A brilliant column in the Financial Times by Nobel laureate Vernon Smith and Steven Gjerstad.

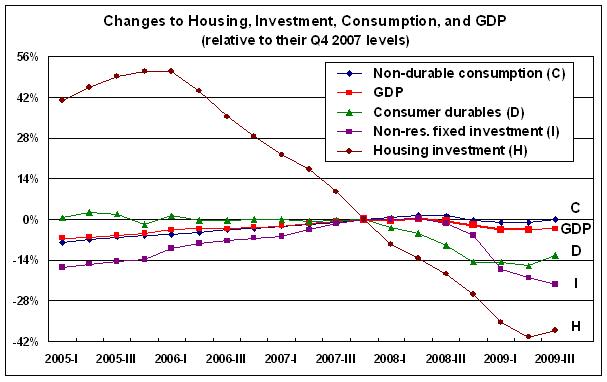

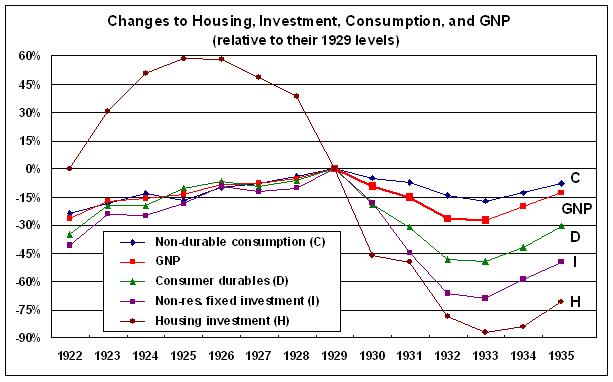

Jumping out at me in particular are two nice graphs that show how housing investment collapsed well before other investment and consumption and effectively drug them down during the current recession and the Great Depression. The graphs ALSO show how much less severe this recession is than the depression.

{kind=link}

{kind=link}

In A Monetary History of the United States, Friedman and Schwartz roundly criticised the Fed for its failure to aggressively expand the money supply from 1930 to 1933. By contrast, many people have criticised the Fed for the scale of its current intervention. How did we reach conditions where the Fed felt compelled to choose between a limited response — which would risk a de-leveraging spiral and collapsing GDP — and a rapid expansion of the monetary base? In part it was because another lesson from the depression went unlearned. Just as in the current crisis, rapid mortgage credit expansion fueled a housing bubble. When house prices fell, mortgage debt weighed on household and bank balance sheets. The deterioration of household balance sheets led to suppressed housing and durable goods expenditures which in turn led to declines in production, employment and investment.

Once the immensity of the current collapse became apparent, Fed Chairman Ben Bernanke applied depression policy lessons to the current crisis, but he was initially reluctant to go beyond traditional liquidity enhancement interventions. In an October 15 2007 speech, Bernanke reiterated the principle that “…it is not the responsibility of the Federal Reserve — nor would it be appropriate — to protect lenders and investors from the consequences of their financial decisions,” adding the qualification, “but developments in financial markets can have broad economic effects felt by many outside the markets, and the Federal Reserve must take those effects into account when determining policy.” By September 2008, the qualification swamped the principle: before the end of 2008 the Fed had reserved a woefully under-collateralised financial system with $333bn in lending on commercial paper, $544bn in discount window loans, and more than $82bn of asset purchases from counterparties to AIG credit default swaps. Though the composition of the intervention has changed over the past year, its magnitude has fallen only slightly.

. . .

The lesson is not just that the Fed failed to anticipate the collapse in the bubble: it also didn’t foresee its devastating consequences. This is reflected in the candid comment last year by Fed Vice Chairman Donald Kohn (Cato Journal): “I and other observers underestimated the potential for house prices to decline substantially, the degree to which such a decline would create difficulties for homeowners, and, most important, the vulnerability of the broader financial system to these events.”

In his “Asset-price Bubbles and Monetary Policy” speech in October 2002 Bernanke noted “evidence for boom-bust cycles in residential property: busts followed 10 of 19 booms.” These are poor odds given the collateral damage nationwide residential price collapses can do to household and bank balance sheets.