revenues for their government owners, in addition to the economic benefits they create for their state and metro area.

But that is not the case in the United States. All commercial airports in this country receive federal Airport Improvement Program (AIP) grants. One condition of these grants is that all airport revenues must remain on the airport and be used only for airport purposes.

Therefore, the governmental owner of a U.S. commercial airport cannot receive any direct financial benefit from that airport. In financial terms, the government owner’s return on the airport’s equity is zero.

Actually, there are two little-known exceptions to the above restriction. When Congress first authorized AIP grants, it “grandfathered” a handful of airports that had a long history of diverting net airport revenues to their government owners. Of the 12 that were originally grandfathered, only nine airport sponsors (including the Port Authority of New York and New Jersey) are still covered by this exception.1Miller, Benjamin M., et al. “U.S. Airport Infrastructure Funding and Financing.” RAND Corporation, 2020. Chapter 3. 36. On the other hand, all commercial airports were given a new option in 2018, when Congress enacted the most recent reauthorization of the Federal Aviation Administration (FAA). A new section of that legislation—the Airport Investment Partnership Program (AIPP)—permits governmental airport owners to enter into long-term public-private partnership (P3) leases of their airports. The net lease proceeds can be retained by the governmental airport owner and used for general governmental purposes.

Many city, county, and state governments are not familiar with this recent development. It is also unlikely that they know the market-based asset value of the airport or airports they own—and could potentially lease under the provisions of the new AIPP. Yet this concept has been used overseas for several decades, as countries have changed their governance models for large and medium commercial airports.

Leasing revenue-producing assets (such as airports) and using the lease proceeds for other governmental purposes is sometimes known as “asset monetization” or alternatively as

“infrastructure asset recycling.” In many such cases the net present value of a long-term (e.g. 50 years) stream of lease payments is paid to the government up-front. Wise policy calls for such sums to be used for balance-sheet purposes, rather than for short-term budget balancing. Well-run governments invest a one-time windfall such as this in paying down outstanding debt, shoring up under-funded pension systems, or on large-scale (and otherwise unfunded) infrastructure.

This report explores the potential of long-term P3 leasing of airports owned directly by city, county, and state governments in the United States. Subsequent sections discuss how airport governance has changed worldwide over the past three decades, the emergence of global airport companies, how airports and other revenue-producing infrastructure are valued by investors, what 31 large and medium U.S. airports might be worth, what kinds of entities are interested in bidding on airport P3 leases (including the emerging role of public pension funds), and some further thoughts on wise use of the proceeds.

Changed Airport Governance Since 1897

Prior to 1987, nearly all the world’s commercial airports were organized as departments of government, in many cases (e.g., Canada and the U.K.) as departments of the national government. That changed dramatically in the U.K. in 1987 as part of the Thatcher government’s wide-ranging privatization of state-owned enterprises. Utilities such as electricity, water, natural gas, and telephone systems were sold to investors, with shares traded on stock exchanges. The same process was applied to the British Airports Authority (BAA), which owned and operated the three major London airports (Heathrow, Gatwick, and Stansted) and several Scottish airports. In 2009, to promote competition, the government required privatized BAA to sell off Gatwick, Stansted, and the Scottish airports, which are all now owned and operated by other investor-owned companies.

In the decades since then, most other large European airports have also undergone changes in governance. A few others were sold outright, à la BAA (e.g. Brussels, Copenhagen), but more common has been the sale of part of the equity to investors with governments retaining the balance. This is the model used in France for Aeroports de Paris and in Germany for airports including Frankfurt, Düsseldorf, Hamburg, and several others.

A different model has emerged in Australia, Asia, other parts of Europe, and Latin America. Countries in these regions have embraced the long-term public-private partnership (P3) lease model. Australia applied this to nearly all its major airports around the turn of the century, offering 50-year leases with 49-year renewal options. Major countries in Latin America followed suit, with Argentina taking the lead, followed by Brazil, Chile, Colombia, Mexico, and Peru, among others. In Asia, the governments of India, Japan, Malaysia, and the Philippines are among those opting for the long-term P3 lease model.

In 2018, Airports Council International, the global airports trade association, published a detailed study on private investment in airports.2Airports Council International. “Policy Brief: Creating Fertile Grounds for Private Investment in Airports.” January 2018. ACI’s research found that in several regions more than half of all airline passengers were being served by airports with majority private-sector investment. The regional totals were as follows:

- Africa – 11% passengers

- Asia-Pacific – 47%

- Europe – 75%

- Latin America/Caribbean – 66%

- Middle East – 18%

- North America – 1%

The change to significant investor involvement in airport management and governance has led to more-robust financing. The ACI report noted that the changed governance model has enabled large increases in airport capital improvements. These include new terminals at all three major London airports (Gatwick, Heathrow, Stansted), Frankfurt, Lisbon, Paris, Lima, Santiago, Sydney, Melbourne, etc. Private capital has also been invested in runway additions at airports including Bogotá, Frankfurt, Vienna—and potentially London Heathrow (approved by Parliament but being opposed by local and environmental litigation).

ACI also compared traditional and investor-financed airports during 2012–2016 and found that capital expenditure per workload unit was $4.76 at traditional airports vs. $5.40 at investor-financed airports. This is noteworthy because it shows that private investors with a long time horizon are willing to continue investing in their airports’ further development even after the initial capital outlay to lease the airport.

What Are Major U.S. Airports Worth?

Infrastructure investors consider many factors when they assess possible investments in revenue-producing infrastructure, whether this be railroads, pipelines, or electric and natural gas utilities. In the United States, most of those entities are already in the private sector and function fully as businesses. When investors consider a long-term P3 lease of a facility that is currently owned and operated by a government, which they plan to make operate more as a business, they assess both its current operations and financial conditions, and also its potential for improvement as a commercial business.

For this kind of infrastructure acquisition, a widely used metric for assessing current value is earnings before interest, taxes, depreciation and amortization (EBITDA). It provides a measure of near-term operational performance as measured by operational cash flow. Interest payments on existing debt are a significant factor in that cash flow, but government-owned enterprises such as U.S. airports are generally exempt from taxation. Depreciation and amortization are non-cash expenses.

Acquirers of airports, seaports, toll roads, and other infrastructure use the facility’s current financial statements to calculate its EBITDA. They develop valuation rules of thumb, based on recent transactions for the type of facility, of what multiple of EBITDA investors that won competitions agreed to pay. Thus, if a decade’s worth of seaport purchases or long-term P3 leases averaged 10 times each facility’s EBITDA (written as 10X), then that would be a good way to estimate such a facility’s acquisition price. (And for long-term leases, the price would be about the same for a 50-year P3 lease and an outright purchase.) On the other hand, an actual offer to lease the airport would be based on a more detailed study of the specific airport and its potential under private management.

In a recent Reason Foundation study on infrastructure asset recycling, data assembled from such transactions in the recent decade yielded the following average EBITDA multiples:3Poole, Robert W., Jr. “Asset Recycling to Rebuild America’s Infrastructure.” Reason Foundation. October 2018.

- Airports – 16X

- Seaports – 14X

- Toll Roads – 26X

- Parking Facilities – 22X

- Water/wastewater – 12X

Those numbers are averages across a set of transactions, with a range of values on either side of the average, depending on the specifics of the facility in question. It should also be noted that the short-term effects of the Covid-19 recession may reduce EBITDA multiples in the short term, despite airports being long-term investments.

Selected U.S. Airports and Their Estimated Values

For this study, 31 large and medium hub airports (as defined by FAA based on their annual passenger volumes) were selected. Table 2 lists those airports and identifies the owner of each. Fifteen are large hubs and 16 are medium hubs. Ownership breaks down as follows:

- City Government – 19

- County Government – 6

- Joint City/County – 2

- State Government – 4

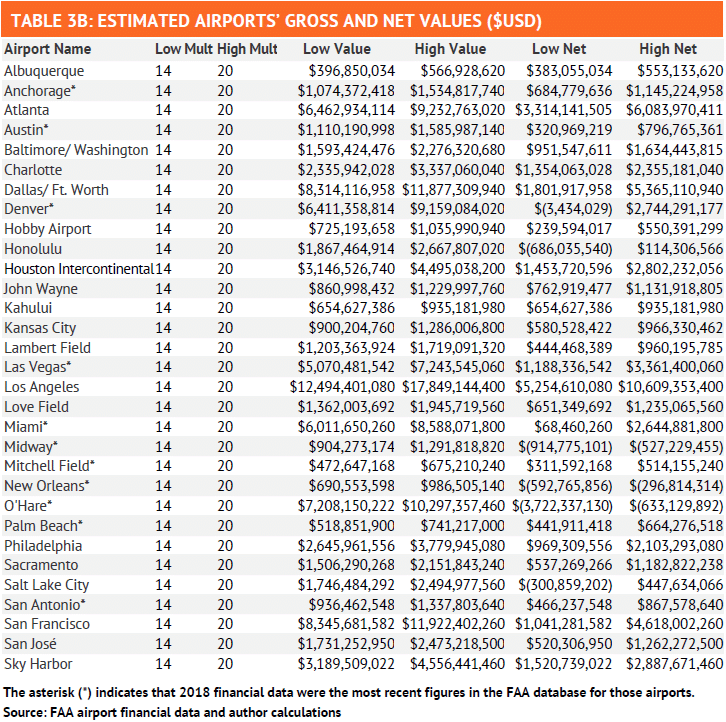

Multiplying the EBITDA number by the relevant multiple yields a low and a high estimate of each airport’s gross value. Los Angeles International (LAX), for example, has an estimated gross value ranging from a low of $12.5 billion (at 14X) to a high of $17.8 billion (at 20X). For much-smaller John Wayne Airport (SNA), the gross value estimates range from $861 million to $1.2 billion.

However, the gross value is not the end of the story. Under federal tax law, facilities financed via federally tax-exempt bonds cannot be transferred to P3 investors unless those bonds are paid off or refinanced. Table 3A also lists the outstanding debt of each airport. Because the airport owner must pay off the existing debt, that amount is subtracted from the estimated gross value to get the estimated net value of proceeds to the city, county, or state government that owns the airport. For most of the airports in Table 3B, that is still a sizable number.

Six of the airports in Table 3 have such a large outstanding debt (due to recent expansion projects) that if their gross value is calculated using the low (14X) multiple, the net value is negative. The most dramatic example is Chicago O’Hare, whose low valuation goes from $7.2 billion pre-debt payoff to minus $3.7 billion after debt payoff. That would make this an unattractive investment. If the gross proceeds turn out to be closer to the high (20X) multiple, only three airports would have a negative net value: Chicago Midway (MDW), New Orleans (MSY), and Chicago O’Hare (ORD). Those airports might still be of interest to investors if the airport market shifts toward higher EBITDA multiples (e.g., 25X or 30X) after the Covid-19 recession.

There are differences of opinion about airport EBITDA multiples going forward. In November 2019, Inframation News reported that its study of airport valuations from 2010 through 2018 found “a steady increase in multiples over the eight-year timeframe,” based on 31 European transactions involving single airports.4Martinez, Pablo and Jenisa Patel. “The Story in Numbers: European Airport Valuations High and Rising.” Inframation News. Nov. 19, 2019. Three months later, Infrastructure Investor raised a caution flag based on two adverse actions in the U.K.—a local government (North Somerset) blocking a planned expansion of investor-owned Bristol Airport and a ruling by the Court of Appeal against the previously authorized third runway project at London Heathrow.5Week in Review. “Should Airport Valuations Prepare for a Hard Landing?” Infrastructure Investor. Feb. 27, Both actions stemmed from concerns over climate change and the 2016 Paris Agreement. Another warning flag was raised by Inspiratia, another infrastructure analysis service. While reporting very recent airport transactions early in 2020, it cited the coronavirus and Brexit as potentially reducing airline and airport passenger volume in 2020—and hence, near-term airport value.6Coker, Omolola. “Covid-19, ESG, and Brexit Effect All Threatening 2020 Airport Activity.” Inspiratia. March 5, 2020

To the extent that investors are more cautious about airports in 2021 and beyond, valuations may end up being closer to our low estimates (based on 14X) than on our high estimates (based on 20X). Fitch Ratings estimates a two-year recovery period for air traffic, and points out that the airports it rates “are generally in strong financial positions, with an average of 500 days’ cash on hand and a debt service coverage ratio of 1.8. 7Broderick, Sean. “Fitch Ratings Eyes Two-Year U.S. Traffic Recovery Period.” Aviation Daily, March 25, 2020. On the positive side, since only one U.S. airport is currently operating under a long-term P3 lease (San Juan), there are indications of pent-up investor demand for U.S. airports that could lead to multiples at or above the high end of the valuation estimates. For example, when the city of St. Louis issued its request for qualifications for a potential P3 lease of its Lambert Field airport in 2019, there was great surprise that 18 teams submitted qualifications. 8Siemers, Erik. “City Attracts 18 Firms Interested in Privately Operating Lambert Airport.” St. Louis Business Journal. Nov. 4, 2019.